Investment Memo:

Haranga Resources Ltd

(ASX:HAR)

-

LIVE

Opened: 25-Jun-2025

Shares Held at Open: 7,570,066

What does HAR do?

Haranga Resources (ASX: HAR) will hold 100% of the Lincoln gold mine, a high grade gold project in the “Mother Lode” region in California, USA.

HAR’s project already has a 286,000 oz non-JORC resource, HAR will be drilling to first define a JORC resource, then target an upgrade to 1 million ounces of gold.

What is the macro theme?

Gold is a precious metal often used as a hedge against inflation, which remains persistently high, and the gold price is trading at all-time highs at the time of this memo.

Gold demand in the USA is at all time highs, and Trump just signed an executive order which explicitly mentions gold as one of the minerals that the USA needs to increase production of.

We think HAR is well-positioned to benefit from these macro tailwinds.

Our Big Bet for HAR

“HAR re-rates to a +$100M market cap on significant resource growth and/or a transaction with a major player in the nuclear fuel supply chain”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our HAR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in HAR?

Advanced gold project in the USA - Gold macro thematic is very strong right now, especially in the USA.

The gold price recently broke out into all time highs above US$3,400 per ounce and is setting new highs every day.

We think gold explorers/developers will do well in this macro environment.

It’s only been ~3 months since HAR announced its planned acquisition, but the gold price is up another ~US$400 per ounce.

The “Mother Lode” is in one of the most prolific gold producing jurisdictions, ever

HAR’s project is in Amador county - one of the epicentres of historical California gold production - this is a county that has produced at least 7.7 million ounces of gold.

Overall the state of California has produced over 115 million ounces of gold and was the centre of one the biggest gold rushes in history.

Back in the late 1840s the world descended on California in search of gold.

HAR will now own 100% of a ~6km trend where there has previously been ~3.4 million ounces of gold production in the past.

High-grade gold resource with expansion potential

HAR’s project area has a current non-JORC 286,000 ounce gold resource at 9.29g/t of gold.

And there is at least up to ~682,000 ounces of gold that HAR thinks could be there based on data from back in 2008 (again this is non JORC data).

We think that HAR has the potential to expand this gold resource with a targeted exploration program.

Exploration upside - target to grow to >1 million ounces of gold

Most of the mines in the region have produced gold down to depths of ~1,800m.

HAR’s resource is based on drilling down to depths of ~150m.

We think that with some drilling (and luck), HAR can grow its resource beyond the current 286,000 ounce number.

Permitted processing plant with district scale consolidation opportunity

HAR holds a Conditional Use Permit (CUP) for its 350,000 tpa processing plant.

The CUP means HAR can operate its project without having to go through a lengthy permitting process.

Permitting in California can be a 15+ year process and so this puts HAR in a strong position to leverage its permits to potentially “roll up” regional opportunities.

California’s permitting landscape has historically been challenging, but HAR’s Lincoln Mine acquisition avoids many of these obstacles by already holding key approvals.

AND, anyone who wants to monetise their resources in the area will likely have to speak to HAR.

There’s A$90M in sunk capital into the project - including a 350,000 tpa processing plant

Over A$90M has been invested into the project to date including into a 350,000 tpa processing plant which was built in 2011-2012.

This is a BIG mine complex that little HAR has managed to get its hands on.

If HAR is able to build a large enough resource, then it could justify moving into production relatively quickly, without the large capital outlay to re-develop all of this mining infrastructure.

Conventional, simple metallurgy with high recovery rates.

The project is also technically de-risked from a metallurgical perspective. Previous metallurgical test work showed recoveries ranging between 64-99% using fairly common processing methods.

When it comes to metallurgy, simplicity is key.

HAR’s project is a well understood style of mineralisation which has been mined and processed for many decades.

HAR’s geology is well understood by the mining industry and the ASX market

Australian investors understand the type of geology on HAR’s project - high grade vein mineralisation - and understand how to value it accurately.

One of the most profitable mines in the world is the Fosterville mine in Victoria which is a similar deposit style geologically to the type of gold HAR is chasing.

We think that the market will be more open to re-rating HAR if a big enough resource is proven because of the listed examples of successful companies that have worked on this style of geology.

What do we expect HAR to deliver?

Objective #1: Deal completion

We want to see HAR complete the acquisition, raise its cash and issue all of the consideration shares.

Milestones

DD completion

DD completion

Deal completed

Deal completed

Objective #2: Convert existing resource into a JORC resource

We want to see HAR convert its existing non-JORC 286,000 ounce gold resource into a maiden JORC compliant resource.

Milestones

Drill results

Maiden JORC resource

Objective #3: Make new high grade discoveries at priority targets

All of HAR’s current resource is made up from drilling down to depths of ~150m. We want to see HAR drill deeper holes to test for new discoveries/extensions to the current resources.

Milestones

Drilling commences

Drilling results

Objective #4: Upgrade the JORC resource

Once HAR defines its maiden JORC resource (Objective #2 above), we want to see the company upgrade it and bring the overall project resource closer to the targeted longer term 1 million ounce number.

Milestones

Upgrade JORC resource

Objective #5: Bonus Objective - District scale consolidation

We want to see HAR leverage its Conditional Use Permit (CUP) and its existing infrastructure to pick up projects nearby.

Milestones

Deal #1 on new ground/resource

Deal #2 on new ground/resource

Commodity Price Risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract.

Should the gold price fall, this could hurt the HAR share price.

Exploration risk

There is no guarantee that HAR’s upcoming drill programs are successful and HAR may fail to find economic gold deposits.

Funding risk/dilution risk

As a small cap, HAR is reliant on capital markets to advance its projects.

If something negative happens at a macro or company level, HAR could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking HAR’s share price with it.

Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, HAR could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price.

Additionally, if delays occur in terms of material newsflow, the market could turn on HAR.

Production Risk

Should HAR go into production, the ability of the HAR to achieve production targets or meet operating and capital expenditure estimates on a timely basis cannot be assured. As a producer, HAR is subject to risks such as but not limited to, labour costs and availability, energy prices as well as HAR’s internal ability to forecast costs like these and budget effectively.

What is our investment plan?

We are Invested in HAR to see the company make new discoveries and make a decision to mine at the Lincoln project in California.

Our plan is to hold the majority of our position in HAR for 3 to 5 years which we hope is enough time to see HAR achieve gold production (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,570,066 HAR shares at the time of publishing this Investment Memo. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time.

Investment Memo:

Haranga Resources Ltd

(ASX:HAR)

-

LIVE

Opened: 27-Sep-2023

Shares Held at Open: 3,410,000

What does HAR do?

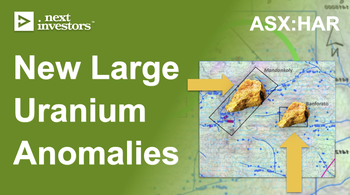

Haranga Resources (ASX: HAR) is a junior explorer defining a uranium project in Senegal, Africa.

HAR owns 70% of its Saraya project, which has an existing JORC resource of 16m Lbs uranium.

What is the macro theme?

Nuclear power has the lowest carbon footprint and highest utility rate of all renewable energy technologies.

Uranium is the primary fuel source for nuclear power, which makes it a critical mineral for a green energy future.

We expect to see uranium production increase across the world, buoyed by the transitions away from highly pollutive base-load energy generation like coal and oil.

Our Big Bet for HAR

“HAR re-rates to a +$100M market cap on significant resource growth and/or a transaction with a major player in the nuclear fuel supply chain”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our HAR Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why did we invest in HAR?

Uranium prices trading at decade highs

Uranium spot prices are recently trading at the highest level in over a decade. Uranium price runs don’t happen often (decades in between) and when they do happen they usually last a few years. The current Uranium run has just started.

HAR has a giant 1,650km2 uranium exploration land holding

HAR’s project is in Senegal, West Africa. While Africa comes with risks, it is one of the rare places where massive new resources can be discovered and deliver multi-hundred million market caps uranium companies (like Paladin Energy, Lotus, Bannerman, Deep Yellow, Aura Energy).

Nuclear giant and reactor builder Areva used to own HAR’s project… twice

The French Nuclear giant owned HAR’s project in the 70’s and ’80s, then again in 2009 to 2011 - they relinquished the project after the uranium price crashed post the Fukushima disaster. Areva did ~62,000m of drilling on HAR’s project.

Existing 16m lbs JORC uranium resource with plenty of exploration upside

HAR’s initial resource released last week is only scratching the surface on its project. Mostly using Areva’s historical 62,000m of drilling, HAR has a further 6 anomalies covering far more ground than the initial resource yet to be tested.

Peter Batten (Ex-Bannerman) just appointed as HAR Managing Director

Peter was one of the founding managing directors for Uranium company Bannerman Energy. In 2006, while Peter was MD, Bannerman was the best performing company on the ASX.

Re-applying Bannerman’s African playbook, HAR to become Bannerman 2.0?

Peter was responsible for taking Bannerman’s African uranium projects from exploration into the feasibility stage. We are hoping he can do it all again with HAR.

HAR has a tiny market cap

HAR seems to have been overlooked by the market at the start of this current uranium run, at ~15c HAR where it last traded, HAR has ~$9M market.

What do we expect HAR to deliver?

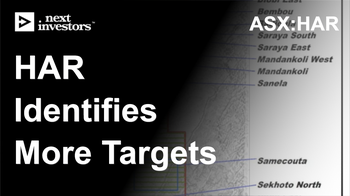

Objective #1: Geophysical/Geochemical surveys across exploration prospects

HAR has six exploration prospects, one of which has a footprint ~5x the size of HAR’s existing JORC resource. We want to see HAR samples and run geophysics over the prospects to work out the best spots to drill.

Milestones

Geophysics/Geochemical surveys

Permitting/planning

Define drill targets

Objective #2: Drilling across exploration prospects

We want to see HAR drill at least two of its exploration prospects.

Milestones

Permitting/planning

Drilling Started

Drilling Results

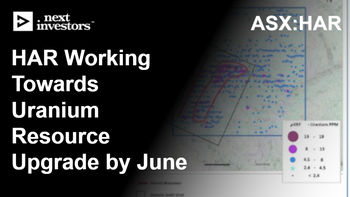

Objective #3: Increase JORC resource

We want to see HAR multiply its existing 16m lb JORC resource.

Milestones

JORC resource upgrade commenced

JORC resource upgrade delivered

Country Risk

West Africa, where HAR’s project is located, is a high-risk region of the world.

Most recently in the region there was a coup in Niger (2023), which coups in Mali (2021) and Burkina Faso (2022) in recent years.

Political instability in the region could disrupt HAR’s ability to operate or commercialise its project.

Exploration risk

HAR is planning to drill exploration targets to grow its uranium resource.

Exploration activities may or may not return any uranium mineralisation or low-grade uranium resource that is uneconomic.

Commodity risk

In recent decades, governments have shunned uranium because of the issues related waste removal and accidents like Chernobyl and Fukushima.

If the adoption of nuclear power is slower than expected then it may impact the future demand for uranium.

Uranium price risk

Share prices of junior explorers like HAR are dependent on strong spot prices for the commodity they are exploring for.

The uranium price has started running at the moment but any retracements in spot prices could lead to capital withdrawing from the sector and a fall in share prices.

Funding risk

HAR is a junior explorer with no revenues to fund exploration and ongoing costs. This means the company is reliant on capital raises to fund exploration programs.

Market risk

If the broader market sells off, investors may shy away from high-risk investment opportunities like junior explorers. During market downturns, investors will look to pull capital away from the high risk investments. HAR is a junior explorer and may be impacted by these market wide sell offs.

What is our investment plan?

As with all our exploration investments, if the share price runs in the lead up to material drilling results, or due to macro or external factors, we may de-risk by Top Slicing 20% of our position.

The rest of the Investment plan depends on the outcomes of the company’s drill campaign and will be updated accordingly, and be governed by the 2 to 3 year holding periods as defined in our trading and hold policy disclosure.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,410,000 HAR shares at the time of publishing this article. The Company has been engaged by HAR to share our commentary on the progress of our Investment in HAR over time. Some shares may be subject to shareholder approval.