Broker notes relevance for Metminco following Continental Gold takeover

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

News released at the start of the week by Columbian gold developer Continental Gold Inc (TSX:CNL) regarding the proposed acquisition by Zijin Mining Group Co Ltd (SSE:601899; SEHK:2899) would have been welcomed by Metminco Limited (ASX:MNC).

Under the terms of a definitive agreement between Continental and Zijin, the latter has agreed to acquire all of the outstanding shares of Continental at a price of C$5.50 per share.

The implied value of the transaction is C$1.4 billion, and the offer price represented a premium of 29% to the company’s 20 day volume weighted average price (VWAP) as at 29 November, 2019.

Continental chief executive Ari Sussman not only highlighted his satisfaction regarding the offer, but he also pointed to the progress the company had made in taking the Buriticá Project from a grassroots discovery to one of the world’s largest and highest grade gold projects.

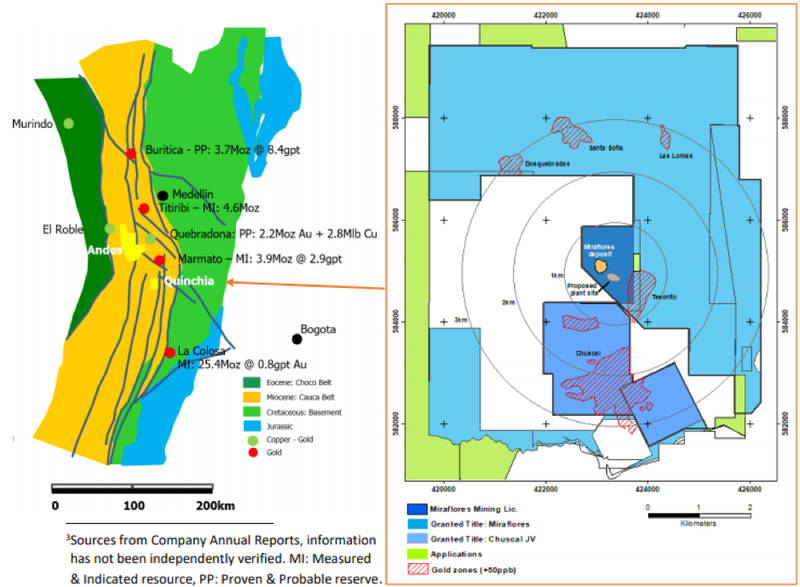

Metminco recently identified Colombia as its key focus following a strategic review and identified the Mid-Cauca belt of Colombia, which hosts several multi-million ounce epithermal gold and porphyry gold-copper discoveries, as its target area.

Note the location of the Chuscal target at the Quinchia Project and its proximity to major regional gold discoveries, including Buriticá to the north and the nearby 3.9 million ounce Marmato Project.

Metminco’s gold in ground carries substantial value

Analysts from UK-based broking house SP Angel which provides extensive research on the global mining sector were upbeat about the news in relation to other miners active in that area of Colombia, including Metminco and Orosur Mining.

Part of their take on the development was as follows:

‘’As well as offering an up to date insight into current industry valuation yardsticks for gold assets, we anticipate that Zijin’s move may stimulate attention towards the gold exploration potential of Colombia and of the mid-Cauca belt in particular which hosts other deposits.

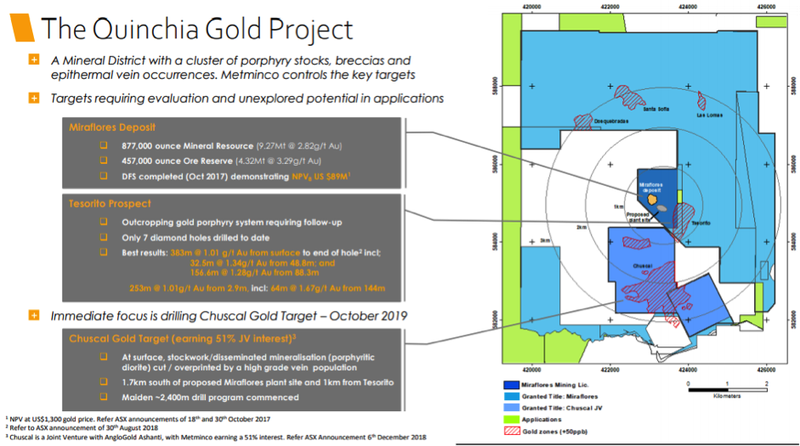

‘’These include the San Ramon deposit of the former Red Eagle Mining (reserves – 2.4 million tonnes averaging 5.2 g/t gold), Orosur Mining’s Anza deposit, where the consultants, MDA have identified a formal “exploration target” of between 1.6 and 2.3 million tonnes at grades ranging between 3.2 and 3.7 g/t gold over a small portion of the identified strike extent of the mineralisation, and Metminco’s Miraflores deposit which, following some 40,000 metres of drilling, currently reports 877,000 ounces of resources.

Crunching the numbers

Continental Gold is still not in production, but it has a sizeable resource of 5.3 million ounces of gold.

Excluding the company’s 21 million ounces of silver, the takeover offer values Continental Gold’s resource at US$200 per ounce of resource.

If such a value was applied to Metminco’s Miraflores deposit which has a resource of 877,000 ounces (9.3 million tonnes at 2.8 g/t gold), it would represent a value of approximately $175 million.

It should also be noted that Miraflores has a reserve of 407,000 ounces gold.

If Metminco were to trade in line with the gold in ground valuation, its shares would be trading in the vicinity of $1.00.

Though a direct correlation can’t be made, the metrics definitely indicate that Metminco’s valuation is representative of its exploration potential rather than its gold in ground, a much more tangible asset, particularly the higher confidence reserves resource which using the same valuation metrics is worth more than $80 million.

By comparison, Metminco has a market capitalisation of about $17 million.

Of course any valuation is speculative.

Early stage drilling results from the Chuscal Gold Target, located in the Mid-Cauca Porphyry Belt have been promising with the first drill hole passing through an extensive 350 metre wide mineralised zone from surface.

A number of intervals intersected impressive grades including 6 metres at 2.5 g/t gold and 10.2 g/t silver close to surface.

As is often the case with this style of mineralisation, the grades improved at depth with gold up to 6.4 g/t gold and silver grades as high as 87.4 g/t.

Commenting on the recent results, managing director Jason Stirbinskis said, “This is a remarkably strong result on our first hole given the extent of the mineralisation encountered from surface, and it has proven very illuminating, greatly improving our understanding of the geology.

‘’After outstanding drill success last year at the nearby Tesorito porphyry discovery, including a best result of 253.1 metres at 1.01 g/t gold from surface, including a higher grade zone of 64 metres at 1.67 g/t gold, and now hitting this wide interval at Chuscal, we believe we are in enviable porphyry territory.

‘’It remains early days into our drilling at Chuscal, but this first intersection has certainly provided very strong encouragement about what Chuscal could be when you consider the sheer scale of the gold anomaly at surface, the impressive widths of mineralisation encountered and its location in the heart of the Mid-Cauca belt, which is already host to several multi-million ounce porphyry and epithermal deposits.

‘’When compared to other global porphyry systems and recent discoveries, this early result reaffirms our view that our Quinchia Project and Chuscal in particular, have great potential”.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.