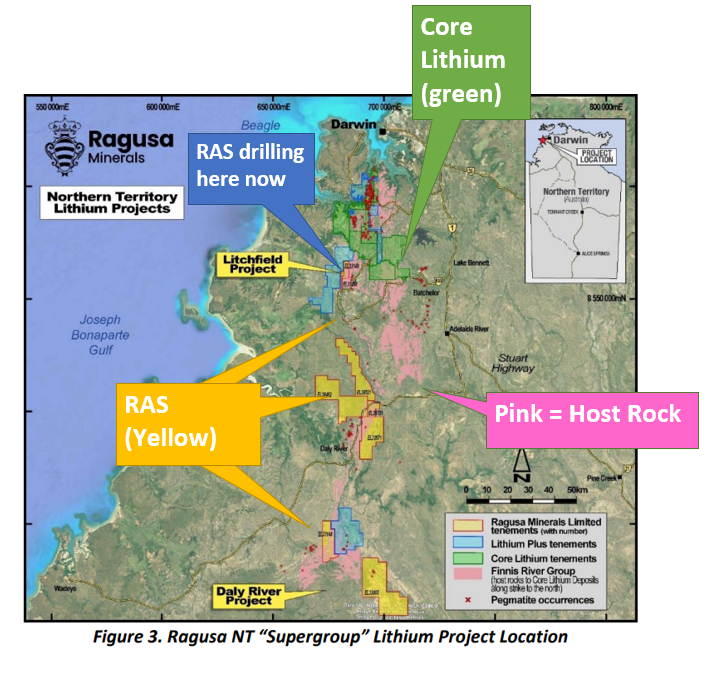

RAS now drilling to the south of $2.1BN capped Core Lithium

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,500,000 RAS shares at the time of publishing this article. The Company has been engaged by RAS to share our commentary on the progress of our Investment in RAS over time.

Our small cap exploration Investment Ragusa Minerals (ASX:RAS) has just started drilling for lithium in the Northern Territory.

The $36M capped RAS’s lithium project that it is drilling now is immediately south of the $2.1BN Core Lithium deposit - and sits on the same type of geology.

RAS’s first drill hole has already been completed - and managed to hit a 35m downhole intercept of pegmatite recorded from just 16m depth below the surface.

RAS has the same type of outcropping spodumene bearing pegmatites that Core identified before it drilled out its project.

This is important because spodumene bearing pegmatites are the host rocks for almost all of the hard rock lithium production globally.

Another important part to the RAS story is managing director Jerko Zuvela’s previous lithium exploration success - Jerko helped take Argosy Minerals (capped at $654M) from explorer to late stage development and we’re hoping he can do a similar thing with RAS.

The pre-drill work completed to date has been behind RAS’s share price rising from ~6c to a high of 44.5c per share.

With the company’s share price coming off a bit from its recent highs to ~28c ( ~$36M market cap), good drilling results could be the catalyst for its next rerate.

Over the coming weeks we are watching for visual spodumene intercepts during drilling and then lithium above typically economic grades in assays.

So how did RAS get here?

It was only a few months ago that RAS started acquiring and pegging its lithium ground, targeting the same style of geology that Core Lithium’s 18.9Mt JORC lithium resource sits on.

The previous owners of RAS’s project detailed “several distinct trends and many kilometres of untested strike length of pegmatites occurring within the leases” in 2018.

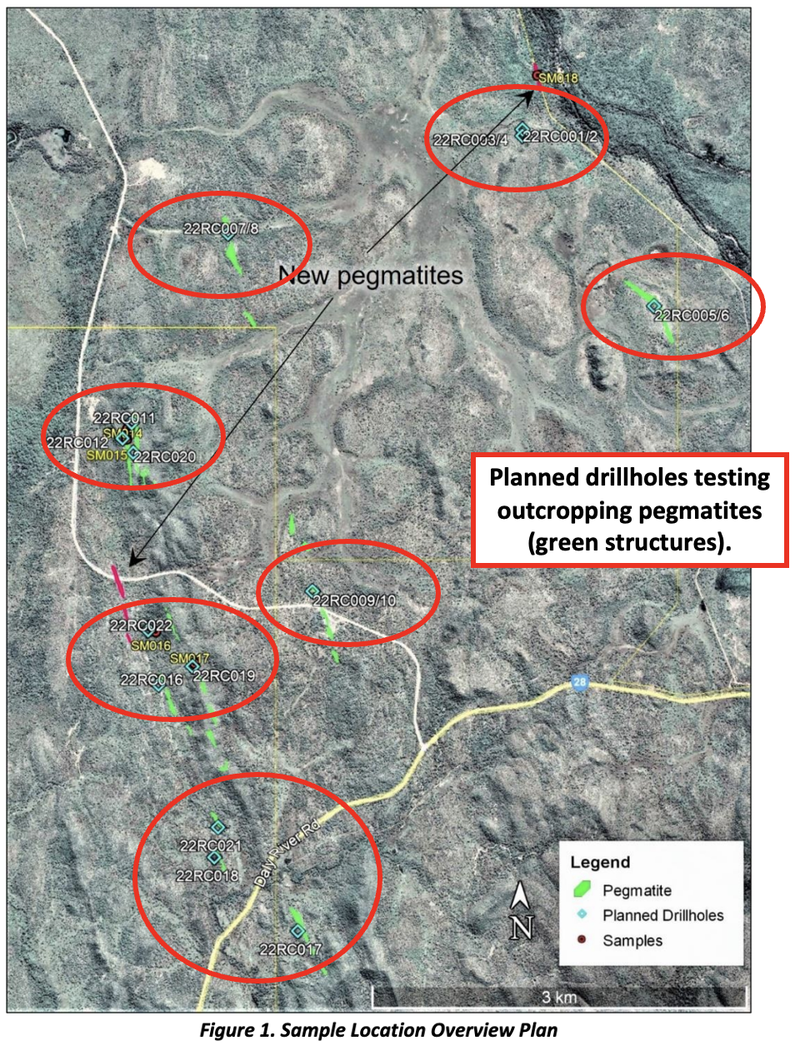

RAS now has untested outcropping pegmatites that have returned rock chip grades of up to 8.01% lithium and 23.1g/t gold, measuring up to ~30m in width at surface.

On top of all of this, it has also recently confirmed spodumene bearing pegmatites.

The presence of spodumene is particularly important because it is generally the host rock for lithium in a majority of the world's already operating hard rock lithium projects.

Where there is spodumene, the probability of making a high grade lithium discovery increases.

As it stands, Core’s market cap is over ~60 times larger than RAS’s, and we are hoping that RAS’s current drilling program is the first step towards changing this ratio for the better.

- Core Lithium (capped at $2.1BN) - Progressing its JORC 18.9 million tonne lithium resource into production.

- RAS (capped at $36M) - Has not defined a resource or discovery but is drilling right now.

With drilling now underway, we hope RAS’s MD and biggest shareholder Jerko Zuvela can do something similar to the success he achieved (and continues to achieve) with Argosy Minerals (currently capped at $654M) - and that is by taking RAS from an early stage explorer to a lithium player with a well defined resource.

We think that with the lithium market continuing to be strong, if RAS does make a new lithium discovery, then the company’s market cap could rerate significantly.

This is central to our “Big Bet” for RAS.

Our ‘Big Bet’

That RAS will return 10x by discovering and defining a significant enough deposit to move into development studies for one of its projects.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our RAS Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

For our summary of RAS’s progress over time and how today’s announcement contributes to our Big Bet see our RAS progress tracker.

More on RAS’s lithium drilling:

The lithium exploration playbook is relatively simple.

RAS already has:

- Fieldwork and pegmatites mapped - RAS has completed fieldwork mapping out the outcropping pegmatites at its project (some of which measure as much as 30m wide).

- Geochemical sampling completed - Rock chips taken with lithium grades of up to 8.01%, and gold grades of up to 23.1g/t.

- Spodumene bearing pegmatites found - RAS has found spodumene bearing pegmatites which are generally a precursor for economic lithium mineralisation.

All that's left now is to drill the targets that RAS has put together.

Below is a map of the targets RAS will be drilling.

The GREEN represents the outcropping pegmatites, and the RED circles where RAS will be drilling.

We are hoping RAS finds similar style success to our other portfolio company Latin Resources, which made a similar style spodumene hosted lithium discovery at its Brazilian project earlier this year.

Below is the market's response to Latin Resources’ discovery, which saw the company’s share price go up by almost 1,000%.

If RAS can deliver similar drilling newsflow, there may be a chance of a similar re-rate in the company’s share price.

How will RAS pay for the drilling?

RAS last reported a ~$2.5M cash balance (as at 30 June 2022) - plenty to run a drill campaign.

Our ideal scenario is a less risky version of what Latin Resources achieved after going into a maiden lithium drill campaign with just $643k in the bank and some in-the-money oppies, delivering excellent lithium results, then raising $35M off the back of the resulting share price run.

The less dilutive raise at a higher post-discovery share price turned out to be a great result for shareholders.

We want to see is the RAS share price re-rate off material initial drilling assays, then execute a less dilutive raise at the higher share price, enough to fund the next few drill campaigns.

Obviously the condition precedent on this ideal scenario is a lithium discovery - which will solve capital raising problems one way or another.

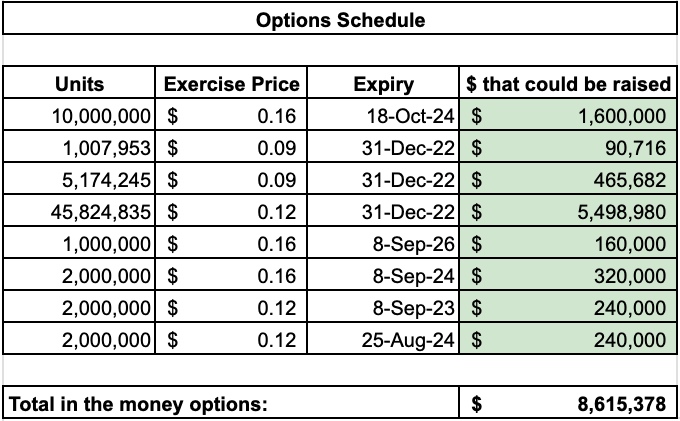

We also note that RAS has ~70 million options that are all in the money at the current RAS share price.

If these “in-the-money'' options were to get fully exercised, RAS would bank ~$8.6M.

(you can track the current cap table and options schedule for any of our portfolio companies in our cap table tracker here)

With a large portion of these expiring on 31 December 2022, there are only 3 full months left before they expire UNLESS the holders convert the options into shares.

Given that, RAS might hold out on raising capital until holders start converting them.

As with all of our exploration Investments, we like to see the company go into maiden drilling programs like RAS’s with a strong balance sheet so that if the results come back negative, the company has enough cash to do some more target generation work before looking to drill again.

In any case, we think a capital raise, whether it be through option exercises or a placement, would be a good move by RAS.

What’s next for RAS?

Drilling results 🔄

With drilling now underway we will be watching for the following:

- During drilling - We want to see visual spodumene. Spodumene is generally the host rock for high grade lithium, any visuals could be a sign RAS has hit economic lithium mineralisation.

- After drilling - This will be all about waiting for the assay results. Here we will be looking for lithium grades above a level that is considered typically economic.

We have set up expectations for the assays as follows:

- Bull case (Exceptional result) = Lithium grades >1.5%.

- Base case (Good result) = Lithium grades >1%.

- Bear case (Poor result) = Lithium grades <1%.

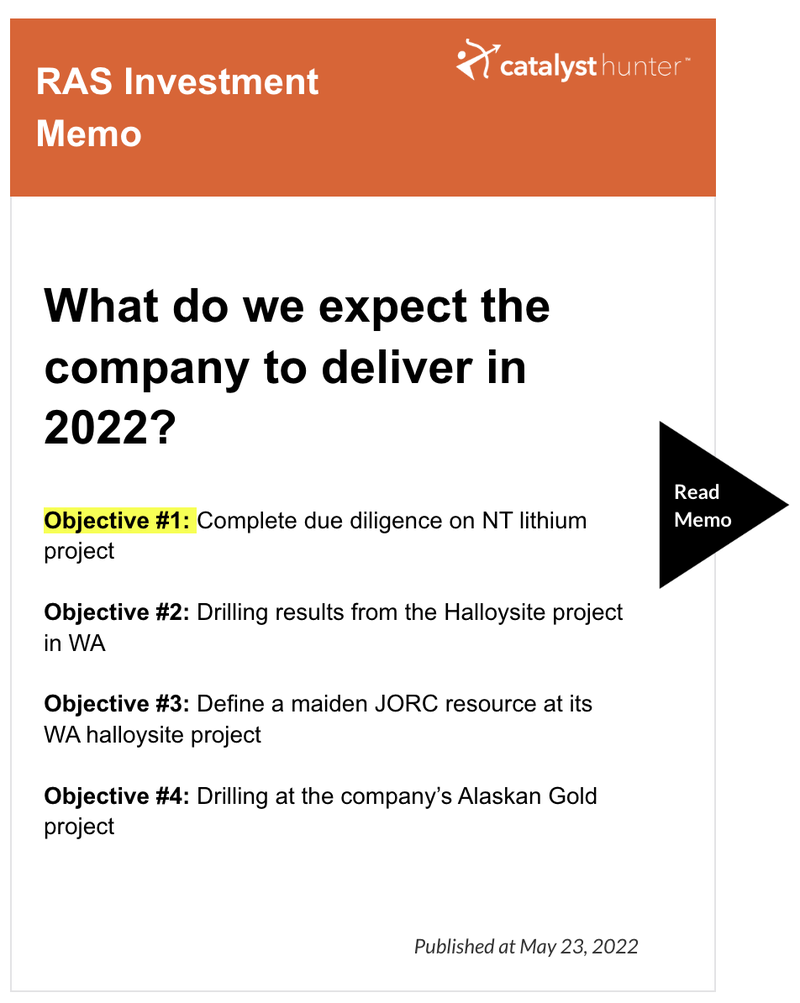

Our 2022 RAS Investment Memo

Today’s news contributes to key objective #1 of our RAS Investment Memo.

Below is our RAS Investment Memo, where you can find a short, high level summary of our reasons for Investing including the following:

- Key objectives for RAS for the coming year

- Why we are Invested in RAS

- The key risks to our Investment thesis

- Our Investment plan

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.