Introducing Our Latest Investment: OKR

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,633,334 OKR shares at the time of publishing this article. The Company has been engaged by OKR to share our commentary on the progress of our Investment in OKR over time.

Today we announce our latest Investment.

The USA is desperate to secure domestic energy sources, and not rely on other countries such as Russia and China, specifically for uranium enrichment capabilities.

The USA has recently introduced several bills and significant funding to support its nuclear industry by securing uranium and uranium enrichment capability domestically.

We believe this will drive significant demand, investor attention and financing to uranium companies with USA based projects plus enrichment capabilities.

Our new Investment is in Okapi Resources (ASX:OKR) - a uranium explorer and developer with projects across four North American uranium districts (USA, Canada).

OKR is also finalising a material stake in uranium enrichment technology in the coming weeks.

This technology is a chemical process which could make uranium enrichment more efficient, safer and cheaper than other enrichment technologies.

One of our key Investment themes for 2023 is critical materials in the USA - specifically for energy and resource independence in a rapidly de-globalising world.

OKR offers uranium enrichment technology combined with JORC-stage USA based uranium assets.

OKR’s uranium enrichment exposure is particularly unique for the ASX.

Capped at ~$27M, OKR is the only ASX listed micro cap with an investment in the space.

The other ASX ‘uranium enrichment’ stock has gone from a $35M to a $1BN market cap in recent years.

Uranium “enrichment” is basically applying an advanced process to raw uranium (that is mined out of the ground) to enhance the concentration of its key element enough to be used as the fuel in nuclear reactors.

Uranium enrichment technologies and processes are closely guarded secrets.

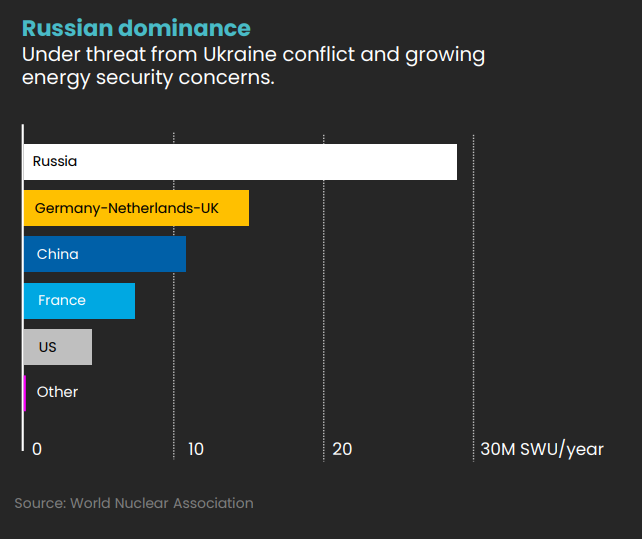

Russia controls ~38% of the world’s enrichment capacity. China controls ~25%.

According to Reuters: U.S. uranium enrichment capability has dwindled to nothing in recent decades as it leaned on other countries to supply the fuel.

The US is most vulnerable to supply chain shocks in the uranium industry because it has the world's largest nuclear reactor fleet - nuclear power accounts for ~20% of electricity production in the US.

Late last week the US introduced the Nuclear Fuel Security Act (NFSA). This Act aims to establish domestic nuclear fuel production to protect against a disruption of Russian supplied “enriched” uranium.

At almost the same time, a US bill (H.R.1042) was proposed to ban imports of enriched uranium from Russia.

OKR has exposure to North American uranium across:

- JORC stage uranium projects inside the USA - 49.8m lb JORC uranium resource in Colorado.

- Exploration projects in the Athabasca basin, Canada - A region that is home to the world's highest grade uranium and ~20% of the world's uranium supply. Canada is politically friendly with the USA.

- ~20% shareholding in uranium enrichment tech - the blue sky upside for the company. This deal is set to complete in the coming weeks now that financing has been secured.

OKR also fits with another of our 2023 Investment themes: adding exposure to more later stage companies to our Portfolio, which can begin production sooner in the current commodities supercycle - our Investment in OKR will be added to our Wise Owl Portfolio.

OKR aims to capitalise on more than $2 trillion in macroeconomic tailwinds.

That $2 trillion comes in the form of US government initiatives as the country launches an all-out push to re-shore its supply chains amid an energy transition, a war and other geopolitical friction.

- Inflation Reduction Act (IRA): ~US$400 over the next 10 years towards clean energy technologies and supply chains INSIDE the US.

- Bipartisan Infrastructure Law (BIL): US$1.2 trillion over the next 10 years on US based infrastructure.

- CHIPS & Science Act:~US$280 billion over the next 10 years on domestic semiconductor manufacturing, R&D and wireless supply chains.

Alongside those policies - and more importantly for OKR, the US is also looking to push billions of dollars in support for the nuclear industry including:

- US strategic uranium reserve: $1.5BN over 10 years to buy local uranium

- US$6BN in funding allocated to keep old Nuclear reactors online.

In our view OKR is well placed to capitalise on these tailwinds ...IF it can successfully execute on its plan and strategy.

As always there are risks in this Investment that we outline in our ORK Investment Memo.

There are two arms of OKR’s strategy:

- Advance its uranium enrichment technology with its technology partner

- Exploration, consolidation and development of its North American uranium assets

Today we add OKR to our Wise Owl portfolio and share our initial OKR Investment memo, including:

- Why we Invested in OKR

- Our long term Big Bet - what we think the upside Investment case for OKR is.

- The key objectives we want the company to achieve over the next 12 months,

- The key risks to our Investment thesis

- Our Investment Plan.

After the Investment memo, today we will also look at:

- What is Uranium enrichment and why is OKR’s enrichment technology stake important?

- Comparison of $27M OKR and $1BN Silex

- Look at how US is completely dependent on foreign uranium and enrichment and what it means for OKR

- A look at OKR’s North American uranium assets

- What’s next for OKR

Here is our initial Investment Memo for OKR:

Why we Invested:

(1) The US is completely dependent on foreign uranium and uranium enrichment. It’s making domestic uranium assets and enrichment a national priority

OKR has projects across four North American uranium districts, in addition to its 19.9% stake in an enrichment technology company. We think the combination of technology and assets will make OKR attractive to acquisitive uranium majors and governments as a target of funding.

(2) The only other ASX uranium peer with enrichment technology is capped at $1BN with 51% ownership of its technology

Silex Systems is OKR’s only “uranium enrichment peer” on the ASX.

Silex has re-rated from a market cap of ~$35M to a ~$1BN in the space of two years on the back of US government initiatives, technical advancements and geopolitical factors.

Silex owns a 51% stake in an enrichment technology JV with Canadian uranium major Cameco (who holds the other 49%).

OKR is set to own 19.9% of its enrichment technology and is currently capped at ~ $25M.

If OKR is able to validate, scale up, and get regulatory approvals for its tech, we think it could follow a similar trajectory to Silex over time as the enrichment technology matures and is proven to work at scale.

(3) OKR has a 49.8Mlbs uranium JORC resource in the USA - development potential

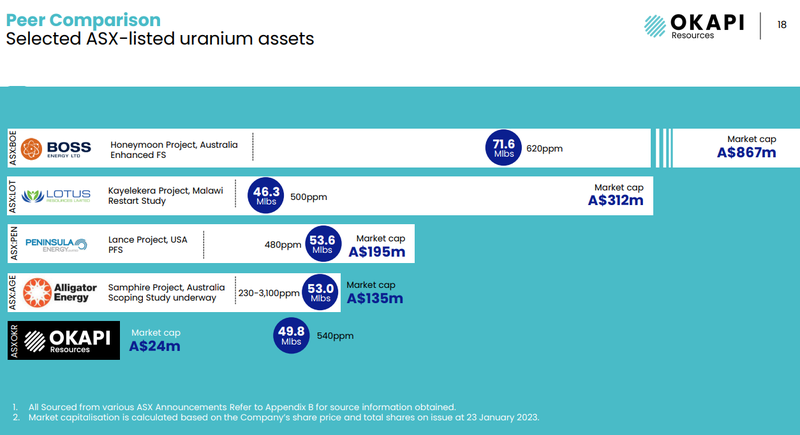

Located in Colorado, USA, OKR’s most advanced US uranium project has a JORC resource of 49.8Mlbs at a grade of 540ppm. Should future drilling be successful here, we think this project could move into a scoping study down the track.

(4) Low EV relative to other uranium peers, and none have enrichment exposure

Following completion of OKR’s February 2023 capital raise ($5M) and subsequent payment for its stake in the enrichment technology ($3.1M), OKR will be trading on an Enterprise Value (EV) of ~$23M (assuming a 15c share price).

OKR currently has a total JORC resource base of 49.8Mlb. On a pure “pounds in the ground”/EV basis, this compares favourably with other ASX uranium peers such as Peninsula Energy (53.6Mlbs, ~$170M EV) and Alligator Energy (53Mlbs, ~$113M EV). While these two peers are more advanced in developing their assets, OKR is the only one with exposure to uranium enrichment.

(5) Highly prospective uranium exploration ground in Canada’s largest uranium producing district

The Athabasca Basin in Canada is home to some of the worlds highest grade uranium projects and produces ~20% of the world’s uranium. We see drilling success in Canada as a significant source of upside if a major discovery is made here.

(6) Strong Management and Board, with North America focus

We are impressed with Managing Director Andrew Ferrier’s background in private equity where he was focussed on managing US uranium assets and investments, as well as his degree in chemical engineering. We think this makes him well suited to understanding the significance of the enrichment technology, and how to get uranium deals done in the US.

OKR Chairman Brian Hill has 35 plus years experience, including a stint as Executive VP Operations at Newmont Mining Corporation (US$36BN market cap).

We also note the OKR management team’s significant US mining experience and in-country team - this is important for getting projects advanced as quickly as possible.

(7) Tight, loyal register

With a relatively low number of shares on Issue, we think the capital structure of OKR is set up well for a re-rate if the company can deliver milestones and/or macro factors bring more market attention to uranium. We think OKR has been flying a little under the radar up until now and the story is going to get bigger in 2023.

(8) Advanced stage company

OKR is not just an exploration company - as noted above, it has a JORC stage Uranium project and a stake in uranium Enrichment technology. This fits with our 2023 Investment theme of adding exposure to more later stage companies to our Portfolio, which could begin production sooner in the current commodities supercycle.

Our Big Bet:

“OKR re-rates to a +$250M market cap by achieving a major technological breakthrough with its uranium enrichment technology and/or is acquired at multiples of our Entry Price by a US focussed uranium major looking to gain access to its assets and technology”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our OKR Investment Memo.

What do we expect OKR to deliver?

Objective #1: Advance enrichment technology

We want to see OKR advance its enrichment technology with its partner to make it attractive and viable in the eyes of uranium majors and the US government and/or other friendly countries.

Milestones:

🔲 Further validation and extend the enrichment performance (show how well it works)

🔲 Achieve continuous operation at bench scale (scale up process)

Objective #2: Regulatory approvals - to let OKR and tech partner negotiate with multinationals

According to OKR, an enrichment plant currently cannot be built in Australia under current regulation and no government arrangements have been sought to export the technology. We think ultimately the US will be most interested in this technology and we want to see regulatory accommodation for OKR’s technology partner’s process.

Milestones:

🔲 Regulatory approvals to conduction discussions with overseas companies

Objective #3: Drill at least two projects

OKR has a portfolio of US based uranium assets at different levels of maturity (3 projects across Colorado and Utah) it also has ground in the Athabasca Basin (6 projects), Canada, a prolific uranium region. We want to see OKR drill at least two of these projects. Drilling is what will ultimately build value and scale in its assets.

Milestones:

🔲 Drilling campaign delivered

🔲 Drill results reported

Objective #4: Deliver at least one resource upgrade

We want to see OKR deliver a resource upgrade, which we think will most likely be at its most advanced project in Colorado, however priorities may change based on exploration success.

Milestones:

🔲 Resource upgrade

Objective #5: Advance development studies on at least one project

We want to see OKR move at least one project into a scoping study or preliminary economic assessment - the first steps on the path to developing a project.

Milestones:

🔲 Scoping study or preliminary economic assessment commenced

Objective #6: Acquire more prospective uranium projects

We think OKR has a keen eye for uranium projects and strong relationships in the US. We want to see OKR consolidate/expand its position at existing projects or acquire additional projects to build up its portfolio of North American uranium assets

🔲 Consolidation/expansion of existing projects (additional ground or rights acquired)

🔲 New project acquisition

What are the risks?

Technology risk - it's possible that OKR’s stake in its technology partner doesn’t work out. OKR could fail to secure regulatory approvals, the technology could struggle to scale up, or the technology partner fails to validate the efficiency improvements it brings at scale.

Intellectual property risk - via its stake in its technology partner, OKR has its hands on a piece of a highly regulated, classified technology. The technology could be the subject of intellectual property theft.

Exploration risk - there is no guarantee that OKR’s upcoming drill programs in North America are successful and OKR fails to find economic uranium deposits.

Permitting risk - OKR needs to acquire permits to drill its projects and maintain its social license to operate. Not getting permits could prevent drilling and local stakeholders will need to be engaged if it seeks to develop a uranium mine in North America. These stakeholders might not approve of a uranium mine in their area.

Market risk (macro) - the broader market could sell down or crash, impacting the risk appetite of market participants and hurt the OKR share price.

Commodity price risk - the uranium price could fall, or fail to rise enough to make OKR’s US assets viable.

Uranium and nuclear sentiment risk - A large nuclear incident (such as Fukushima in the past) could make nuclear power unfavourable for a period, and set back the industry.

Geopolitical/political risk - friction between the major powers could decrease, in turn impacting the urgency of US initiatives to secure domestic uranium supply and enrichment capacity. Alternatively, key legislation could fail to pass.

Delay risk - both technology and drilling progress could be delayed and the market could sell down OKR on a lack of material newsflow.

Funding risk - as a small cap, OKR is reliant on capital markets to advance its projects. If some, any or all of the risks above materialise OKR could struggle to access capital.

What is our Investment Plan?

Our plan is to hold the majority of our position in OKR for 3 to 5 years in the hope of an acquisition by a major company after the project is de-risked (see “our long term bet” above).

Over the next 12 months we will apply our standard de-risking strategy for early stage companies.

We may look to sell 20% of our holding if the company delivers on one or more of the above objectives and the share price materially re-rates. Any sell downs will be in accordance with our trading and hold policy disclosure.

Our OKR Progress Tracker

Below is our OKR Progress Tracker document.

We will be using this internally to keep up to tabs on the company's progress.

What is Uranium enrichment and why is OKR’s enrichment technology stake important?

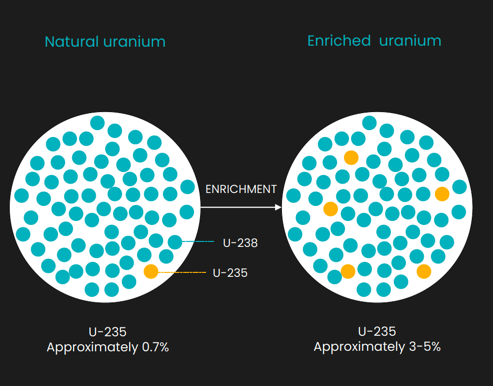

Before uranium can be used in nuclear reactors it needs to be “enriched” - an industrial process that brings natural uranium, which contains only 0.7% of U-235 (Uranium-235), to a uranium content of 3-5%.

Increasing the concentration of Uranium-235 is what makes uranium valuable in the nuclear reactor fuel cycle.

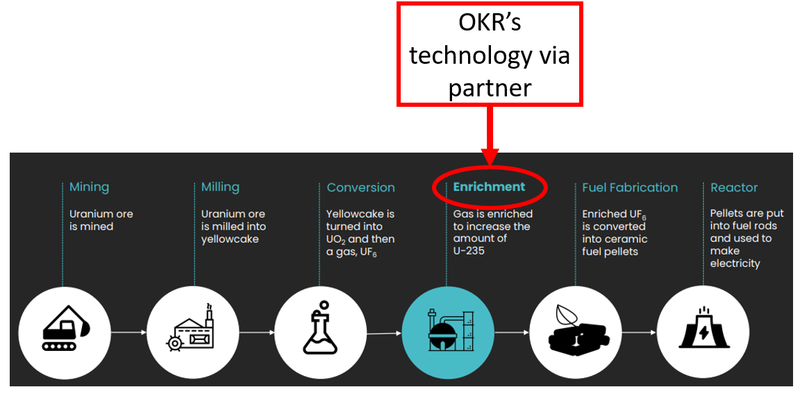

Enrichment is an important part of a multi-step process to take the raw material through to a form which can be used in nuclear reactors:

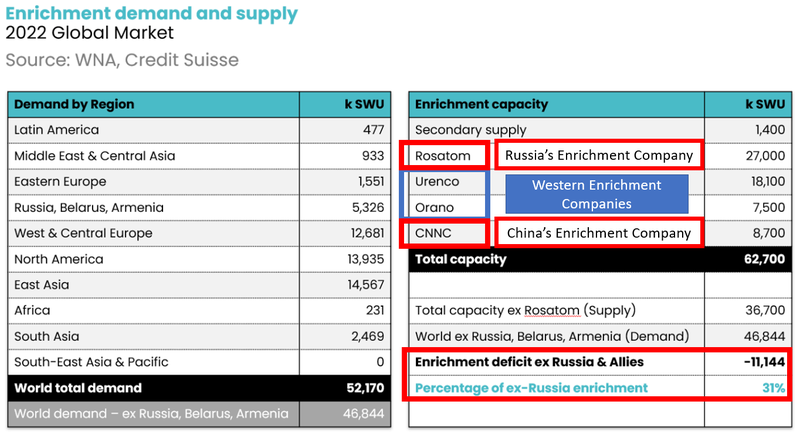

The uranium enrichment industry is controlled by four major companies. None of those companies are US based.

The biggest players in the enrichment space are based out of Russia who control ~38% of the market.

Below is a quick summary of the companies that have enrichment capacity in the world matched up against sources of demand:

Quick takeaway: Russia and China dominate the global uranium enrichment market with a combined 63% of global capacity - and there’s a big squeeze going on in the West for enrichment capacity.

The enrichment capacity crunch could be exacerbated by new technology as well.

In addition to the standard level of enrichment - Small Modular Reactors would require a 19.5% threshold to be reached.

These reactors are part of the next generation of nuclear reactors - Bill Gates and Warren Buffer have put a large amount of money behind developing this technology and we expect these reactors to become more widespread in the future.

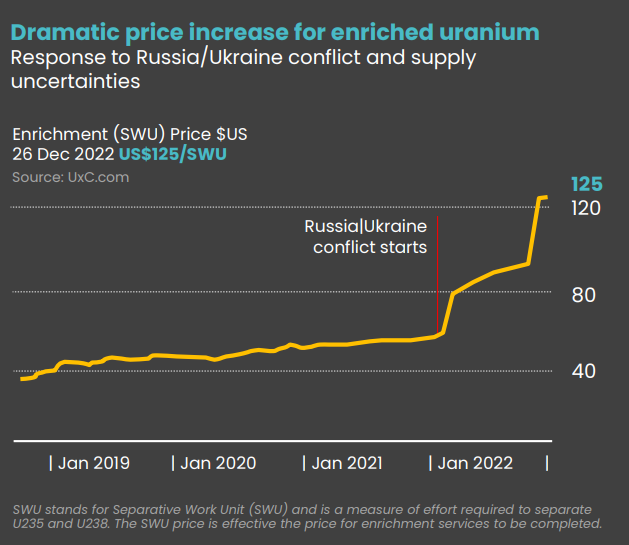

As a result, we see significant growth ahead for the $6BN enrichment market - which experienced a serious price crunch from the outset of the Russia/Ukraine war:

Here’s where OKR comes in...

Once mined, it needs to be “enriched” before it can be used in nuclear power stations (more on this process in the next section).

Silex stands for Separation of Isotopes by Laser EXcitation - yes, they actually use lasers to enrich uranium.

OKR’s uranium enrichment technology partner, on the other hand, is developing a chemical process to make enrichment more efficient, safer and cheaper than other enrichment technologies.

Because it's a chemical process, there’s no need for lasers and OKR says there’s no significant heating, cooling or high pressures involved and the process can be built from readily available components.

What’s more, OKR says that the “enrichment factor is between 10 and 30 times higher than that of previous chemical enrichment technologies developed in France and Japan”.

All of that sounds potentially revolutionary - but it’s also a bit of a black box right now.

Meaning, we don’t know the specifics of how the technology works because it's classified (see risks section).

We note that after the technology partner lodged a patent in 2018, the Australian Safeguards and Non-Proliferation Office and Defence Export controls now regulate all “technical disclosure”.

But we see this as an early sign of the technology's merits, because the Australian government is closely guarding it.

Ideally, OKR’s technology partner gets its technology to the US - so there may need to be regulatory accommodation for export.

As a result, regulatory developments will be key for OKR (see Objective #2 in our OKR Investment Memo).

Two ASX uranium enrichment stocks: Comparison of $27M OKR and $1BN Silex

Again, with regards to OKR’s enrichment side of the business, OKR is the only micro cap with exposure to uranium enrichment on the ASX.

And the only other ASX listed company with exposure to uranium enrichment is ~$1BN capped Silex Systems.

As we said above, Silex Systems has re-rated from a market cap of ~$35M to a ~$1BN market cap in the space of two years on the back of US government initiatives, technical advancements and the Russia/Ukraine war.

Silex owns a 51% stake in an enrichment technology JV with Canadian uranium major Cameco (holds the other 49%) - so the market is effectively valuing its technology at ~$2BN.

Silex is a powerful example of what happens when a commodity macro theme collides with a technology macro theme.

In a sign of how strong these macro thematics are, since the Russia/Ukraine conflict Silex’s share price has risen from ~$1.14 per share to $4.84 per share.

In light of what Silex has achieved, we think the enrichment story could be a source of “blue sky” upside for OKR over the long run.

Always remember though, just because Silex has performed well does not indicate that OKR will achieve similar success - this is just a potential comparison.

This technology could prove to be better than Silex’s technology, worse, comparable or anything in between - its classified tech.

The proof will be the degree to which uranium majors and governments move to invest in/support OKR’s and their technology partner.

For example, a big equity stake in OKR from a uranium major would be important validation of the tech - as would regulatory approval to expand the operation in Australia or discussions with the US Department of Energy.

Whatever happens, we’ll be watching closely for these types of signals.

How the USA is completely dependent on foreign uranium and enrichment and what it means for OKR

The story in the US starts with the geopolitical events of February 2022 and what followed.

In the fallout of the Russia/Ukraine conflict the US, Europe and other Western countries all introduced sanctions targeting Russia’s energy industry (oil, gas, goal etc).

One sector that wasn't at all sanctioned was the uranium sector.

Until last week, the uranium industry has flown under the radar of sanctions.

This isn’t because the US forgot about it or because it isn't important to anyone... rather, it’s because there is just no alternative to replace the supply of enriched uranium that comes out of Russia and China.

And as for the supply of raw uranium, most of the world's direct (mined) supply doesn't actually come out of Russia, making it only a second order target of sanctions.

Targeted first were things like oil and gas produced in Russia and sold to the world. The uranium market works a bit differently.

Russia doesn't directly control uranium mine supply, instead it controls the more opaque (but significantly more important) uranium enrichment industry.

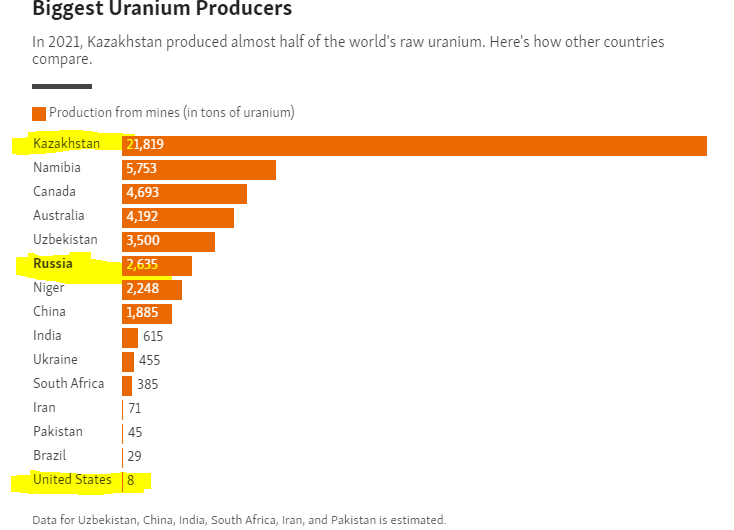

As of 2021 Kazakhstan produced over 50% of the world's raw uranium supply. The US, on the other hand, produces barely any.

Mined uranium on its own is not useful as a fuel for nuclear reactors.

This is where the Russia/China dominance comes into play.

Together the two countries control ~63% of global enrichment capacity.

As is the case for mined uranium production, again the US has very little domestic enrichment capacity:

The answer to why sanctions were never placed on the uranium supply chain is relatively simple: the US and the West simply can't replace the enriched uranium supply coming out of Russia and China.

Again, the US is most vulnerable to uranium industry supply chain shocks because it has the world's largest nuclear reactor fleet - nuclear power accounts for ~20% of electricity production in the US.

Turning off its key supply routes via sanctions would be like shooting its domestic nuclear power industry in the foot.

Yet this week, the US took the first steps towards doing just that...

US senators Joe Manchin and John Barrasso (both from the senate energy and natural resources committee) this week introduced the Nuclear Fuel Security Act (NFSA).

The bill’s ultimate purpose being, “To establish a nuclear fuel program with the purpose of onshoring nuclear fuel production to ensure a disruption in Russian uranium supply would not impact the development of advanced reactors or the operation of the United States’ light-water reactor fleet”.

Senator Manchin’s comment is enough to tell the story, “American energy security and independence is impossible when we continue to rely on Russia and Vladimir Putin for the uranium we need to power our nuclear reactors”.

The CEO of $2.1BN US-based developer Uranium Energy Corporation, which holds projects next door to our earlier stage US-based uranium exploration Investment, GTI Energy (ASX: GTR), jumped on the news with the following tweet.

Here we go.

— Amir Adnani (@AmirAdnani) February 15, 2023

House Energy & Commerce Committee bill has been introduced (HR-1042) to immediately ban Russian low-enriched #uranium into the U.S. 🇺🇸

👉 https://t.co/pk6JHPWN0a pic.twitter.com/pPU3bSlQfd

With this, we think the macro environment for uranium is approaching an inflection point where the momentum, especially inside the US/North America, starts to increase exponentially.

There remains significant US domestic demand from its existing mature nuclear power fleet. And now, the introduction of the Inflation Reduction Act brings ~US$400BN in government incentives into law to develop domestic clean energy supply chains.

Of note, US$700M of that funding is being specifically directed to the enrichment space.

Adding this all up - we think that one of the best places to Invest in the uranium sector is in the US/North America.

And we think our latest Investment in OKR offers exposure at an appropriate valuation for what's to come in the uranium enrichment space over the next 2+ years.

That’s because OKR addresses BOTH the domestic raw material aspect AND the enrichment side of this macro theme.

Here’s a quick rundown of OKR’s North American assets and why they are so important right now.

OKR’s North American uranium assets

We see OKR’s drilling at its North American uranium assets as also very important because this will make up much of its near term news flow.

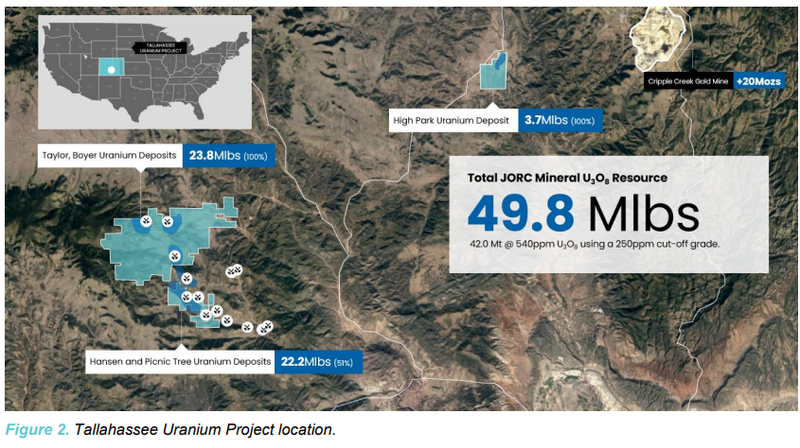

OKR’s most advanced project is called Tallahassee and is in Colorado - It has a JORC resource of 49.8Mlbs at a grade of 540ppm.

Should future drilling be successful here, we think this project could move into a scoping study down the track.

The Tallahassee project makes up the resources in this peer comparison slide in the latest OKR slide deck:

As above OKR’s market cap is significantly less than its peers, in part reflective of its peers being more advanced in the development of these projects.

Our hope is that OKR can progressively re-rate in line with these peers by moving its most advanced project in Colorado into development along with a potential resource upgrade after future drilling - a permit is in place for 18,200m across 60 drill holes.

We’d also be looking for OKR to potentially consolidate its ground here and up its pounds in the ground - at the moment OKR’s Hansen and Picnic Tree deposits are 51% owned.

Below is a map of the Tallahassee project in Colorado:

The other two US projects are split across two other uranium districts in Utah and Colorado.

These are the recently acquired Maybell (Colorado) project and the Rattler project (Utah):

Maybell (Colorado) is in a uranium district that has historical production of 5.3 million pounds of uranium at an average grade 1,300ppm.

The Utah project is 85km north of White Mesa Uranium/ Vanadium mill – the only operating conventional uranium mill in the USA.

We won’t dive into these assets today, but suffice to say, we think they are highly prospective and well located.

Finally, we are particularly attracted to OKR’s projects in Canada - Canada is a friendly country to the USA so this location fits well with our Investment thesis.

OKR has 6 projects in the Athabasca Basin which is home to the world's highest grade uranium and ~20% of the world's uranium supply.

OKR plans to get on the ground and run airborne geophysics in the Athabasca Basin in March 2023.

What’s next for OKR?

This is what we think the near-term newsflow for OKR will look like:

🔄 Geophysics at Athabasca Basin

A program to identify the best drill targets at projects located in the same district that hosts the Cigar Lake Mine owned by uranium major Cameco

🔄 Drilling at most advanced project in Colorado

A permit is in place for 18,200m across 60 drill holes - we want to see OKR firm up a timeline for this drilling.

🔄 Drilling at second Colorado project

At the Maybell project OKR has engaged a company called BRS Engineering to work over historical data - the company has direct experience at the Maybell Project when it was operating. We’d be looking for a drill program in H2 2023

🔄 Drilling at Athabasca Basin

Following geophysics results which are due in Q2 2023, we expect OKR to drill its most promising projects in Canada later this year.

🔄 Progress on enrichment tech

Scientific progress and regulatory approvals aren’t linear processes but we are looking for one of the following three things to happen on the enrichment front:

🔲 Further validation and extend the enrichment performance (show how well it works)

🔲 Achieve continuous operation at bench scale (scale up process)

🔲 Regulatory approvals

Our OKR Investment Memo:

Below is our Investment Memo for OKR where you can find a short, high level summary of our reasons for Investing.

The ultimate purpose of the memo is to track the progress of our Portfolio companies using our Investment Memo as a benchmark.

In our OKR Investment Memo you’ll find:

- Key objectives for OKR in 2022

- Why we Invested in OKR

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.