Mustang Resources fully funded through to October ruby sales

Published 20-JUL-2017 13:43 P.M.

|

5 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Finfeed presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

Mustang Resources (ASX: MUS) has secured an A$8.5 million funding facility under an 18-month term convertible note facility (Convertible Note Deed) with a leading US institutional investor, ensuring that it is fully funded through to its upcoming maiden rough ruby tender in October 2017.

The Convertible Note Deed, with convertible notes having a face value of $10 million, has been signed with Arena Investors LP (Arena), a US based institutional investor with more than $600 million in assets under management.

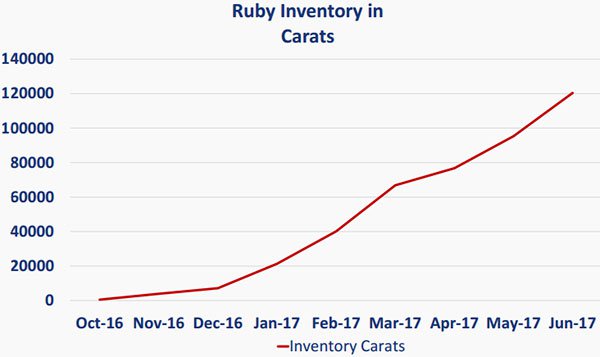

In commenting on this development, Mustang’s Managing Director Christiaan Jordaan said, “The funding arrangement marks another key step in the company’s growth as it continues to recover high quality rubies from its recently upgraded processing plant and ongoing artisanal development program at Montepuez, where its total ruby inventory now stands at ~132,000 carats”.

Commodity prices do fluctuate and caution should be applied to any investment decision here and not be based on spot prices alone. Seek professional financial advice before choosing to invest.

Jordaan highlighted that this facility ensures MUS is fully funded until the first closed-bid tender of the group’s rubies in October this year, providing the company with the ability to maximise the number of rubies tendered for sale in October.

Jordaan views the funding from an institution of Arena’s size and standing as a significant vote of confidence in Mustang and the Montepuez ruby project. Importantly, achieving this funding agreement minimises dilution for existing shareholders.

Demonstrated success from a high quality ruby rich region

As a backdrop, MUS is focused on the near-term development of the highly prospective Montepuez Ruby Project in northern Mozambique. The Montepuez Ruby Project consists of four licences covering 19,300 hectares directly adjacent to the world’s largest ruby deposit discovered by Gemfields PLC (AIM:GEM) in 2012.

Since supply of rubies from sources outside Mozambique has become fractured and unreliable, MUS stands to capitalise on the current demand around the world for ethically produced rubies by becoming a reliable, consistent supplier of high-quality rubies.

Management is currently fast-tracking its work program on the Montepuez Ruby Project with high priority targets being identified and low-cost bulk sampling well underway. First rough ruby sales are scheduled for October 2017 under a closed bid tender of an estimated 200,000 carats gem quality rubies.

Hartleys sees 50% share price upside potential

Hartleys resource analyst, John Macdonald made the following comments this week regarding the quality of rubies typically recovered from the region being mined by Mustang Resources.

“The best Montepuez rubies are often compared to the highest value Mogok stones from Myanmar that have long been in scarce supply in the rough. Gemfields Plc produced and sold rough Montepuez rubies for US$280M revenue from 2014 to 2017. At least an equivalent amount of informal production may also have come out of Montepuez in the same period”.

Macdonald noted that MUS is the only pure listed exposure to the Montepuez gem field, and the upcoming bulk sampling program could convert seamlessly to commercial operation if successful.

Given this scenario, he has placed a speculative buy on the stock in the expectation that the company will build up a production and sales record in 2017 and 2018.

On this basis, Macdonald has set a 12 month price target of 8.5 cents representing a premium of circa 45% to Thursday morning’s opening price of 5.9 cents.

Hartleys weighs up Mustang’s operational performance to date

Hartleys provided a thorough rundown of MUS’s achievements to date, as well as highlighting the operational aspects of the Montepuez project. The broker noted that the group had developed a 380,000 tonnes per annum processing capacity at Montepuez at a nominal cost of less than $10 million.

Hartleys highlighted the fact that commercial gem operations depend both on ore grades in carats per tonne and average value per carat. The product of the two statistics provides a $/tonne figure which is a more useful number.

The broker postulated that all-up costs in Montepuez might average US$15-40/tonne, depending on a number of factors. At 50 carat/100 tonne (recovered) and US$300/carat (rough), revenue would be US$150/tonne.

Reflecting on MUS’s progress to date, early indications of 50 carat/100 tonne from the June bulk sampling results at 8245L is encouraging in this context, although the tonnage tested is still limited at this stage.

Hartleys also noted that average carat value remained unconstrained, probably in the US$50-700/carat range.

It should be noted that broker projections and price targets are only estimates and may not be met. Also, historical data in terms of earnings performance and/or share trading patterns should not be used as the basis for an investment as they may or may not be replicated. Those considering this stock should seek independent financial advice.

Where to from here

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.