Nickel Mines negotiates superior funding package

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

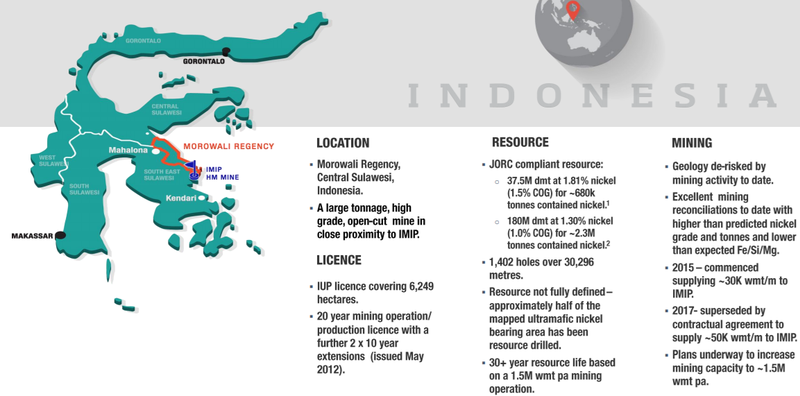

Pursuant to Nickel Mines Ltd’s (ASX:NIC) intention to increase its interest in the Ranger Nickel Project in Indonesia from 17% to 60%, the company has negotiated a funding package comprising a mix of debt and equity with Decent Investment International, an associate of the group’s operating partner Shanghai Decent Investment (SDI).

The proposed funding package totals US$150 million and comprises a debt facility with Decent of US$80 million and planned equity of US$70 million.

The equity component includes US$40 million of Nickel Mines shares to be issued as partial consideration for the 43% interest in the Ranger Nickel Project, which will lift NIC’s interest from 17% to 60%.

The remaining US$30 million is planned to be raised as fresh equity from current and/or new professional investors.

Nickel Mines has previously stated it is targeting the completion of the acquisition by June 2019.

Mates rates says Bell Potter

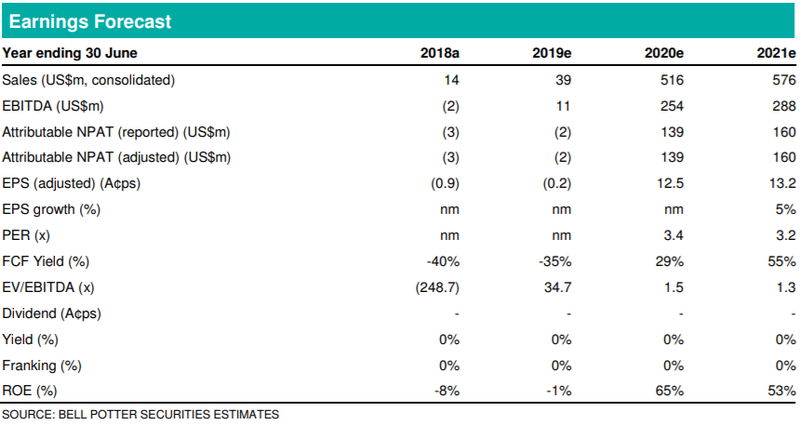

Bell Potter analyst, David Coates viewed the transaction positively, among other things noting that the total size of the package had been reduced from US$160 million to US$150 million, including reduction of the debt component from US$100 million to US$80 million.

Furthermore, the funding is now being provided by Decent, as opposed to Sprott Private Resource Lending.

On this note, Coates said, “Decent has offered a lower interest rate (LIBOR + 6%) vs Sprott (LIBOR + 7% + 2% fee + 45 million warrants), which, in our view, justifies the change.

“The trade-off has been a higher equity component, now US$70 million (vs US$60 million) and incrementally more dilution.

“On our assumptions, SDI’s shareholding in NIC would increase to circa 18% following the raise.”

(LIBOR stands for London Interbank Offered Rate, and it is a benchmark interest rate at which major global institutions lend to one another in the international interbank market for short-term loans.)

Share price upside of 115%

With Nickel Mines now having fewer stakeholders to satisfy, this represents not only a cheaper package, but an arrangement that is easier to manage.

The dilution to value through the issue of more shares has only had a nominal impact on the company’s metrics as indicated by Bell Potter’s projections.

Coates has maintained his buy recommendation, while marginally lowering his valuation from 95 cents to 93 cents per share.

The company is Bell Potter’s top pick in the sector, and Coates’ valuation implies share price upside of nearly 120%.

With robust returns on equity and the current share price implying a fiscal 2020 PE multiple of less than four, there only appears to be one direction for the company’s share price to head.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.