Broker share price target suggests Matador offers 200% upside

Published 18-MAR-2020 10:18 A.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Hartleys’ resources analyst Paul Howard has released an upbeat report on Matador Mining Ltd (ASX:MZZ), valuing its assets at 43 cents per share and attributing a 12 month price target of 38 cents per share to the stock.

This compares with Tuesday’s closing price of 12.5 cents - it should be noted though, that the Matador story may be starting to resonate as its shares surged 20% yesterday.

It was just last month that the company significantly increased the mineral resource at its Cape Ray Gold Project in Newfoundland, Canada.

The 18% increase in contained gold metal followed a 12,600 metre drilling program conducted in 2019.

Matador’s tenure covers 80 kilometres of continuous strike along the highly prospective Cape Ray Shear.

Within the package is a 14 kilometre zone of drilled strike which hosts a JORC resource of 16.6 million tonnes at 2.2 g/t for 1.2 million ounces gold.

Upcoming scoping study should highlight value

This is an under explored tenure, with only a small portion of the 80 kilometre strike previously drilled.

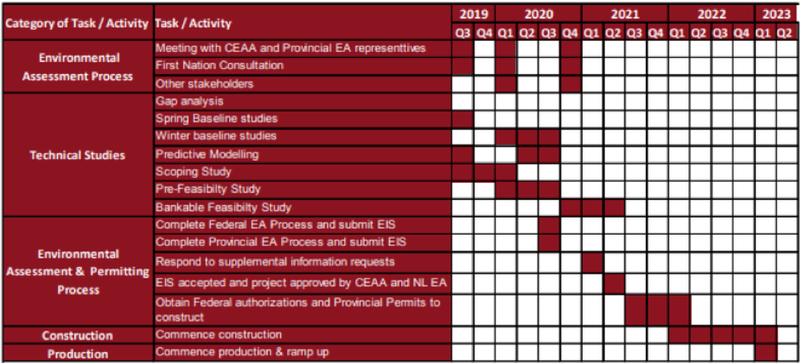

With a number of key operational and environmental studies targeted for completion in 2020, the next 12 months is shaping up as a very full year for Matador.

We have already touched on the issue of environmental assessments, but from an operational viewpoint, 2020 is a watershed year for the group.

As indicated below, the scoping study is due for completion in the March quarter and the prefeasibility study should be prepared by the September quarter, with the latter being an important indicator of the economic viability of the project.

Hartleys crunches the numbers

In assessing the project, Howard said, ‘’Matador has a conceptual exploration target of 30-36Mt grading 1.4 to 2.4 g/t Au for 1.3Moz to 2.8Moz across the 80km of ground it holds along the Cape Ray Shear Zone.

‘’Of this, 5km contains its 1.2Moz resource with extensions likely at depth and along strike.

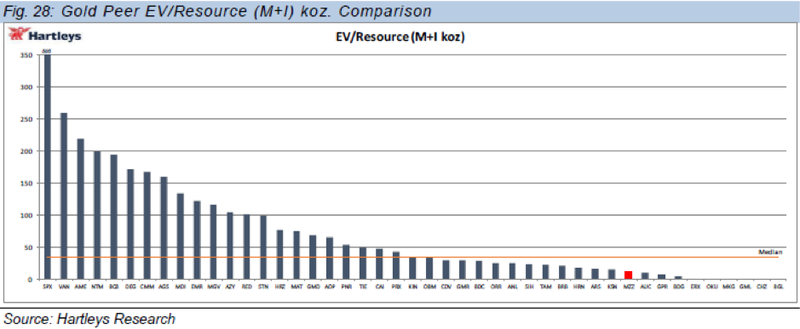

‘’On EV/M&I resource (enterprise value to measured and indicated resource), MZZ is a strong buy but is still to release a formal study and hence presents some risk, as does current market conditions (i.e. Coronavirus impact).

‘’However, at 2.2g/t gold, Cape Ray is the highest grade, sole open pit resource of the 45 ASX-listed companies we have reviewed.

‘’We therefore initiate coverage with a Speculative Buy recommendation.’’

The following graph highlights Matador’s heavily discounted valuation compared with its peers based on enterprise value to resource ounce metrics.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.