Mozambi Extends Graphite Portfolio in Tanzania

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Graphite hunter Mozambi Resources (ASX:MOZ) has just picked up four more licenses in Tanzania in a deal worth an initial amount thought to be in the order of $539,000, but only $104,000 in cash.

Two of the four licence areas, which are interwoven with MOZ’s current tenements, currently host prospects while the other two have had little to no exploration well done on them.

It will bring MOXZ up to 11 tenements overall, and the new areas will be included in a 777 line kilometres VTEM survey.

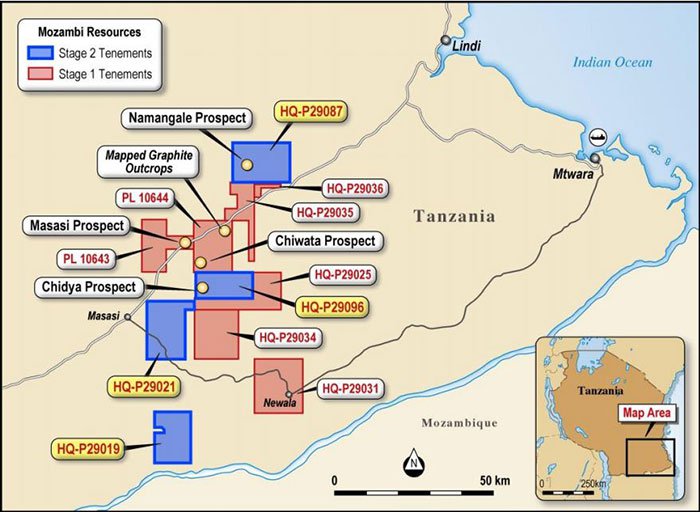

Map showing MOZ’s new tenements

HQ-P29096 hosts the Chiyada prospect, and is less than 10km south of MOZ’s existing Chiwata prospect.

As reported yesterday by Finfeed, MOZ effectively quadrupled the strike length at Chiwata As the result of rock chip samples collected from trenches at the project.

It told the market today that “further delineation of this deposit [Chiyada] could add significant synergies for the company going forward” – hinting that the two deposits could be linked in some way.

Meanwhile HQ-P29087 hosts the Namangale Prospect, north of existing MOZ licenses.

As part of the deal, MOZ has committed to spending a minimum of $500,000 on exploration in the new license areas in the first two years.

The deal in detail

MOZ has managed to swing the deal by getting in touch with the company with those mining tenements under application.

Under the terms of the deal, the company will withdraw its application and MOZ will tender on in their stead.

MOZ will pay for the cost of the applications, capped at $US4000 ($A5673).

Once the licenses are issued, MOZ will pay an initial $100,000.

It will also issue 15 million fully paid ordinary shares of the company, with its price currently 2.9c. It will also issue 7.5 million listing options, currently at 1.5c.

This means the deal could have an initial outlay worth $539,000 (not including the options), with $104,000 of this in cash.

There are also milestones surrounding the deal, with the issue of up to 60 million shares contingent of proving a resource of up to a 20 million tonne JORC compliant resource at more than 5% total graphitic carbon.

There are also ongoing 3% smelter royalty attached to the deal, but MOZ can halve this by paying $2 million.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.