YPB expands its anti-counterfeit footprint in SE Asia

Published 02-SEP-2020 12:18 P.M.

|

13 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Chinese demand for Australian manufactured dairy is high and product authenticity is of utmost concern.

However, it is becoming more and more difficult to determine the legitimacy of some dairy products.

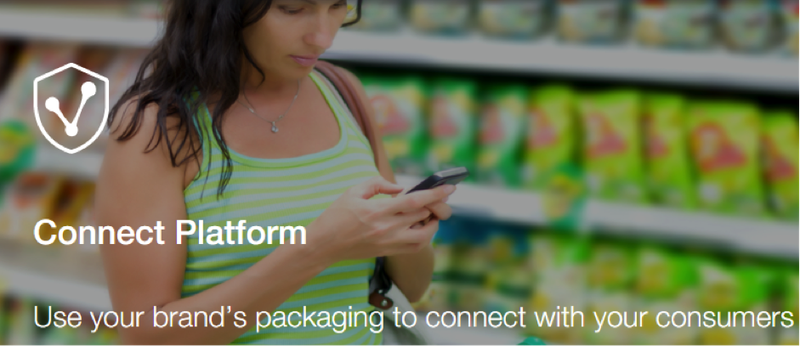

Last year, YPB Group Limited (ASX: YPB) announced it had signed a 2+2 year sales contract with Nature One Dairy for the integration of its consumer engagement and serialised authentication solution, Connect, into its milk powder tins.

The idea was to ensure product authenticity and bring peace of mind to consumers.

That relationship has been going strong.

Nature One Dairy is one of Australia’s milk formula manufacturers accredited by the Certification and Accreditation Administration of the People’s Republic of China (CNCA) for export to China.

Today, YPB announced that follow-up business from Nature One Dairy in Australia has been extremely positive.

The relationship with NATURE ONE DAIRY® has been strengthened with YPB announcing just this week that the group had confirmed the expanded usage of YPB’s CONNECT codes in its regional expansion through South-East Asia.

NATURE ONE DAIRY® (NOD) was YPB’s first dairy sector customer and it is a producer of nutritionally enhanced milk powders, as well as being a contract manufactures for a number of Australian and international retailers.

The group has confirmed that it intends to increase the utilisation of YPB’s CONNECT beyond the initial applications in China and domestically to its new markets of Myanmar, Singapore, Vietnam, Indonesia and Cambodia.

NOD has initially ordered an additional 10 million codes to be implemented over the initial Master Service Agreement (MSA) period.

The group’s South-East Asian expansion takes its product lines into more markets and additional product types such as senior and student nutrition targeted at the Vietnam market.

YPB’s chief executive John Houston highlighted the positive revenue impact from this development in saying, “NATURE ONE DAIRY® is a cornerstone client of YPB’s innovative CONNECT platform and we are delighted to extend our MSA to support its SE Asian expansion. We believe that not only will this add to revenue recognition, but also the awareness of this technology which is easily implemented on production lines to confirm product authenticity and encourage consumer engagement.”

Today’s news comes on the back of improved financial performance for the half year ended 30 June 2020.

YPB’s financial performance improved significantly in the first six months.

The net operating loss of $1.7 million was a 52% or $1.9 million improvement on the first half of 2019, and this could be attributed to timely cost actions that have set the company up with a lean effective cost base.

In terms of managing cash flow and gearing the group’s balance sheet to cope with the challenging conditions, the company was provided with $1.2 million of loans from an entity associated with chief executive John Houston, of which $600,000 was subsequently converted to equity following shareholder approval.

New equity totalling $800,000 was also raised post period end.

As at 30 June 2020, the company held $532,000 in cash and cash equivalents.

More big news this week

YPB's proprietary smartphone enabled technology suite allows consumers to confirm product authenticity and, for brands, that triggers consumers’ engagement.

Being able to identify product authenticity is a critical and more widespread issue than many are aware of, and it tends to be the high profile brands that are targeted with one of the notable examples being the sale of fake Penfolds top shelf wines in China in recent years.

On the score of China, this week’s release of the group’s result comes just days after the company announced two new important contracts in China that incorporate the group’s core technologies, a development that triggered a 25% share price increase.

However, COVID-19 side-tracked management’s execution of the company’s plans the first half.

As budgeted, revenue from Retail Anti-Theft (RAT) was zero during the period following the closure of that business late in the first half of 2019 and was the major factor in the 41% or $244,000 revenue fall compared with the previous corresponding period.

However, COVID-19 also crimped planned revenues, interrupting normal customer ordering and new business development.

On a brighter note, costs were down across the board, falling 52% as reported or down 30% adjusted for exchange rate (FX) movements.

Key factors contributing to the reduced costs included management’s major refocus and reshaping of its operations over the past two years, including further aggressive cost action and temporary staff salary reductions in the half as COVID-19 struck first in China and then in Australia and South-East Asia.

Directors absorbed their share of the pain, cutting fees to zero between April and December 2020 inclusive.

YPB steps up to assist in protecting suppliers and consumers during COVID

YPB has not just being proactive in terms of absorbing some of the COVID-related impact in terms of shareholder returns, but through its state-of-the-art technologies the company has looked to tackle the problem of counterfeit face masks.

Global counterfeiters are taking advantage of the worldwide panic, producing and selling fake face masks and Covid-19 testing kits.

Earlier in the year, Chinese authorities shut down more than 80 shops on e-commerce platform Taobao, run by Alibaba, for selling counterfeit masks, and police found 100,000 fake masks during a raid of an underground factory in Shanghai.

There has also been widespread reporting of the sale and distribution of fake face masks, usually counterfeit versions of the popular N95 variant made by 3M.

US Customs officials uncovered six plastic bags containing fake Covid-19 testing kits in a package sent from the UK on March 12.

However, with the virus showing no signs of slowing down, more fake sellers are likely to surface on e-commerce sites faster than they can be shut down, especially as people continue to stockpile masks or buy thousands at once to send to family and friends in parts of the world that have run out.

To help combat this, YPB is offering manufacturers of both masks and tests their technology free to help control the rapid spread of fake products.

Low sales costs translate into higher gross margins

Harking back to the group’s operational performance, cost of sales or direct product costs also fell significantly to $10,000 from $152,000, again reflecting the product costs of RAT in the prior period.

The mirror image of the low cost of sales was the very high gross margin in the June half of 2020.

The high intellectual property content of YPB’s revenues accounts for the 97% gross margin achieved during the period, up from 75% in the prior period where RAT gross margins of circa 30% dragged down the average.

Very high gross margins are likely to be sustained and are a key element in YPB’s plan to profitability, as profit leverage to revenue growth is extremely high with effectively every incremental revenue dollar falling straight to the profit line.

As revenue growth is achieved, the company’s profitability can improve rapidly as virtually all cost lines were down, many experiencing significant declines.

The biggest contributor to the first half cost fall was lower labour costs (aggregated as consulting fees, director’s fees and employment expenses) down $703,000 or 34%.

This was due in part to staff rationalisation, part permanent salary cuts, part temporary and voluntary salary cuts (April through June) and lower capital raising costs.

The group also received subsidies from the government of local jurisdictions relating to the various COVID-19 financial assistance packages in Australia and China, but the quantum was immaterial at $21,000.

The increase in Directors’ Fees related to active new business development work performed by a non-executive director, and this was paid in the form of equity (performance rights) not cash.

A notable increase in professional fees was driven by unavoidable experts’ reports necessitated by compliance requirements.

Momentum improving in China

The key operational development in the half was further new business momentum in YPB China, despite severe COVID-19 restrictions.

Although the potential is not yet fully proven, YPB China is unearthing significant new interest in YPB’s established T2 tracer-scanner technology driven equally by YPB’s excellent reputation in Tracer technologies and a heightened awareness of the need for product security and provenance.

The China operations were restructured last year with the cost base reduced significantly.

The sales function was more closely integrated with the skilled Australian sales team and new sales strategies and tactics were developed.

A key element of the strategy was to focus almost exclusively on channel partners – major suppliers of parts, packaging and other inputs to major branded consumer goods manufacturers both within China and internationally.

These intermediaries have privileged access to brands and offer leveraged – one to many – market access for YPB.

Key new channel partners were signed in the second half of 2019 and new parties came on board in the June half with management anticipating further new channel partners to emerge in the near term.

Some neglected prior YPB relationships have also been rekindled.

Structured account management, previously a key weakness of YPB, has been instituted and is expected to drive solid recurring revenues from these relationships.

Channel partners provide entry into high-volume industries

Via the channel partners, YPB now has an opportunity to gain access to very high volume industries, and the focus is now on driving volumes significantly higher.

This will take time, but the building blocks are being assembled for significant growth in YPB China.

Importantly, these opportunities relate primarily to the established T2 tracer-scanner technology for maintaining product security in supply chains.

The level of interest is indicating that there may well be a significant opportunity for this technology in China, as was identified at YPB’s inception, and that the conditions for market acceptance are now more favourable.

Importantly, the potentially bigger, consumer-facing opportunity of MotifMicro1 is well advanced in its path to commercial development and trials with PanPass, one of China’s largest security label printers.

COVID-19 has slowed both MM1 technical developments and high volume trials but major progress was made in the June half.

Release of a fully commercial MM1 product is anticipated late in December half, although it may slip into the first half of calendar year 2021.

Nevertheless, the preparation for commercial release and revenue generation from MM1 in China is well-progressed and it is expected to begin generating revenues quickly upon its release.

It is also worth noting that a new sales resource was added in Thailand towards the end of the June half, perhaps paving the way for further opportunities in South-East Asia.

Early progress in new business development has been encouraging and may bear fruit in the coming months.

During the June half, an innovative MM1 high security shrink wrap was developed with OPP Gravure Printing Co. Ltd in Thailand.

Further development activities have been severely hampered by COVID-19 in Thailand, but mutual interest remains in developing the relationship further.

Major advances with Connect and MotifMicro1

YPB has also made significant progress on the technical front particularly with its Connect and MotifMicro1 products.

In the June half, the new generation Connect 2.0 consumer engagement platform was released.

It is a newly architected, user friendly, lower cost of operation product that went live during the period.

The migration of existing customers from Connect 1.0 to 2.0 is ongoing and this is expected to result in lower hosting and other operating costs for YPB once the migration is completed by the end of 2020.

Major progress was also made on MotifMicro1 smartphone readability, culminating in the announcement on July 27 that the critical technical milestone of Android smartphone readability of the proprietary MotifMicro1 particle had been achieved.

Importantly, this technical step was also a key commercial milestone, with the addition of Android functionality to the existing iOS capability of MotifMicro, a major technical hurdle on MotifMicro’s commercial development path.

The Android capability is included in the second generation MotifMicro1 APP which was also released at the end of July.

Smartphone readability development is highly dependent on Artificial Intelligence skills and capacity, and our Bangkok team has advanced capabilities in this area.

COVID hangover remains, but December quarter growth is a prospect

COVID-19 and its aftermath continue to make estimating the timing of new sales revenues and cash receipts unusually difficult.

Nevertheless, present indications are that December half revenues should stabilise at June half levels, and possibly grow, but with a heavy weighting towards the December quarter.

The range of possible outcomes is wide and dependent on ‘normality’ resuming for YPB’s customers and their ordering patterns, as well as the timing of new business wins that in some instances are still being hampered by COVID-19 restrictions.

Costs are likely to rise somewhat in the December half as the temporary COVID-19 salary reductions ended on June 30, 2020.

However, other cost items are likely to remain relatively flat and will remain tightly managed.

Changed work practices across the business community will permanently reduce a range of costs and improve staff productivity.

Discussing the result and the group’s outlook for the remainder of the year and into 2021, Houston said, “H1 2020 demonstrates that YPB is heading toward becoming a successful, self-funding business.

‘’Our product suite is now diversified and commercially robust, and we have developed a cost effective yet highly skilled tech team in Bangkok.

‘’Our sales strategies and staff are at a new level of professionalism, and our cost management is very tight with the new norms of remote work and meeting permanently reducing a range of costs.

‘’YPB China’s market development progress with our established T2 tracer-scanner is very encouraging and it is possible that T2 in China alone could underwrite the company’s profitability should we be able to build further momentum in that business over time.

‘’As MotifMicro1 approaches commercial release, our market opportunity balloons many fold as it will be a globally unique, high-security, product authentication technology for the much larger consumer market.

‘’Market entry is well planned with early adoption partners in both China and Thailand established.

‘’Further, MotifMicro’s possible applications are only limited by imagination, and licensing MotifMicro1 for specific industries and geographies remains an important plank of the plan to realise its true value (although not in active development presently).

‘’Finally, I’m proud of and grateful for the dedication and sacrifices of our staff during COVID-19, and the whole team is intent on making YPB the success we know it can be.”

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.