Iron ore in for a correction?

Published 09-MAY-2016 15:28 P.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Iron ore has been on a run lately, but the party could be over according to new data on Chinese steel sentiment.

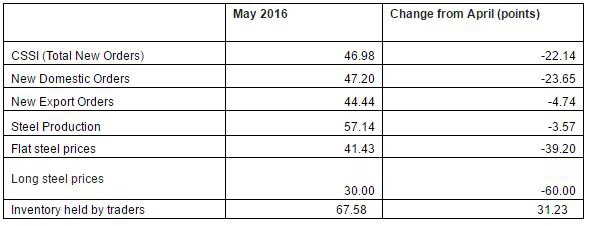

According to data compiled by S&P Global Platts, steel sentiment is set to take a dive over May as weak domestic demand starts to bite.

Its index measures the sentiment in the Chinese market (70-85 China based market participants) on the likelihood of the domestic demand for steel going up or down, with a measure of less than 50 a decrease.

The bad news for iron ore bulls is that for the month of May, S&P Global Platts has measured domestic steel demand at 47.20, a contraction.

That’s a 23.65 point decrease from April, and comes as the amount of inventory held by traders jumps up to 67.68 on the index – a 31.23 point increase on the previous month.

It could be a short term measure, but S&P Global Platts’ steel and raw materials editor Paul Bartholomew thinks it could be the start of something.

“The big downturn in the outlook for domestic steel orders and prices is the big concern and unfortunately all the ingredients for a price correction appear to be in place, judging by the results of the index,” he said.

“The big and sudden shift from optimism to pessimism – particularly in the outlook for construction steel prices – is further indication of how sentiment driven the market has become.”

If steel sentiment in China is down, that is more than likely going to spell at least short-term trouble for iron ore producers in Australia – given Australia’s iron ore feeds the Chinese steel market.

Iron Ore has been on somewhat of a bull run since the start of the year, increasing from about $41 per tonne on the spot market to about $61 at last close.

It’s unclear whether the S&P Global Platts report in itself will have a massive effect on the price in the short term, but if the sentiment holds true then over the short-to-medium term cold water could be poured on the recovery.

Back in March the Chinese government gave the iron ore price a shot in the arm by unveiling an ambitious infrastructure program.

It officially targeted growth of 6.5% to 7%, seen as quite bullish, suggesting that the government would keep the foot on the accelerator rather than cool down.

As part of its infrastructure plans, it promised an 800 billion yuan ($A163.3 billion) spend on railways, and 1.65 trillion yuan on building roads – both of which require steel and therefore require iron ore.

But, it did prompt fresh concerns about the level of debt China was taking on.

Spiralling debt from Chinese private companies meant private debt is thought to be more than 200% of GDP – and that debt was run up constructing new buildings, roads, and rail.

So a brand new infrastructure spend when private companies are already over-leveraged?

In any case, it’s clear from the steel sentiment that any positive effects from the infrastructure spend announcement has run its course – and it’s likely that until individual projects are announced and steel rolls out of factories that the road for iron ore will continue to be a bumpy one.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.