Nickel Mines forecast to deliver US$136 million net profit

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Not surprisingly, when Nickel Mines Ltd (ASX:NIC) informed the market of its decision to increase the company’s 17% ownership in the highly successful Ranger Nickel Project to 60% the company’s share price increased sharply.

The uptick from 41.5 cents to a high of 46.5 cents in the week following the announcement represented an increase of approximately 12%.

However, there has been recent weakness in the nickel price, and perhaps that accounts for a retracement towards the end of April.

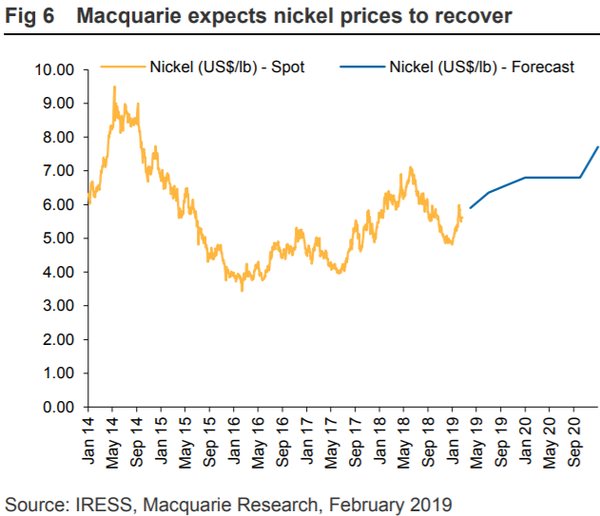

This could represent a buying opportunity, particularly if analysts at Macquarie are on the mark in projecting sustained upward momentum in the nickel price in coming years.

The broker’s forward estimates are highlighted below, and they are generally in accord with Bell Potter’s forecasts, one of the brokers that covers NIC.

Bell Potter is expecting the nickel price to increase from US$5.83 per pound in fiscal 2019 to US$7.15 per pound in 2020, rising again to US$7.45 per pound in 2021.

The broker is bullish on NIC, taking a particularly positive stance since the group announced that it would be increasing its stake in the project to 60%.

How does this snapshot of NIC’s financials look?

Bell Potter upgrades share price target to 95 cents

In response to increasing its holding to 60%, Bell Potter substantially increased its profit forecasts for fiscal years 2020 and 2021, reflecting the significantly higher proportion of revenues attributable to NIC as a result of increasing its stake in the project.

The broker’s net profit estimates for fiscal years 2020 and 2021 were increased from US$95 million to US$136 million and US$110 million to US$157 million respectively.

This implies earnings per share of 12 cents in fiscal 2020, indicating that the company is currently trading on a forward PE multiple of less than four.

This represents a significant discount for a company that has material earnings visibility, strong financial partners and an operation (60% owned Hengjaya Nickel Project) that is running at nameplate capacity, no small feat in itself given that it was only commissioned three months ago.

In tandem with upgrading its earnings estimates, Bell Potter also upgraded NIC’s net present value share price target from 72 cents per share to 95 cents per share, implying upside of 120% to the company’s current trading range.

Highly leveraged to recovering nickel price

In commenting on the game changing medium to long-term significance of the group’s move to 60% ownership, as well as the negotiation of an agreement regarding an acquisition financing package, managing director, Justin Werner said, “We are extremely pleased to be in a position to fast-track our increased interest in the Ranger Nickel Project with Ranger now set to commence commissioning well ahead of schedule.

“This decision will see our attributable nickel production across both Hengjaya and Ranger nearing 20,000 tonnes per annum and see us well on our way to fulfilling our ambition of being a globally significant nickel producer and a tier-1 nickel investment exposure among our global peer group.”

This is definitely the case as NIC is a much safer way to gain leverage to the nickel price than targeting speculative miners.

While a PE-based positive rerating should occur sooner rather than later, also keep an eye on the nickel price because even a 5% increase will have an exponential impact on NIC’s bottom line.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.