M&A activity tipped for the Cooper Basin

Published 18-SEP-2015 15:30 P.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

A leading oil and gas analyst has tipped merger and acquisition activity in the Cooper Basin on the back of ongoing strength on the east coast market.

EnergyQuest chief executive, Dr Graeme Bethune, said a drop in the share price in the companies in the basin had more to do with headlines about the oil price rather than market realities.

“The biggest falls have been for Cooper Basin players, averaging 70% and raising the likelihood of consolidation,” Dr Bethune said.

“This slump in share prices looks excessive.

“It is well ahead of the fall in oil prices of 42% in Australian dollars.”

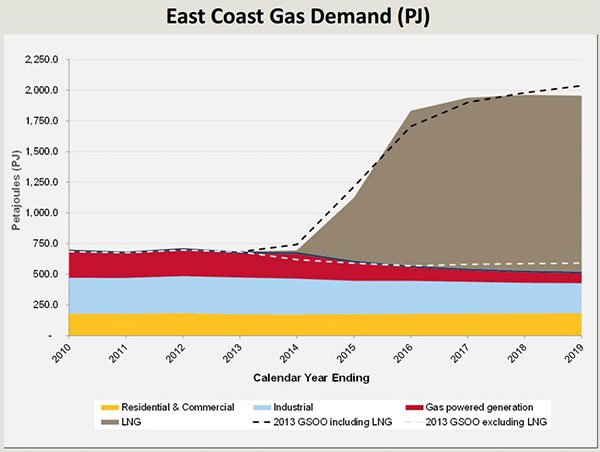

He also noted that the east coast gas market was one of the few tight gas markets in the world with increasing prices.

The European gas market is in the doldrums, US gas prices have slumped to US$2.77 per million British Thermal Units (A$3.70 per gigajoule), and LNG spot prices in Asia have halved.

“However, Australian east coast gas prices are increasing and small Cooper Basin players are actively developing new gas supply projects to meet strong east coast demand,” Dr Bethune said.

Demand profile for east coast gas market

“This presents great consolidation and takeover opportunities for new players with stronger balance sheets,” Dr Bethune said.

A good time for a junior?

The analysis has the potential to spark speculation of an impending wave of M&A in the Cooper Basin, with smaller companies looking attractive to bigger fish.

One such company, Real Energy (ASX:RLE) is thought to be close to naming a hydraulic fracturing contractor to conduct a vital 5-stage frac on its Tamarama-1 and Queenscliff-1 wells.

RLE previously told the market that an earlier independent study on the two wells at ATP927P had found that a five-stage frac would be most effective for maxiumum flow from the wells.

It subsequently told the market that it had opened up a tender process for contractors to compete for the job, which could potentially see a further firming up of the resource at the permit.

Independent experts DeGolyer and MacNaughton, based on the drilling of the un-fracced wells, said that the permit had an oil and gas in place resource of 13.76 trillion cubic feet of gas, up 141% on previous estimates.

The experts also said the permit has a contingent resource of up to 672 billion cubic feet.

However, getting the gas to flow following a frac job at the wells would firm up the numbers further and show the market that the gas can be produced.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.