Will Australia lose its Triple A rating?

Published 03-JUN-2016 10:08 A.M.

|

1 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

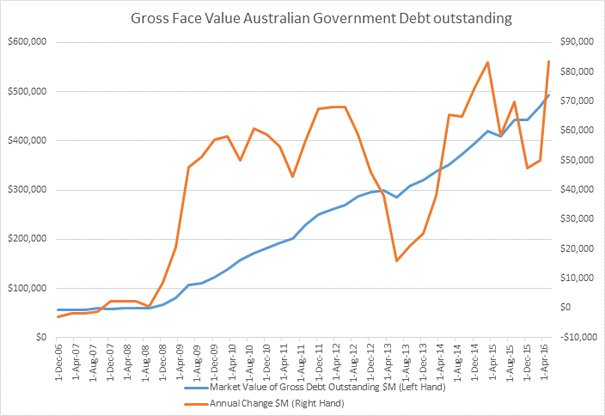

As of 30 May 2016, the gross market value of Australian Government Debt outstanding is about $493.5 Billion writes Mike Cornips, Director at Options Educator, TradersCircle.

The annual increase in the level of debt bottomed in June 2013 at about $16 billion, but peaked in March 2015 at $83.2 Billion. Over the past couple of months, we have seen an increase to an annual $83.7 Billion.

It is better to look at the level of the market value of debt rather than the face value of debt to ascertain the level of Government borrowing to fund the deficit. The media tends to focus on the face value of the debt but if the Government issues $1 million of Bonds with a maturity of 21st April 2027 with a coupon of 4.75%, it doesn’t receive $1 million, it would receive $1,234,000 (23.4% more). This happens because the market price (ASX code: GSBG27.ASX) is $123.47, not $100.00. Because the regular coupon payment is 4.75% and the market interest rate is 2.31%, the market is prepared to pay more than $100 today because coupon payments are higher than the current rate of interest.

The media has been commenting on the ballooning debt issue in the context that both major parties are no longer focusing on the debt and deficit disaster. Currently our level of debt appears quite manageable considering $500 Billion is “only” about 30% of GDP. The problem is that the annual growth of debt (over 5% of GDP) is greater than other AAA rated countries.

The issue then is not whether Australia can afford the debt (it can), but whether the external rating agencies lower our coveted AAA credit rating. Any incumbent Government that has the rating lowered during their term of Government will certainly cop a nose bleed in terms of fiscal responsibility.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.