Volt bags offtake deals in China

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Volt Resources (ASX:VRC) has plugged into the growth of lithium-ion battery production in China, signing three non-binding offtake deals to the tune of 100,000 tonnes of graphite per annum.

It told its investors in a note today that it had managed to bag three separate non-binding memorandum of understandings with three Chinese companies – all of which manufacture lithium-ion batteries.

Combined, the three MOU’s equate to 100,000 tonnes of graphite per annum from the company’s flagship Namangale project in Tanzania.

The three non-binding deals lay the groundwork for detailed test work with an eye towards wrapping up binding offtake arrangements.

The three companies are Optimum Nano, Huzhou Chungya, and Shenzhen Sinuo – with the former of the trio the second largest producer of lithium-ion batteries in China.

It has supplied 80,000 electric vehicles with lithium ion batteries to date – specialising in providing batteries to electric buses and trucks.

VRC said a recent Benchmark Intelligence report indicated that despite 100% of the natural spherical graphite being produced in the country and production expanding at nearly 50% last year – there are fears that emerging players such as Tesla could make supply scarce.

“What is abundantly apparent is the incredible expansion plans that are taking place in the lithium-ion battery industry within China,” VRC executive chairman Stephen Hunt said.

“Signing the MOUs is a very significant step in the marketing process and positioning ourselves to be at the forefront of graphite supply.”

In other VRC news, it confirmed that it had managed to bag $4 million from a placement of 40 million shares at 10c each before costs – a price which is a 29.6% and 12% premium to the company’s 30 and 15 volume weighted average price respectively.

The placement was made to “a strategic institutional investor” – demonstrating the corporate appetite for graphite companies as the likes of Telsa continue to make waves in the lithium-ion battery market – and subsequently the raw material market.

Last month it managed to bag the services of Edward Sugar-backed EAS Advisors to help tap investors in North America.

Sugar has a track record of investing in early-stage ASX-listed resources plays, having participated in deals worth a cumulative $US3.5 billion ($A4.8 billion) to date.

The offtake agreements come despite the company not having yet completed a pre-feasibility study at its Namangale project – with the company confirming today that a pre-feasibility study would be completed in the fourth quarter this year.

If nothing else, the non-binding MOUs with Chinese manufacturers will give investors greater certainty around the demand-side for graphite from the project.

More on Volt Resources’ Namangale project

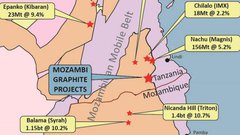

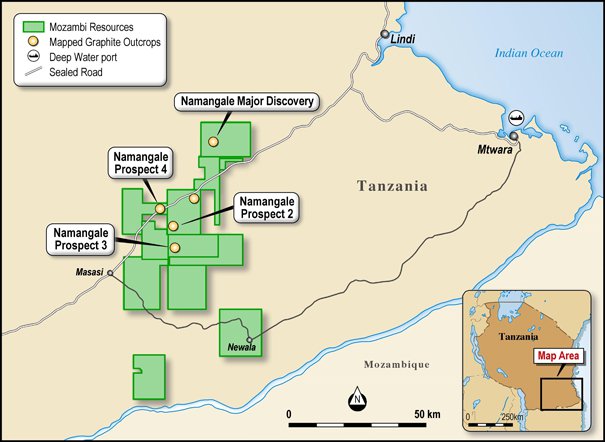

The project is one of the largest in Tanzania, with a JORC compliant inferred resource of 179 million tonnes at an average grade of 5.1% total graphitic content.

MOZ’s Tanzania operations are located close to the deep-water port of Mtwara, 140km from the Namangale Prospect.

Location of the Nachingwea Project tenements, including Namangale project (ex-Mozambi Resources)

Sealed roads and high-voltage are available across its prospects, connecting MOZ to export routes internationally.

Mtwara Port has a capacity of 400,000 metric tonnes per year and could handle up to 750,000 metric tonnes per year with the same number of berths if additional equipment is put in place for handling containerised traffic.

The port is currently heavily underutilised, with approximately 34% of its total capacity currently in use.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.