Santos/Total decision could double Melbana’s share price

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

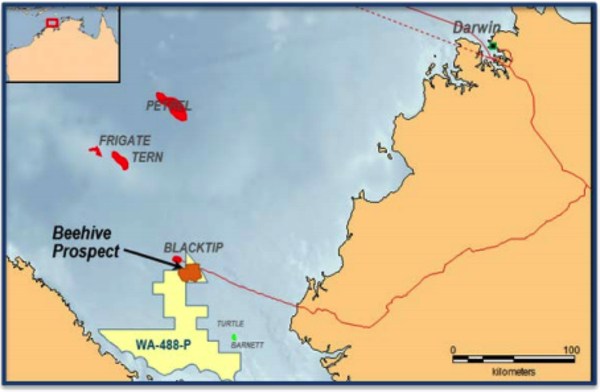

Hartleys oil and gas analyst, Aiden Bradley ran the ruler across Melbana Energy Ltd (ASX:MAY) this week, making some interesting observations regarding various recent developments and flagging the upcoming decision by Santos and/or Total to drill an exploration well in the group’s Beehive prospect (WA-488-P), offshore Western Australia.

While acknowledging that the termination of Melbana’s farmout agreement for Block 9 in Cuba, along with the departure of the group’s chief executive officer had created negative investor sentiment, essentially placing downward pressure on the company’s share price, Bradley sees the potential for a substantial recovery.

In fact, Bradley’s price target of 2.2 cents implies 100% upside to yesterday’s closing price of 1.1 cents - however this is speculative.

Bradley sees the decision regarding Beehive as the main catalyst for a rerating.

Indeed, a decision by Santos and/or Total to drill an exploration well should increase the value attributed to Beehive.

Melbana free carried for US$50 million drilling program

In terms of the proposed farmout agreement, Melbana will have a fully carried interest in an exploration well estimated to cost approximately US$50 million, a coup for a company with a market capitalisation of $20 million.

Should a decision be taken to drill the well, Melbana will still have a 20% interest in an asset with a best case recoverable prospective resource of 388 million barrels of oil equivalent.

However, the 2 October deadline for the formalisation of the agreement looms large, and there is a real ‘will they, or won’t they’ question mark hanging over Melbana.

It could be argued though that an affirmative decision isn’t factored into the share price, and in terms of weighing up the pros and cons of a green light, Bradley is of the view that the case for drilling the well is ‘quite strong’, citing the size of the potential resource.

This underpins the broker’s speculative buy recommendation he has attributed to the stock.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.