Talon sinks its teeth into fourth North Sea asset

Published 05-JUN-2019 10:46 A.M.

|

3 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

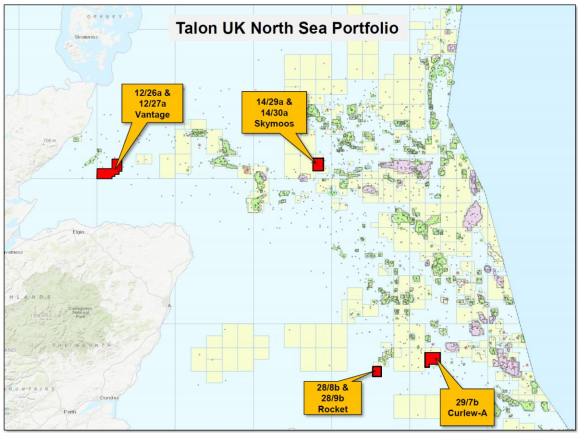

North Sea oil and gas group, Talon Petroleum Ltd (ASX:TPD) has been offered a 50% interest in a licence over Blocks 12/26a and 12/27a in the North Sea via the UK 31st Offshore Licensing Round.

Talon undertook some company transforming initiatives in the March quarter as it entered into a binding heads of agreement for the purchase of all of the shares in EnCounter Oil Ltd.

The transaction provided the company with 100% ownership of two recently awarded, high-impact exploration licences in Skymoos and Rocket.

The newly awarded licence is the fourth UK North Sea asset acquired by Talon since the company embarked on its UK North Sea strategy in mid-2018.

The acquisition also provided additional benefits with Talon gaining access to a significant technical database and a highly-experienced UK North Sea management team with previous exploration success.

That technical team includes Graham Dorè and Paul Young who importantly also have an intimate knowledge of the licences offered.

Discussing these advantages and the strategic importance of the blocks in terms of the company’s broader strategy, Talon managing director, Matt Worner said, “We are extremely pleased to add another highly prospective licence to the Talon portfolio.

“This new licence includes the Vantage Prospect, which was identified by Talon’s technical team, Graham Dorè and Paul Young.

‘’The award of this licence shows we are delivering with our strategy to capture low-cost, high upside drilling targets via the regularly held UK Licensing Round process.’’

Further licences in pipeline and farmout imminent

Talon has recently applied for another licence in the 31st Supplemental Round and will shortly commence its consideration of licence areas proposed to be available in the 32nd Seaward Licensing Round, for which bids are due in late 2019.

In relation to the company’s established assets, Worner said “Additionally, we have started the farmout process for our Rocket and Skymoos prospects and we have received encouraging interest at this early stage.”

The new licence contains the Vantage Prospect, an Upper Jurassic stratigraphic trap updip of a known oil discovery well located within the licence area and contains a best estimate prospective resource of 44 million barrels of oil (mmbo).

Based on normal risking methodology used in the oil and gas industry, an estimated probability of commercial success for the Vantage Prospect, after all technical work has been completed, is expected to be in a range between 20% and 30%.

Interestingly, Talon jointly applied for the licence with Geoscience Services Limited (GSL), a company of which Dorè and Young are directors.

The bid for the licence was made prior to the company entering into the transaction with EnCounter Oil Limited, which brought Dorè and Young to the Talon team.

Building an impressive portfolio of assets

In addition to the newly awarded licence, Talon’s portfolio now includes a 10% participating interest in the Curlew-A discovery (Licence P2396) which contains 2C contingent resource of 45mmbo.

The company also has a 100% participating interest in two licences with a combined best estimate resource of 134 million barrels of oil equivalent (mmboe).

These are the Skymoos (licence P2363) and Rocket prospects (licence P2392), the locations of which can be seen below, with the Vantage prospect lying to the west of Skymoos.

Work program commitments for the initial two-year phase of the licences include poststack processing of 500 square kilometres of existing 3D seismic data and the acquisition of 150 line kilometres of existing 2D seismic data.

Management expects its share of the costs based on its 50% interest is approximately $60,000.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.