Microcap Cannabis Stock BOD has two major near term catalysts…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,535,112 BOD shares at the time of publishing this article. The Company has been engaged by BOD to share our commentary on the progress of our Investment in BOD over time.

What makes a medicinal cannabis stock go up more than 270% in a day?

Three weeks ago a long forgotten stock went vertical when its cannabis derived medicine outperformed a pharmaceutical giant’s pain drug.

A drug which has previously generated upwards of US$5BN in annual sales.

It’s the kind of early stage breakthrough that gets the market’s attention.

It’s also a sign that when the market’s eyes do snap into focus - things happen very quickly.

So there’s a blueprint out there for cannabis stock re-rates - we just need the right catalyst to come in.

Recently, our cannabis microcap Investment BOD Science (ASX:BOD) has shifted gears from slowly growing revenue, in favour of going for a big blue sky approach to delivering shareholder outcomes.

BOD is currently expecting two near term catalysts:

- Clinical trial results on its cannabis based insomnia treatment (any day now), which can be sold over the counter if successful

- Initial Pharmacokinetic (PK) study results which will show if its “bioavailability” product can make medicine delivery more potent and water soluble i.e the medicine can be delivered via a "drink" (think gatorade but with medicine in it) - this would make BODs product sellable in a “drink” format

(1) is due this week and (2) is expected in a couple of months

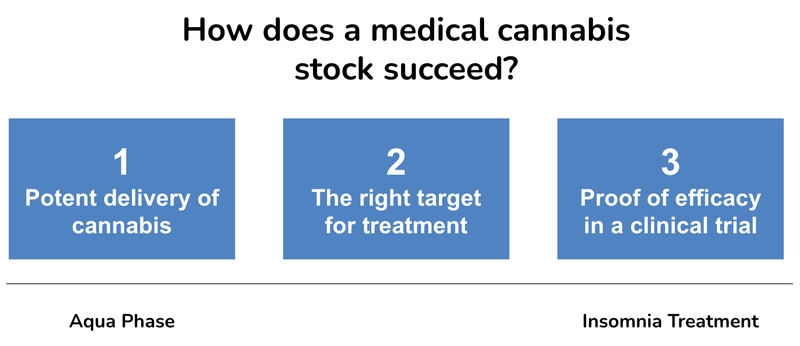

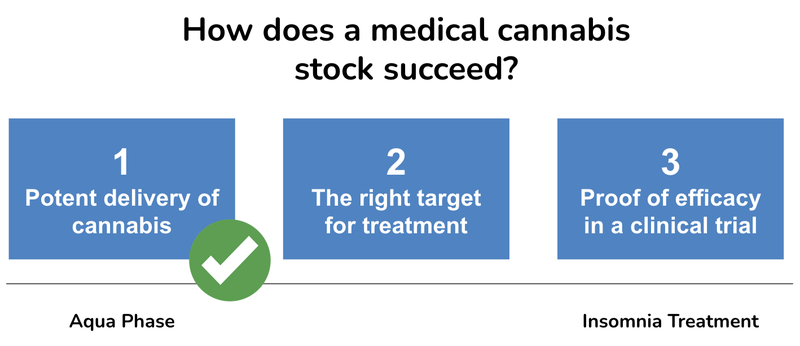

We think in the current soft market there are three keys to share price success with any medicinal cannabis product:

- Potent delivery of cannabis

- The right target for treatment

- Proof of efficacy in a clinical trial

This was the strategy adopted by Zelira Therapeutics, which saw its share price rise 270% in one day off the back of strong results from a top-line-study for its cannabis-based pain medication.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This is an example of what we hope might happen, but remember that just because Zelira’s share price reacted this way on successful trials, doesn't necessarily mean BOD will do something similar if their trials succeed.

Also, BOD is chasing a different condition in a clinical trial - insomnia.

The prize for a successful cannabis based insomnia treatment appears to be big enough that a few companies are trying to find one (and two so far have failed in their trials):

With two other companies failing in their clinical trial, the expectations for BOD are low, which is reflected in the market cap.

Share price movements on the results of binary outcomes, like a clinical trial, are all about expectations and results exceeding or meeting expectations.

We think that BOD is starting from a low base of expectations, given the past failures of other companies, which means that the potential for a material re-rate on positive results is higher.

We cover this phenomenon in depth here: Share price moves on expected vs unexpected announcements.

Remember, BOD has two main products here at the moment as a cannabis medicine and tech company, CBD clinical trials for insomnia, and a “bioavailability” product that could make cannabis delivery more potent, and sold in a “drink” format.

Whereas THC focussed cannabis companies (the thing that gets people “stoned”) need scale - CBD companies like BOD need clinical evidence and intellectual property.

BOD is pursuing just this - with two major catalysts to come in the next two months.

These are the two catalysts we’re closely watching:

Catalyst #1: Insomnia Treatment Results

Description: Results from the Phase IIb clinical trial using BOD’s CBD (Cannabidiol) product on insomnia

When: Due this week

Our Take: If the clinical trial is successful it will form the basis of an application to Australia’s Therapeutic Goods Administration (TGA) and unlock the opportunity for significant sales for the first “over-the-counter” cannabis products in Australia. We think media attention would likely follow.

Catalyst #2: Aqua Phase test results

Description: Two efficacy results on BOD’s new Aqua Phase tech

When: End of June + End of July

Our Take: The results from these two Pharmacokinetic (PK) Studies evaluate how well BOD’s tech can improve absorption of CBD (also known as bioavailability). A material improvement in bioavailability would have major implications for BOD. It opens up the potential to licence/or form partnerships across the whole global CBD market, a US$6BN industry that would be eager to get access to this tech.

Here is how each catalyst fits in our keys for a successful cannabis company:

We are that betting BOD can deliver a widely available CBD medication that is clinically proven to treat insomnia in pharmacies all across Australia.

Following that, a tech breakthrough for the global CBD market.

CBD Gatorade? It’s not too outlandish. We’ve previously flagged how BOD’s Aqua Phase could be the gateway to a lucrative cannabis drinks market.

Together, we think these two catalysts could play a big role in changing BOD’s fortunes.

And today we want to do a deep dive on both.

We see Catalyst #1 as a springboard for BOD, and Catalyst #2 as the beginning of BOD’s emergence as a leading cannabis-tech/cannabis-science company.

This forms the basis of our Big Bet:

“BOD will deliver a minimum 10x return on successfully commercialising at least one application of its new technology that optimises the human body's absorption of cannabinoids.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our BOD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

The blueprint: BOD’s strategy

BOD’s CEO and founder Jo Patterson has made a strategic decision to home in on clinical evidence and intellectual property.

That strategy has two main prongs at the moment - which are the two catalysts that are due soon.

If BOD can prove its CBD works for insomnia and/or its Aqua Phase tech works this could underpin a valuation uplift.

Intellectual property and clinical evidence (even early signs of improved efficacy and safety profile) worked for a company called Zelira Therapuetics.

Zelira saw its share price rise by more than ~270% in a single day (late May) when it released topline results from a head-to-head study.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This is an example of what we hope might happen, but remember though that just because Zelira’s share price reacted this way on successful trials, doesn't necessarily mean BOD will do something similar if their trials succeed.

Like BOD, Zelira is a cannabis focussed biotech/science company - Zelira is advancing non-traditional treatments for big market diseases, in this case, diabetic nerve pain.

We think that if BOD can deliver on either one or both catalysts we previously outlined (CBD insomnia/ water soluble “bioavailability” product), BOD could experience a similar re-rate that Zelira has shown is still possible in the cannabis industry.

Zelira’s overall strategy has some differences to BOD’s strategy - but we think its move shows that in the right circumstances cannabis companies can still re-rate significantly.

More on BOD’s insomnia trial

BOD’s Phase IIb clinical trial on insomnia is expected to be complete by this week, with results soon to follow.

Led by a prominent sleep research organisation, the Phase IIb results will identify whether BOD’s unique CBD formulation will help people with insomnia.

If the results show strong levels of efficacy, BOD hopes to have sufficient data to register its treatment as an “over-the-counter” solution with the TGA - the first cannabis product of its kind in Australia.

A little bit of background on over-the-counter cannabis products in Australia.

In 2020 the Therapeutic Goods Administration of Australia (TGA), who is the Australian equivalent of the FDA, announced new rules that would allow companies to sell registered medical cannabis products without a doctor’s prescription in sub-150 mg doses.

In order for a company to be eligible for the Special Access Scheme, it would need to prove that its product works through a clinical trial.

Although the scheme has been around since 2020, there are still no over-the-counter cannabis products sold in Australia.

This is because there are a few narrow targets for conditions that are mild enough not to need medical supervision, but not so mild that it doesn’t need treatment.

That's where insomnia comes in.

Insomnia is the perfect condition for emerging medical cannabis products to target, to become the first over-the-counter cannabis product in Australia.

Although the market size for insomnia in Australia is relatively modest, with $97M spent on pharmacy sleep aids in 2021 - the prize is bigger than that.

If BOD could prove that its product is efficacious in a clinical setting, it opens up a range of new markets and opportunities for treatment.

Remember, the third piece of the puzzle for a successful cannabis companies “proof in a clinical setting” - and this is what BOD is trying to achieve here.

There were four companies in the race to be the first product to market, with two companies failing the clinical trial.

So far, the first two companies have failed the clinical trial - Cann Group and Ecofibre.

In each case, the company could not prove that their medicinal cannabis product was statistically superior to a placebo at improving sleep in people with insomnia.

This may have something to do with the clinical trial design, and how patients were screened OR it could be with the potency of the product.

This article does a great job of breaking down each of the four clinical trial designs:

Ultimately, clinical trials have a binary outcome and have a low chance of success - particularly with cannabis based products that are yet to be proven to improve sleep.

There is no guarantee of success here.

However, IF BOD is able to succeed however it will be the first over-the-counter cannabis product in Australia and have 100% of the market share - in a field that is hard to prove works.

Success for BOD at this clinical stage also sets the stage for other over-the-counter uses of its product and builds upon a body of evidence for BOD’s product at a clinical level.

“Proof of efficacy in a clinical trial” is one of our key markers for a successful cannabis product - and we are hoping that BOD can be the first to prove that its cannabis tablet is effective at treating insomnia.

More on BOD’s Aqua Phase acquisition

In September last year BOD announced the acquisition of a cannabis product and process technology that allows more rapid onset, better efficacy and lower dosage rates of cannabidiol (CBD) products.

Basically a product that makes cannabis more potent.

The mechanism behind the technology is that lets the human body absorb CBD more effectively, leading to less product being needed to achieve the desired effect.

The current problem with many CBD formulations is that the body struggles to absorb the CBD because it doesn’t get broken down properly in the stomach.

CBD users and patients need to take large amounts to get the desired therapeutic impact - and even then, results can be dubious depending on the quality of the product.

There is also a regulatory benefit in greater potency of cannabis.

The threshold for approval for over-the-counter use in Australia is 150mg of cannabis. But treatment for anxiety disorders (a common use for cannabis products) is more in the 300-450 mg range.

If BOD’s products can produce the same amount of potency in a smaller active ingredient, then it opens up a bunch of new conditions to target with over-the-counter treatments.

This new product, called Aqua Phase, promises to dramatically increase the bioavailability of CBD in the human body - so it's more potent, and more effective.

Bioavailability is the ability of the stomach to absorb a particular substance, and with BOD’s new product there are a range of opportunities that it could pursue.

The acquisition of the product is subject to two Pharmacokinetic (PK) Studies, which are basically tests to see how well BOD’s tech can improve absorption of CBD.

If the tests indicate 30% or greater bioavailability, then BOD will have to pay £1M (~AUD$2M) to complete the acquisition.

However, if the tests don’t meet the threshold, we think BOD may be able to still acquire the product, potentially at a cheaper value, if it still has some meaningful impact on bioavailability.

Here is where we see the material opportunities for BOD with this acquisition:

- Improve BOD’s current product suite

- Unlock Epidiolex ‘like’ moonshot for epilepsy

- New products, new markets

- Other opportunities

Improve BOD’s current product suite

BOD can gain a competitive advantage by applying its new tech to make existing products deliver the same or better therapeutic impact with less raw material.

With BOD’s clinical trial for insomnia underway, it could vastly improve its suite of clinical based products.

Unlock Epidiolex ‘like’ moonshot for epilepsy

BOD’s new tech presents an opportunity for fast-tracked FDA approval to sell its CBD under a new drug application.

If BOD does go down this route it will be a long clinical trial process, but the prize at the end of the tunnel is big.

The only FDA approved cannabis product is Epidiolex which is a CBD oil used for treating child epilepsy.

This product recorded US$500M in sales in 2020, with US$1.4BN in sales forecast in 2025.

With this new technology BOD could follow the Epidiolex route and launch a similar or better product to tap into the market.

New products, new markets

One clear target market to consider will be the beverages market where several countries, including Canada, are open to cannabis-infused beverages businesses.

One estimate of the US cannabis drinks market places it at ~US$1BN and growing at a staggering 54% year on year through to 2028.

Imagine a cannabis/CBD drink formulated on BOD’s Aqua Phase products...

This is a big blue sky opportunity for BOD that could be unlocked with the Aqua Phase acquisition.

Other Opportunities

With a more potent product there are a myriad of different directions that BOD could go.

We won't speculate too much but BOD could licence its technology, develop new drug applications and more.

If the Aqua Phase acquisition goes ahead, we want to see BOD form a clear plan to capitalise on the investment.

That said, this acquisition does tick off one of the key aspects that we see as to delivering success in a medical cannabis stock.

If BOD can prove that its product is potent and can deliver more therapeutic value in smaller doses, its next step is to find the right target for treatment and prove that its product works in a clinical setting.

This is the pathway followed by GW Pharmaceutics, which was acquired by Jazz Pharmaceuticals for US$7BN along with its cannabis based Epidiolex product treating children with epilepsy.

With the results due soon, a positive result will open many doors for BOD to deliver value to shareholders.

New markets opening up for BOD

Last week, BOD announced an important step towards entering a new market in South East Asia.

As many cannabis market watchers would know, Thailand has recently legalised the sale of cannabis products, resulting in a boom market in the country.

Neighbouring Malaysia, is considering altering its cannabis laws, potentially starting with a medicalisation initiative.

BOD is well suited to these types of initiatives - given that its sole focus is on cannabidiol (CBD) - a non-hallucinogenic component of cannabis.

This is the short version of BOD’s Letter of Intent announcement:

- BOD will work with Antah Group (large investment holding company in Malaysia, which has a healthcare arm)

- BOD to supply products to Antah with “investigational medical products”, likely BOD’s CBD range

- Together, the two companies will explore potential clinical trials in the country

- Antah will have exclusive right to market BOD’s products in Malaysia

The idea here is that BOD will be at the forefront of any Malaysian medical cannabis push.

Although this is just a signal of BOD’s intent to enter the market, and it sits outside the scope of the objectives we set out in our current BOD Investment Memo, we will be watching this space closely to see if BOD can gain traction in the region.

What’s coming up next for BOD?

🔄 Results for the Phase IIb clinical trial on insomnia

We’re expecting BOD to announce the completion of the clinical trial by the end of this week with the results to follow shortly after.

These results will form the basis of an application to Australia’s Therapeutic Goods Administration (TGA) and unlock the opportunity for significant sales in Australia.

A successful outcome from the trial and the potential for TGA approval after dossier submission would make this possible.

🔄 PK Study results and Aqua Phase acquisition complete

⬜ Aqua Phase strategy

There are lots of paths that BOD could take with the Aqua Phase technology.

We want to see the company outline a strategy and identify some key markets or products to target (with the potential for clinical studies).

What could go wrong?

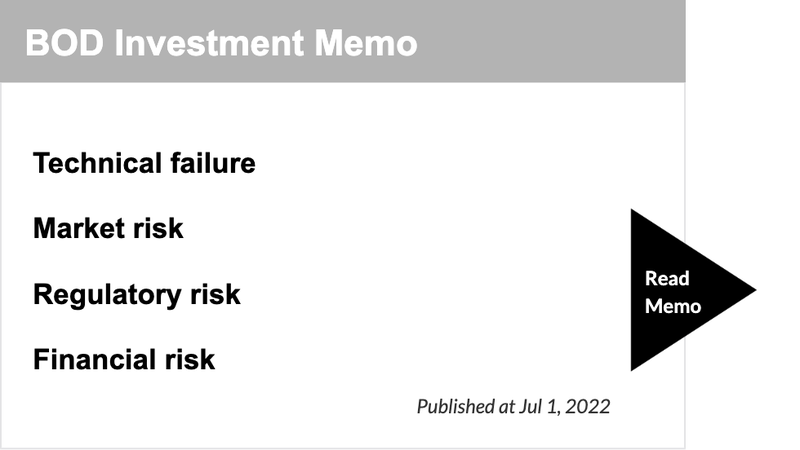

There are some key risks that we have highlighted in our BOD Investment Memo which are pertinent to its upcoming milestones.

Technical Failure - Insomnia Trial

There is a chance that BOD cannot prove in a clinical setting that its product is more effective than a placebo at treating insomnia.

There have been two other clinical studies like this before from ASX listed companies, Cann Group and EcoFibre.

Both trials failed to prove that the product worked compared to a placebo.

Regulatory - Insomnia Trial

BOD’s clinical trial is a Phase IIb, the results may show some evidence that its product is effective, but it may not be enough for the TGA to approve the treatment.

This will mean that BOD will have to conduct what is closer to a Phase III trial.

Market Risk - Insomnia Trial

If BOD’s Phase IIb clinical trial is successful, and approved for Special Access B Scheme by the TGA, it will be able to sell its products in pharmacies over-the-counter.

It does not confer any exclusivity, and if another player enters the market it will detract from BOD's market share in this space.

Due Diligence Risk - Aqua Phase

There is a chance that the Aqua Phase technology fails the PK studies. This could lead to BOD walking away from the acquisition.

Funding Risk - General

If the Aqua Phase technology successed BOD will be on the hook for £1M (~AUD$2M) to complete the sale.

As at 31st March 2023 BOD had AUD$3.3M in the bank.

As a small cap company generating limited revenues, BOD will likely need to tap the market for funding.

BOD’s Investment Memo

Below is our Investment Memo for BOD where you can find a short, high level summary of our reasons for Investing.

The ultimate purpose of the memo is to record our current thinking as a benchmark to assess the company's performance against our expectations for the following 12 months.

In our BOD Investment Memo, you’ll find:

- Key Objectives for BOD for the coming year

- Why we are Invested in BOD

- The key risks to our Investment Thesis

- Our Investment plan

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.