Our Latest Investment: Rare Earths Exploration

Disclosure: The authors of this article and owners of Catalyst Hunter, S3 Consortium Pty Ltd, and associated entities, own 12,823,582 FNT shares at the time of writing. S3 Consortium Pty Ltd has been engaged by FNT to share our commentary on the progress of our investment in FNT over time.

At Catalyst Hunter, we believe the green energy transition is the most compelling investment thematic of the decade.

This energy transition thematic is in the process of catapulting two previously forgotten rare earths elements into the limelight.

Readers of our other portfolio “Next Investors” will know that exposure to critical metals for the world’s energy transition is behind many of our most successful investments to date - Vulcan Energy Resources (current return 4,820%), Euro Manganese (417%) and Kuniko (398%), to name a few of the highlights of our investing journey.

While past performance isn’t an indicator of future performance, we are trying to replicate this success at Catalyst Hunter by investing in more critical battery metals companies.

Today, we’ve made an investment in an area that is getting an immense amount of investor attention in the new energy metals space - rare earths.

While there are 17 different Rare Earth Elements (REE) - we have focussed on two in particular - Neodymium (Nd) and Praseodymium (Pr).

These two particular rare earths are crucial to creating the permanent magnets used in Electric Vehicles and wind turbines for clean electricity.

The battery metals and clean energy theme just keeps getting stronger, so we’re looking to replicate our past successes and gain exposure to all the metals required for the green energy transition.

Which is why today, we’re adding this Rare Earths Explorer to our portfolio:

Over the last 12 months, we’ve been patiently waiting to find the right investment to capture exposure to rare earths - exposure that is aligned with our investment methodology.

If you’ve been watching the market like we have, you’ll have seen the share price rises on a number of rare earths companies.

Driving this share price action is a combination of forces. Here’s the quickest rundown of the story possible:

- Rare earths, in particular Nd and Pr, are essential to the energy transition

- Nd and Pr are essential to the manufacture of permanent magnets found in both EVs and wind turbines

- China makes up the majority of rare earths production

- With tensions between the West and China running high, government and investors are quickly seeking out alternative sources of rare earths.

As far as investment thematics go, this is one of the most simple and powerful we’ve ever seen. More on what NdPr is and why it matters to follow... first let's look more at where FNT sits and who is next to them.

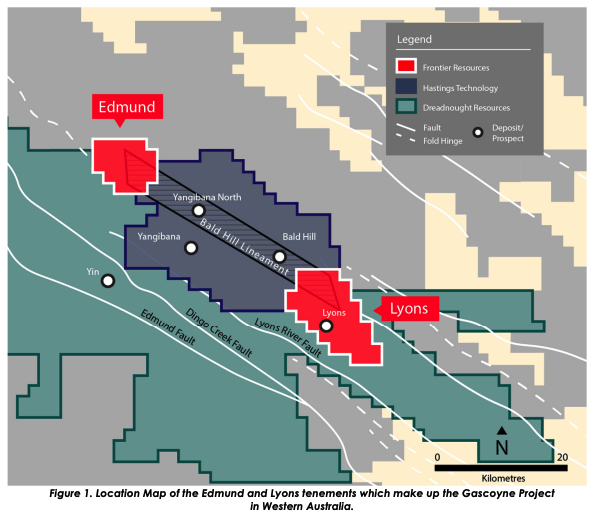

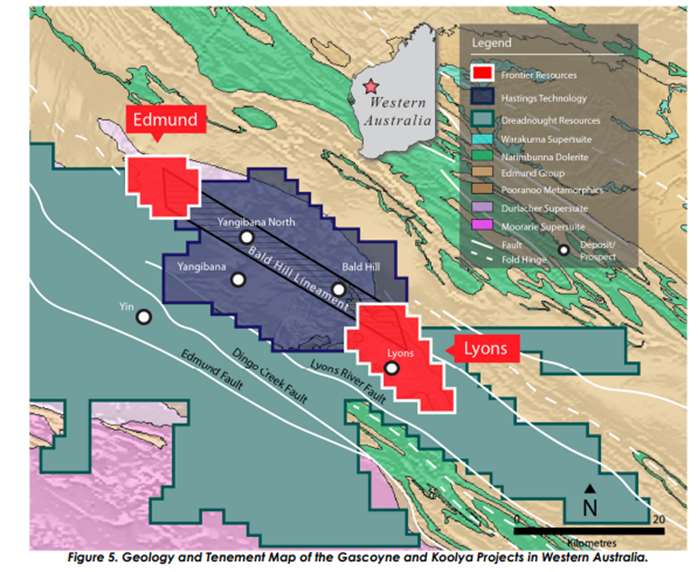

Frontier Resources (ASX:FNT) is exploring for rare earths primarily in the Gascoyne region, WA.

FNT’s ground is located directly either side of ~$500M market capped Hasting Technology Metals’ which owns an advanced rare earths project - check it out on the map below.

The Hastings rare earths project is likely to go into production in 2023 and boasts the highest grade of NdPr of its ASX-listed rare earths peers.

Last week Hastings’ received a $140M loan from a Federal Government Fund to help bring its rare earths project into production - this is a huge signal that Australia is very keen to shore up more local, reliable sources of rare earths.

In addition to literally being next door to Hastings’, FNT’s tenements also border those of Dreadnought Resources, another explorer - which is capped at ~$122M - over four times the size of FNT.

Here you can see the positions on the map below - FNT is in red, either side of Hastings, and Dreadnought is the paler blue region around FNT and Hastings:

What stage is FNT at right now

FNT is currently waiting on EM survey results, and we are hoping some drill targets will be identified in this process.

With $5M in cash, and assuming some interesting drill targets are found, we think FNT has enough cash to carry out a maiden drilling campaign on this ground.

From the outset, we need to make it clear that our latest addition to the Catalyst Hunter portfolio is definitely on the higher end of our risk spectrum - this is early stage exploration and the stock has seen a lot of buying in recent days.

In terms of share price action, FNT started moving quickly in recent days prior to our investment.

We think the recent days trading activity we think this could be due to a number of factors:

- anticipation of the EM survey results (which the company previously said are due in late January),

- the hiring of new Chairman David Frances, which we know well from our investment in Province Resources (ASX:PRL) - an investment that worked out well for us, and;

- Hastings’ $140M loan deal struck with the Federal Government’s facility - which shone a spotlight on the region - including Hastings next door neighbour, FNT...

The result of all this has meant that our entry price on this one is slightly higher than if we had invested in say mid January.

We invested now as even though the stock appears to have re-rated from a few weeks back, we still like the upside at these levels ahead of the EM survey results and drilling.

We reiterate that this is a highly speculative early stage exploration play - the company is yet to define any drill targets, much less go and drill them. It is early days, and we may even see temporary lulls in the share price between now and any drilling event.

Given the early stage nature of this exploration, it also means we have a number of key catalysts in the near term pipeline - something we highlight in our FNT Investment Memo:

The upside potential for us is definitely in play still given drilling is yet to commence pending a successful EM survey that generates firm drill targets.

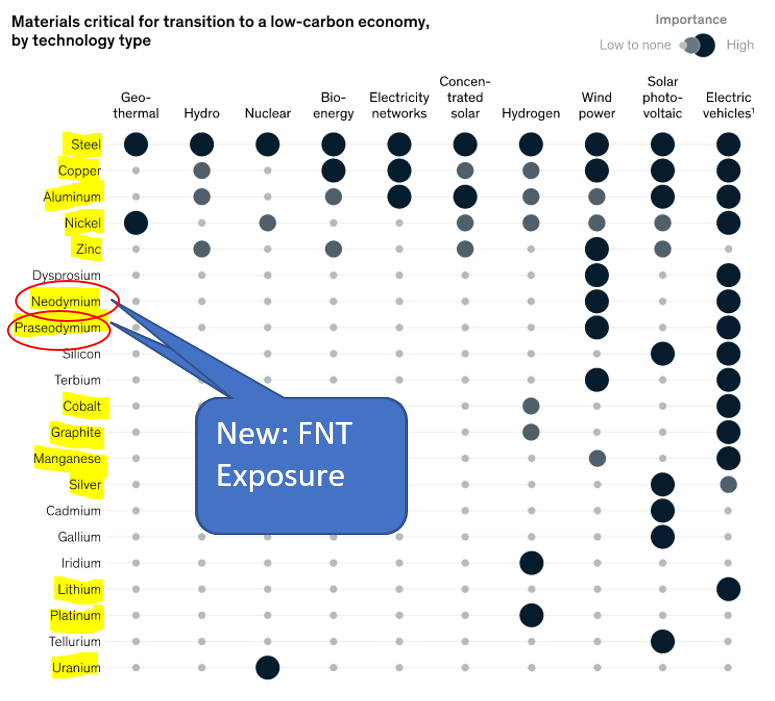

Our investment in FNT is now part of a clearly defined strategy for us - to get exposure to all the raw materials on the “energy transition” list from McKinsey below, we have investment exposure to those highlighted in yellow:

The final seven “un-highlighted” elements are still on our wish-list (please respond to this email if you know any listed or private companies with projects in Dysprosium, Silicon, Terbium, Cadmium, Gallium, Iridium or Tellurium)

We believe the energy transition will be fueled by these critical raw materials - making for one of the most powerful investment themes of the coming decade.

Over the past 12 months we’ve been looking to add rare earth exposure to our portfolio, and were close on a number of occasions.

With FNT having key catalysts in the pipeline, we now have that exposure and we believe it is well suited to the Catalyst Hunter portfolio.

Here’s how we’ll proceed for the rest of this note here is what we will be looking at:

- The macro forces driving rare earths investment

- Where FNT’s ground sits, and why it's geology could lend itself to a discovery

- Why we invested in FNT

- Key objectives for FNT

- Key risks

- Our FNT investment plan

To get a quick high-level summary of each of these points, simply click the link below to get our FNT Investment Memo:

Macro forces driving rare earths investment

FNT is part of a broader macro theme that we’re seeing play out right now.

The quick explanation of this thematic is that as of 2021:

- China accounted for 60% of global rare earths production.

- The West is moving quickly to secure the supply chain and produce their own rare earths.

- These rare earths are critical to the energy transition.

We want to share with you important historical context around rare earths because our FNT investment thesis has macro analysis at its core.

That historical context stretches back to 2011 - when the last rare earths boom played out in the market.

At the time, China made up 95% of global rare earths supply and was threatening to impose an export ban on rare earths.

It set off a speculative frenzy that took one US miner Molycorp Inc. to a market cap of US$6B and Australian mining company Lynas Corp from $5 to more than $24 in the space of 8-months from a previous low in 2009 of ~50¢.

Molycorp subsequently went bankrupt in 2015 and the Lynas share price languished below $1.00 and the company was on the brink, just like Molycorp.

Today, Lynas is trading at a $9.55 share price, with a market cap of $8.6 billion.

Wary of the past, rare earths sceptics might ask “why is this time any different than last time?”

To answer that question, our macro analysis has led us to believe that this is not a repeat of 2011s’ speculative frenzy.

Rather, rare earths are now part of a multi-year pivot towards energy transition raw materials.

And FNT could be part of that energy transition should it discover Nd and Pr.

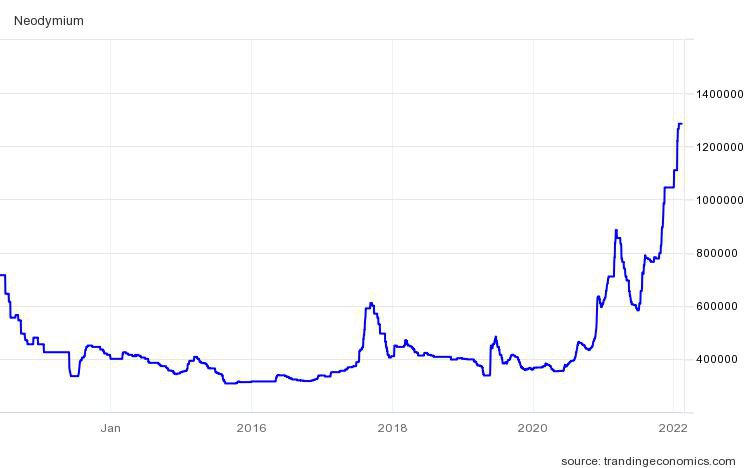

To support this thesis, and explain why this isn’t a 2011 boom and bust all over again here is what we call “Exhibit A”: the Neodymium (Nd) price chart:

Equity research that we’ve sighted shows a strong correlation between Nd and the other rare earth (Pr) we’ve got exposure to via today’s FNT investment (assuming they make a discovery of course).

We think that trend will continue, because unlike in 2011, there is a demand dynamic that wasn’t present - EVs and wind turbines which need permanent magnets made up of Nd and Pr.

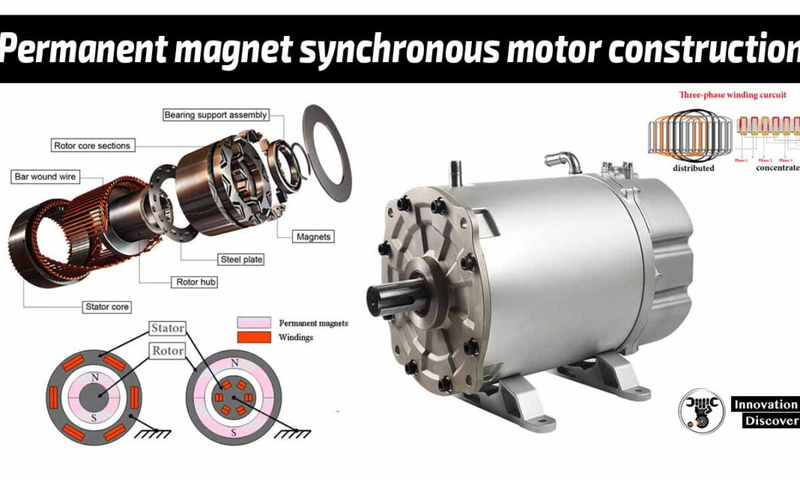

These magnets look like this:

Since the discovery of rare earth based permanent magnets in the 1960s, the number of these magnets is poised to go exponential in an EV future.

And the neodymium (permanent) magnets in a typical EV weigh up to 3kg.

But for us the real story is wind power because a single wind turbine uses around 1000kg of rare earths. Particularly Nd and Pr.

You’ve seen the exponential EV demand growth charts before, but wind turbines get less of a look in.

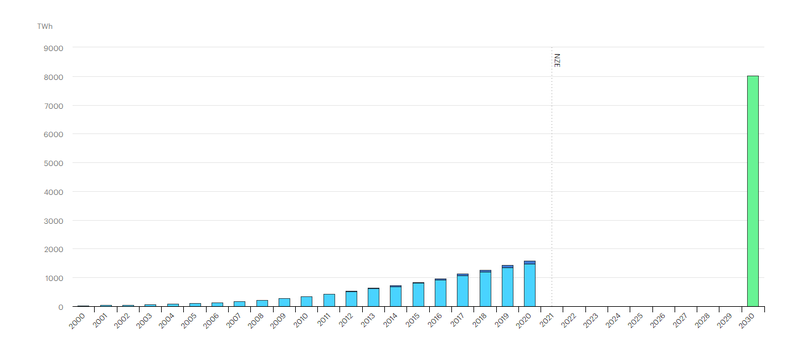

Which brings us to Exhibit B in our rare earths thesis:

That big green bar on the right is the amount of wind turbines needed to hit net-zero by 2030, a six-fold increase in installed capacity.

Now, net-zero by 2030 is unlikely, indeed most countries have committed to net-zero by 2050, but it gives you a sense of wind power’s prominent role in the energy mix going forward.

Combine Exhibit A, and Exhibit B and you have a compelling macro narrative around rare earths like Nd and Pr, something that should play into the hand of FNT.

Where FNT’s ground sits, and why it's geology could lend itself to a discovery

It would be easy to simply classify FNT’s prospects as another riff on basic nearology investing - “small company next to bigger company means small company might get bigger”...

.. but what’s clear to us, is that the particular part of the Gascoyne region that FNT is aiming to explore is an emerging rare earths district, and a place where the source rocks may not even have been found yet.

Put another way, aside from location alone, think the geology of the area and its unexplored nature lends itself to further discoveries.

FNT’s tenements are wedged either side of Hastings’ $500M Yangibana project and directly to the north and contiguous with Dreadnought’s tenements:

Not all “nearology” is created equal

We have written before about there being levels to “nearology” plays.

Too often in the exploration space, companies will come in after a discovery is made, peg whatever grounds they can get their hands on next to a major discovery, and then go and try to raise capital off the back of this.

Just because a company has some ground nearby, doesn’t mean that ground is valuable OR that being next door to something will mean anything.

After talking rocks with an independent geologist, we established our internal “nearology scale” with four clearly defined tiers.

- "Entry level” nearology - only geographically close - almost irrelevant:

If two projects are geographically close but have different geology - it's almost irrelevant.

We are looking at those projects that sit on different types of rock formations with different fault zones.

These almost always are only a play on “we are 40km away from the world’s biggest deposit therefore our grounds should also hold a world-class deposit”.

This rarely works out.

- “Better” nearology - geographically close AND same geological structures:

This is when two projects have the same geology and structures below the ground, but no supporting data - or drilling that has de-risked it to date.

This is a good starting point for an explorer, with the grounds most likely being unexplored. We like to invest in these types of companies because they are genuinely doing frontier exploration.

Getting the fundamentals right and working off what you know (using findings other companies in the same region have made).

There is still a lot of risk with plays like this but the potential upside is high. Generally we manage to pick these types of explorers up at fairly low enterprise values.

- “Even Better” nearology - geographically close AND same geological structures AND supporting exploration work

This is when two projects have the same geology and structures WITH supporting drill-data/geochemistry and/or geophysics.

This is when an explorer has met the requirements of the second tier but has also gone and tested their knowledge and de-risked the assets to an extent.

With these, we like to see either some drill intercepts showing something is where the company thinks it is, rock chips in the area pointing at something, or geophysics showing massive EM targets that need to be drilled.

- “Best” nearology - geographically close AND same geological structures AND supporting exploration work AND confirmation same deposit extends

This is when there is an extension of the same deposit - this is when the asset has been de-risked and is confirmation that the nearology concept has actually paid off and there is in fact worth something of value.

This is fairly straightforward, sometimes deposits extend out from the imaginary lines set by “tenements” and straight into grounds held by other companies.

These situations are fairly easy to spot and are the best type of nearology plays.

So how does FNT rank on our nearology scale?

We rate FNT’s nearlogy to Hastings as a solid 3 out of possible 4, which is very good. FNT has the potential to be a 4 if they can deliver some positive drill results.

Here is how FNT’s neurology to Hastings stacks up against each of our neurology quality rankings 1 to 4:

- "Entry level” nearology ✅ – FNT tenements are right in and amongst it in this part of WA.

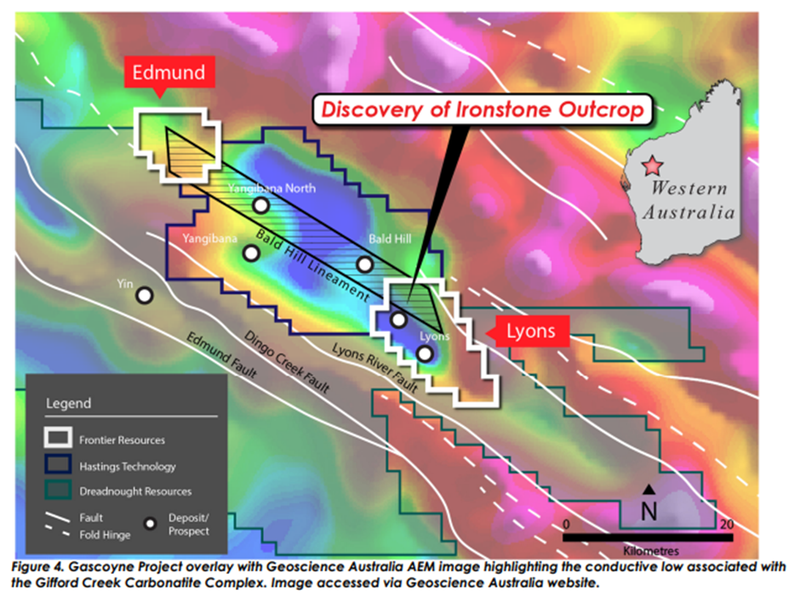

FNT’s projects are wedged on either side of Hastings’ Yangibana project and directly to the north and contiguous with Dreadnaught’s tenements (who recently confirmed high-grade ironstone structures over a ~2.5kms strike zone at its Yin prospect).

As seen in the image below, FNT definitely ticks off the requirements for the first tier.

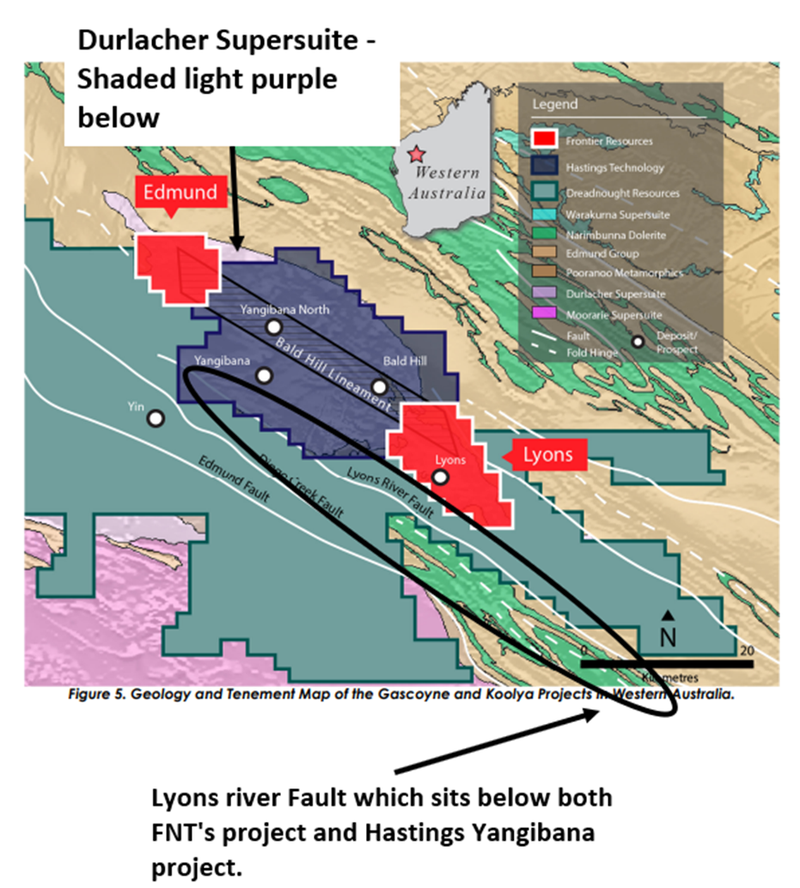

- “Better” nearology ✅ – FNT’s project sits on the same “Durlacher Supersuite” structure and has the same ironstone outcroppings as Hastings Technology’s project.

Hastings Yangibana project was actually discovered based on findings from prospectors who did various rock chip sampling programs in the 1970 and 80s. They targeted the ironstone formations in this part of WA and found some rare earth elements (REE), but until Hastings took control of the project in 2011, the area was largely underexplored for REE.

Hastings then managed to take what began with simple rock chip sampled ironstone outcroppings and turn it into the 27.4mt JORC resource that it has today.

FNT’s Lyons project has similar ironstone outcroppings which sit just above the same “Lyons river fault” that the Yabaninga project sits on top of.

Most importantly though they both sit on top of what's called the “Durlacher Supersuite”. You can just faintly see that it runs into FNT’s Lyons project and almost ends right on the border of the project's southeast section.

FNT also holds the Edmund project which is on the northeast section of this structure. Again almost exactly where the structure ends.

In summary, FNT sits on similar geological structures to Hastings deposit - which is a good thing.

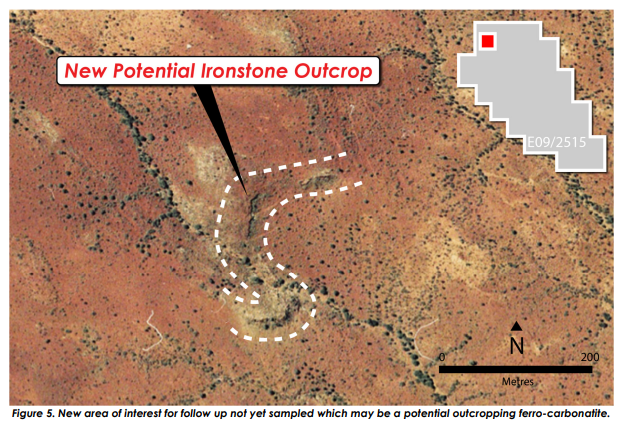

- “Even Better” nearology ✅ – FNT has rock-chip sampled some of the ironstone outcroppings and has conducted EM surveys - with results due soon.

Having met the criteria for tiers 1 and 2 on our nearology scale, FNT just managed to push itself into the third tier.

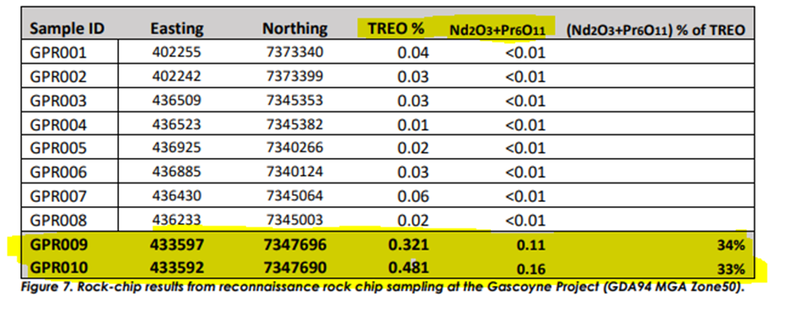

With a recent rock-chip sampling program over the outcropping ironstone formations (identical to Hastings next door) which confirmed REE-bearing ironstones with maximum assays of 0.48% total rare earth oxides (TREO) with a combined 0.16% Neodymium and Praseodymium.

Although these grades are nothing to write home about, FNT’s aim with the rock-chip sampling program was to show the presence of something of interest to conduct further exploration.

This compares to Dreadnought’s recent sampling program which produced very high grade rock-chip samples upto ~11.2% TREO, including 3.6% Neodymium + Praseodymium. This sent the share price of Dreadnought from 2.3c to 2.8c in one trading day adding ~$12M in market cap to the stock.

In addition to this, FNT in late 2021 completed an airborne magnetic-radiometric survey covering ~230km of its grounds from which the results should be due very soon.

This will be the final bit of work done before some high-priority drill targets are set and can be readied for drilling.

In the meantime, working with images put together by Geoscience Australia, we can see the conductive lows that FNT’s Lyons project sits on top of (blue colours).

Again, we are not geologists and this is our interpretation of complex geological analysis but to us, it looks like the Yangibana deposit seems to be sitting on really similar coloured blobs to Hastings.

Ultimately we want to see the outcome from the airborne EM surveys FNT did so that we can have a higher level of assurance there are drill-worthy targets on FNT’s grounds.

So in summary, at this point in time, FNT’s rare earths projects have hit our nearology requirements across the first three tiers:

- “Entry level” nearology - Sitting in the same region, ✅

- “Better” nearology - Sitting on top of similar rock structures ✅

- “Even Better” nearology - Rock-chip samples/Aeromagnetic surveys pointing at certain target areas of interest (ironstone outcroppings). ✅

Bringing this all together, FNT ranks in the third tier (“Even better”) of our nearology scale.

The next step is to demonstrate via drilling that the mineralised system that Hastings found does in fact extend or is present in FNT’s ground.

We think this would lead to a significant re-rate in the FNT share price.

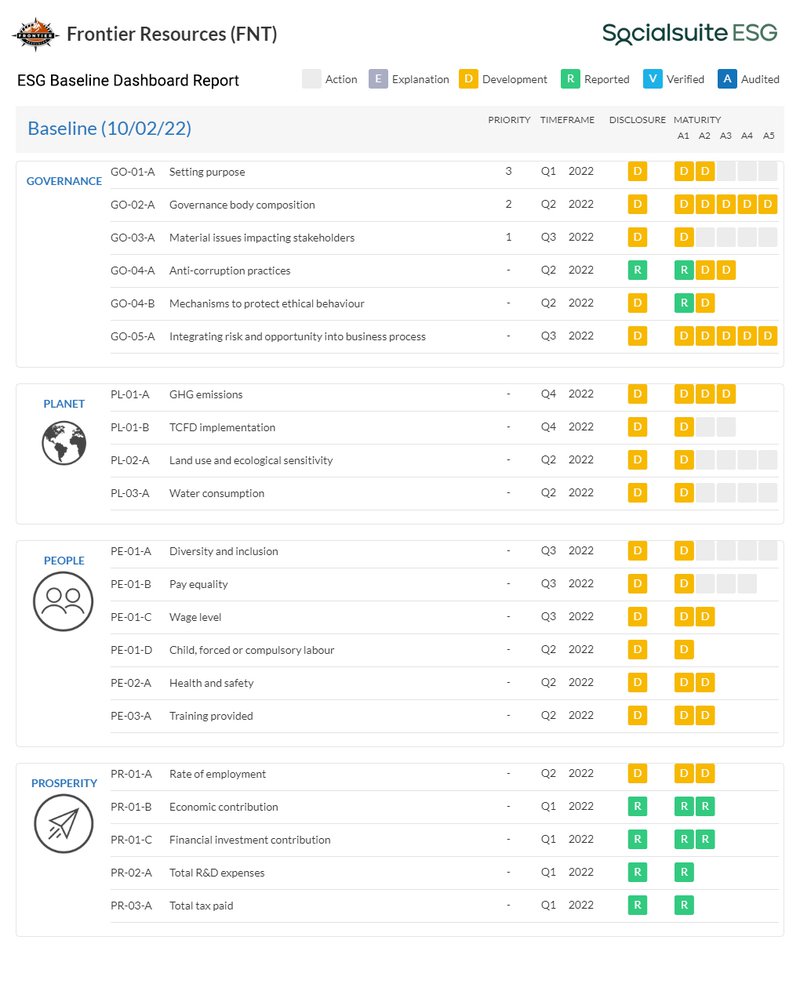

FNT is taking Environmental, Social and Governance disclosures seriously

You’ve probably heard of environmental, social and governance (ESG) by now.

The world has collectively decided it wants to “go green” and also usher in a new version of capitalism that takes into account not only shareholder profit, but environmental, social and governance (ESG) considerations too.

Global funds through to the “mom and dad” retail crowd are increasingly seeking investments that help make the world a better place, and as a by-product, helps us feel better about those investments.

The belief is that companies with strong ESG credentials are less risky or prone to questionable practises, more transparent, and better positioned for the long term.

We like investing in companies that regularly disclose and improve ESG because they are better able to:

- Access ESG funds – There is currently more ESG money than there are ESG investment ready opportunities.

- Secure top tier customers – Top companies are conscious of ESG in their supply chain – think Tesla, Apple, Governments etc.

- Attract the most talented teams – Smart people do not want to work for non-ESG companies.

- Positive community perception – Doing business at all levels is just easier when the community wants you to exist.

- Shareholder returns with positive impact – Be proud they are creating a positive change in the world while providing outsized returns to shareholders.

FNT has committed to ongoing ESG reporting and disclosures, which can be tracked in their quarterly ESG report here:

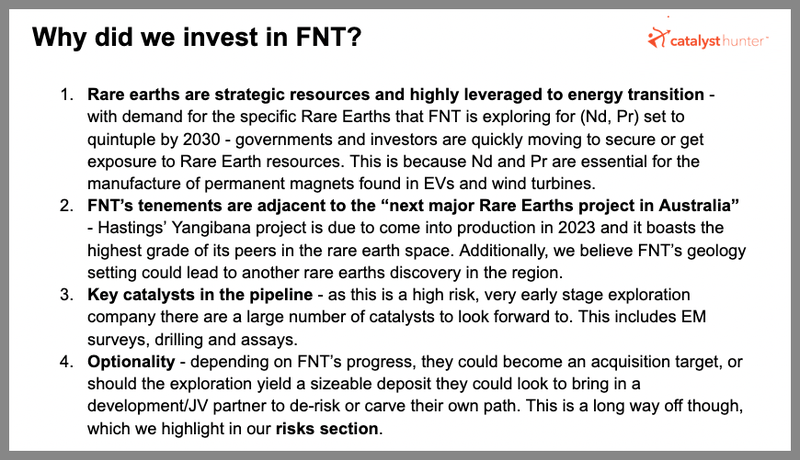

Why we invested in FNT

On top of the macro theme driving rare earths investment, the proximity of FNT’s tenements to a world-class rare earths project and the favourable geology in the region, there are the two other reasons why we invested in FNT as per our FNT Investment Memo.

Reasons #3 and #4 are closely tied to FNT’s status as a very early stage explorer.

For us, FNT’s appeal lies in the fact that it could be anything in the future.

With that in mind, we’ve laid out the three things we want to see from FNT in 2022.

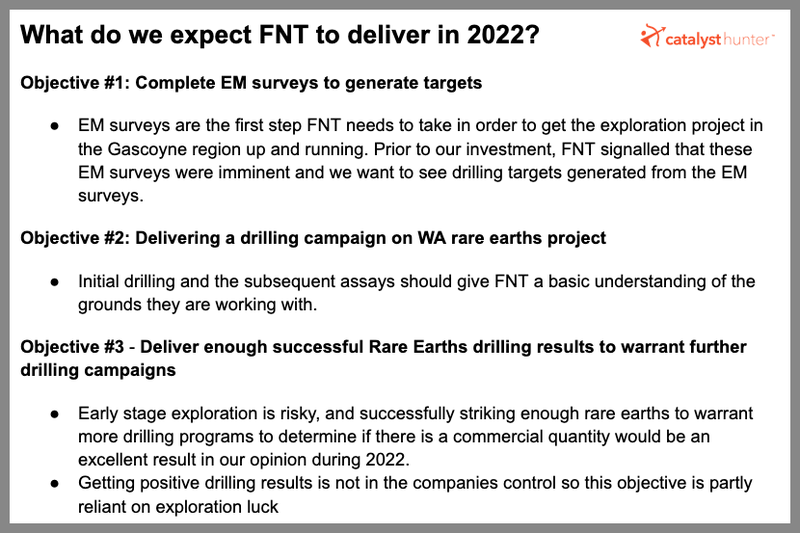

Key objectives for FNT

Like most early stage exploration companies - FNT’s activities in 2022 should follow a familiar path.

Namely, FNT needs to complete its EM surveys to generate drill targets, drill those targets and get assays from that drilling back.

This process repeats as FNT refines its understanding of the project - with the ultimate aim of discovering an economic resource with various opportunities for a market re-rate along the way pending success.

These are the three key objectives that we’ve highlighted in our FNT Investment Memo:

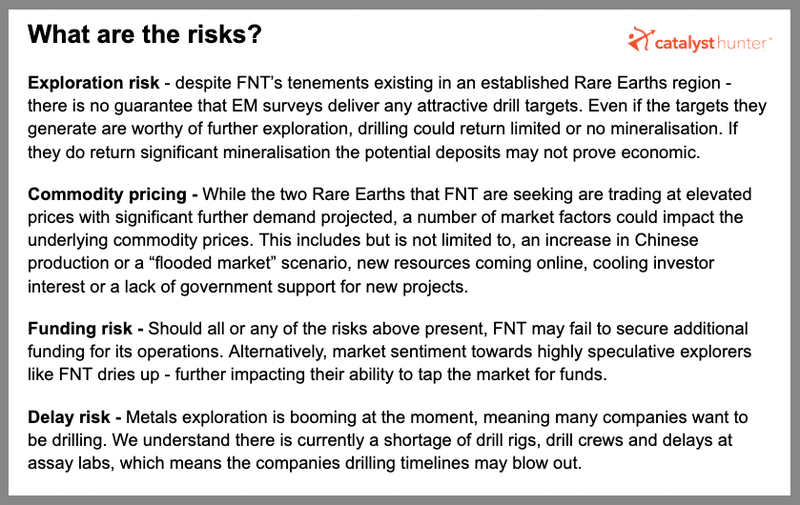

Key risks

We note four key risks with our FNT investment in our FNT Investment Memo:

These types of risks are relevant for any highly speculative explorer - and given its very early stage status, these risks are heightened.

With FNT, we’re keenly aware that this is a high risk investment - indeed, it falls firmly on the outer band of our risk appetite spectrum.

At the same time, for the reasons we’ve outlined above, we also feel that the rewards for FNT’s success could be substantial.

In short, we believe FNT is a good fit for our Catalyst Hunter portfolio.

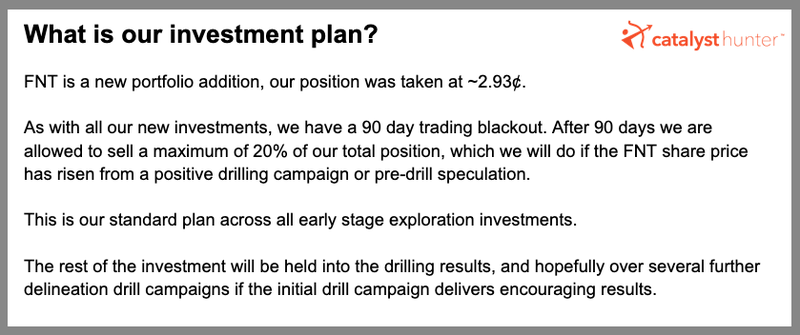

As with all our investments, we have a specific strategy for our position in FNT which consists of an investment plan.

Our FNT investment plan

Disclosure: The authors of this article and owners of Catalyst Hunter, S3 Consortium Pty Ltd, and associated entities, own 12,823,582 FNT shares at the time of writing. S3 Consortium Pty Ltd has been engaged by FNT to share our commentary on the progress of our investment in FNT over time.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.