Market lull ahead of US non-farm payroll numbers

Published 03-FEB-2017 12:53 P.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

There was little action in global markets overnight, but what did emerge was in line with expectations. Arguably, the most important development was the Bank of England’s decision to keep rates on hold, but that was anticipated.

The FTSE 100 appeared to respond positively to the Bank of England’s decision, gaining 0.5%.

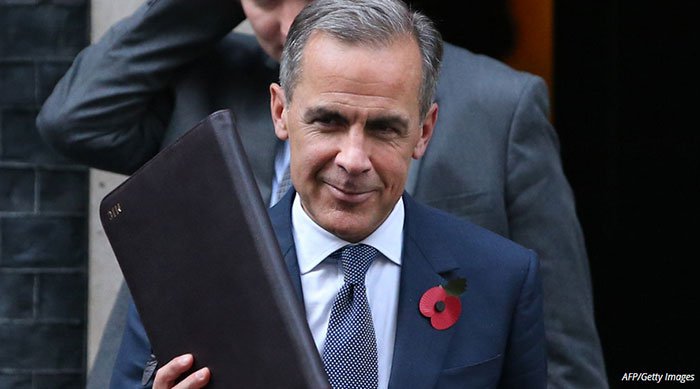

Perhaps it was BOE Governor Mark Carney’s rhetoric that prompted a significant fall in the British pound, as he indicated the likelihood of near-term rate rises were slight given the uncertainty that surrounds the Brexit transition and the current state of the economy.

Markets were also relatively flat in mainland Europe with the DAX the main mover as it came off nearly 0.3% to close at 11,627 points. The Paris CAC 40 was flat, closing at 4794 points.

Both the Dow and the NASDAQ were relatively flat, finishing just shy of the previous day’s close.

On the commodities front, there was a strong rally in gold in early trading as it increased from the previous day’s close of US$1208 per ounce to US$1228 per ounce. While it lost some of this momentum in afternoon trading, it is still up 0.7%.

The oil price was down 0.5%, looking to finish the week in a range between US$53 per barrel and US$54 per barrel.

Metals markets affected by Philippines government decision

Base metals were mixed with nickel and lead gaining ground, while zinc and copper came off slightly after what could only be described as a stellar week.

The Philippines government’s decision to order suspension of mining, predominantly in relation to nickel producers in the country is still to play out fully. There is the potential for nickel to rally on the back of this development, and this was evidenced in yesterday’s strong share price support for Western Areas and Independence Group.

Aside from commodities, one of the biggest moves in the last 24 hours has been the strengthening of the Australian dollar against the US dollar as it increased more than 1% from the previous day’s close of US$0.758 to hit a high of US$0.769, and there are signs that this run could continue.

This was triggered by yesterday’s trade figures which featured an all-time record trade surplus.

It should be noted that broker projections and price targets are only estimates and may not be met. Also, historical data in terms of earnings performance and/or share trading patterns should not be used as the basis for an investment as they may or may not be replicated. Those considering this stock should seek independent financial advice.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.