Nick Scali, you’ve done it again

Published 15-AUG-2016 14:33 P.M.

|

3 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

While investors tend to get excited about high profile retailer, JB Hi-Fi (JBH), it is unlikely that the group will match the much smaller Nick Scali (NCK) at an earnings growth level after NCK delivered a quality result last week which featured earnings per share growth of 32%.

To provide some context, JB Hi-Fi is trading on a fiscal 2016 PE multiple of 19 relative to consensus forecasts which point to earnings per share growth of 5.1%.

NCK is trading on a far more conservative multiple with double-digit earnings per share growth forecast in fiscal 2017 compared with consensus estimates of 6.2% for JB Hi-Fi.

Consensus forecasts are subject to fluctuation and investors should note that earnings estimates and price targets may not necessarily be realised and as such should not provide the basis for any investment decision.

However, while the relative performances of JBH and NCK perhaps poses the question as to whether it is time to look for an emerging smaller player in the consumer discretionary space, it is worth looking at Nick Scali’s performance to get a feel for the business and its scope for future growth.

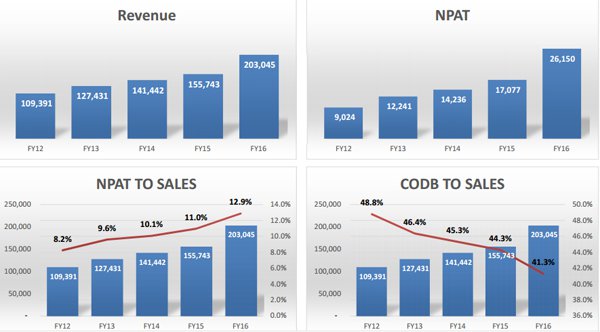

Shares in furniture and bedding retailer Nick Scali (NCK) spiked last week after the company delivered a record net profit of $26.2 million, ahead of management’s guidance ($24 million-$26 million) and Macquarie Wealth Management’s estimate of $25.2 million.

The company’s share price increased from $4.80 on the day prior to the announcement of the result to an all-time high of $5.69 before closing at $5.67 on Friday. This represents an increase of 18%.

It should be noted that share prices are subject to fluctuation and investors should take a cautious approach to any investment in NCK and not base that decision solely on historical price movements.

The group’s operational statistics were extremely impressive with sales up 30% and same-store sales growth of 11.1%. The latter is important in the context of Nick Scali being a store rollout story.

As the business matures and there is less scope for store expansion there will be an increasing reliance on management’s ability to deliver organic growth.

That said, the company has consistently delivered on this front since listing on the ASX in 2006 with management traditionally under promising and outperforming. As can be seen in the following table, Nick Scali’s outperformance hasn’t just been a function of top line growth, the company has demonstrated over the years that it can drive down costs while still growing the business.

Management’s astute performance over the last five years combined with the expectation that Nick Scali’s can sustain robust double-digit growth in coming years underpinned significant increases in earnings per share forecasts off a relatively high level by Macquarie Wealth Management.

The broker increased fiscal 2017 and 2018 earnings per share forecasts by 3.4% and 8.6% respectively while increasing the 12 month price target by 9.7% to $6.09, implying a premium of circa 10% to Friday’s closing price.

In providing guidance, management warned investors not to expect the outstanding profit growth of more than 50% in fiscal 2017 given that this was assisted by an accelerated store rollout strategy.

However, the company will continue to open stores in Australia in fiscal 2017 while targeting the opening of 3 to 4 stores in New Zealand in fiscal 2018.

Management has maintained its long-term network target at 75 stores in Australia and New Zealand. Currently the group has 47 stores, indicating there is still significant scope to grow the business.

Macquarie Wealth Management has an outperform recommendation on Nick Scali, and its fiscal 2017 forecasts imply a PE multiple of 16 relative to Friday’s closing price.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.