Big Oil enters the lithium game… Mandrake was there first

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,150,000 MAN shares and staff own 35,714 MAN shares at the time of publishing this article. The Company has been engaged by MAN to share our commentary on the progress of our Investment in MAN over time.

Some abandoned oil fields contain lithium rich brines.

We think there is going to be a rush to extracting lithium from these old oil fields now that lithium is in such high demand.

Particularly in the USA.

Specifically by oil & gas super majors who want to get in on the battery metals rush, have huge balance sheets, and the technical abilities to extract and process liquids out of deep holes.

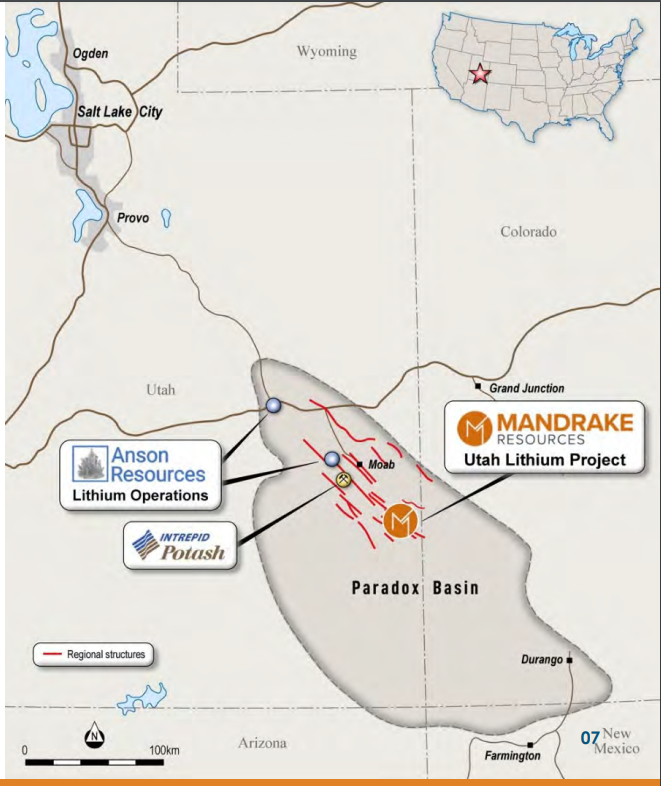

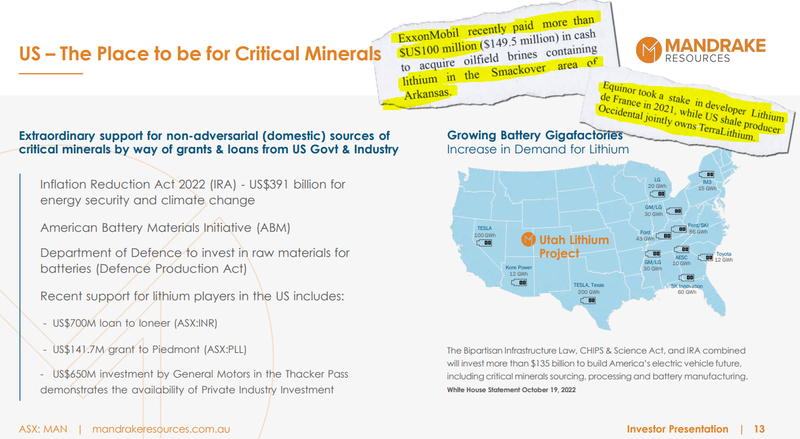

The United States hosts a number of oil fields with the potential for economically valuable lithium resources, including Utah’s Paradox Basin, and Arkansas’ Smackover Formation.

Extracting lithium from oil fields seems like the obvious path for big oil to enter the battery metals scene...

And it's already started. A few months ago, Exxon Mobil spent US$100M to acquire Galvanic Lithium in the Smackover Basin.

As always happens in oil & gas - it’s the small, nimble microcaps that have moved early and fast to pick up all the highest potential land.

Our Investment Mandrake Resources (ASX:MAN) has done just that.

MAN has spent the last 6 months acquiring 88,096 acres (356km2) of ground, which sits over enormous brine reservoirs in Utah’s Paradox basin.

There’s a bunch of old oil and gas wells on its ground too...

MAN already has access to re-enter 84 of these existing oil and gas wells to sample lithium brines.

This saves MAN millions of dollars in drilling and exploration costs, accelerating MAN’s pathway to a maiden JORC resource.

Plus it has 3D seismic, geological and petrophysical data in its hands.

MAN is capped at $28M, and held a relatively large $18.3M in cash in the bank at March 31st - which equates to MAN having a sub $10M enterprise value.

MAN’s project sits ~60km away from the more advanced $196M capped lithium developer Anson Resources.

Anson’s project has a JORC resource of ~1Mt lithium carbonate equivalent at 124 mg/L, with an additional aggregate exploration target of 2.1 Mt - 4.7 Mt LCE.

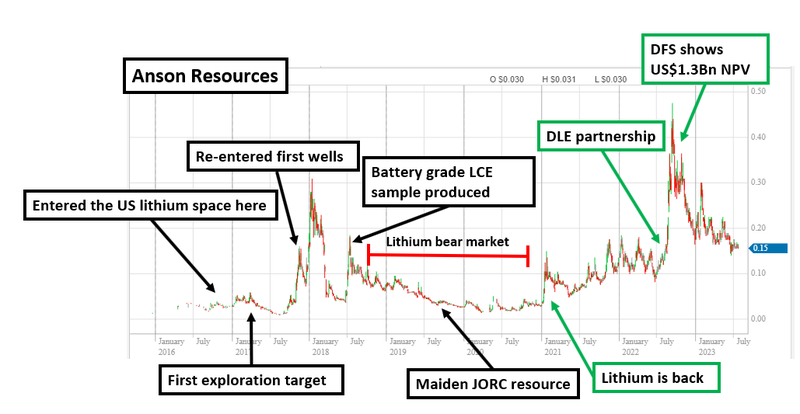

Anson, over the past ~6 years has gone from a market cap of just $1.8M to now trade at $196M.

To get there, Anson started by staking more and more ground, re-sampling existing historic oil and gas wells and then defining a maiden JORC resource.

In mid-2022 after the company announced a Direct Lithium Extraction (DLE) partnership and the results from its Definitive Feasibility Study (DFS) its market cap hit a peak of ~$490M.

MAN is looking to follow the same story arc as Anson - and hopefully growth in valuation.

Here is what MAN has done so far on its US lithium project, and what MAN is working toward:

- Increased the size of its project ✅ - MAN has already increased its ground position to 88,096 acres (~356km^2). For context, Anson’s project sits on 167km^2 of ground so MAN’s project area is actually bigger.

- Access to historic data ✅ - MAN has existing data from old oil and gas wells, geological data and 3D seismic data. Historic wells ~6km away from MAN’s project intercepted lithium grades of ~340mg/Li. For context, Anson’s JORC resource has a grade of ~127mg/Li.

- Access to old oil and gas wells ✅ - MAN recently signed a well access agreement and now has entry rights into 84 historic oil and gas wells at a fraction of the cost of drilling new wells. MAN has already picked out two high-priority wells to re-enter over the coming months.

- Sample the old wells for lithium 🔄 - MAN plans to re-enter two wells to sample for lithium instead of oil and gas.

- Maiden JORC resource 🔲 - hopefully, the sampling delivers good results and MAN is able to define its own maiden JORC resource estimate.

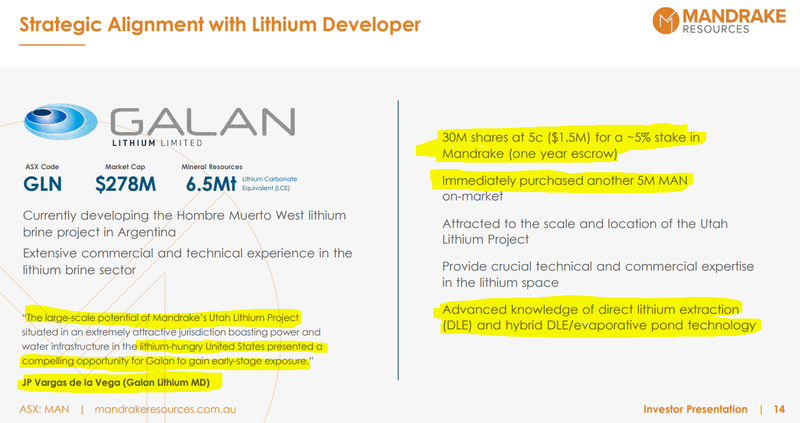

MAN has already managed to attract a $1.5M direct investment at 5c from $264M capped Galan Lithium - Galan now owns 6.4% of MAN.

We are hoping that after MAN has a JORC resource of its own, the market will be able to compare its project with its neighbour Anson Resources.

As long as MAN can:

- Deliver a resource of size/scale comparable to Anson and then,

- Sign some kind of partnership with a Direct Lithium Extraction (DLE) technology company for development...

Then we think the company could deliver on our Big Bet, which is as follows:

Our Man Big Bet:

“MAN returns 1,000%+ by making a lithium discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our MAN Investment Memo.

For a high level update on MAN’s progress, check out our Progress Tracker for MAN:

How MAN is following the Anson Resource playbook

Anson first entered the US lithium space back in September 2016.

Over the next few years Anson kept increasing its landholding in Utah mostly by staking additional ground.

By mid-2017, Anson had put together its first brine exploration target. In January 2018, Anson started re-entering its first well and had assay results by March.

By July 2018, Anson had produced its first sample of battery-grade lithium carbonate equivalent product from its pilot plant.

Anson’s maiden JORC resource came out into the market in June 2019.

Through the lithium bear market, Anson’s focus was on increasing the size/scale of the resource and putting the project through feasibility studies.

Now the project has a DFS with a net present value of US$1.3BN and Anson has managed to lock in a deal with Direct Lithium Extraction (DLE) technology developer Sunresin.

Both the DLE partnership and the DFS put its project into a position where it is ready to develop.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Where is MAN relative to Anson?

MAN is preparing for re-entry into its first two wells.

We are hoping that if MAN can produce some strong lithium sampling results it can put together a JORC exploration target and a maiden JORC resource.

A JORC resource will mean MAN’s project can be compared with other US lithium brine projects in terms of size/scale and grade.

🎓 To learn more about the importance of JORC resources read: What is a JORC resource? How does a company define a resource?

The re-rate cycles of MAN peer Anson

Anson’s share price went through two periods of re-rates.

The first came in the initial market rush into lithium back in 2017-2018.

Anson at the time re-entered its wells, announced an exploration target, produced battery grade lithium carbonate equivalents and put together a maiden JORC resource estimate.

The next ~2-3 years was the lithium bear market and despite the company making progress with its project, the share price stayed near all time lows.

Then in 2021 as the lithium market improved Anson’s share price started rising again.

The peak however was in mid-2022 after the company announced a Direct Lithium Extraction (DLE) partnership and the results from its phase one Definitive Feasibility Study (DFS).

At its peak, Anson was capped at ~$490M.

Ultimately we think MAN’s share price could react in a similar way -

- First re-rate higher off the back of project-level news - as MAN delivers an exploration target, maiden resource estimate and some processing newsflow.

- Second re-rate higher off commercialisation news - as MAN delivers progress on a DLE partnership and project funding.

With MAN trading at an enterprise value of sub-$10M, we think the company has plenty of room and newsflow to re-rate to a higher valuation.

The added bonus is that MAN has the funding already in place to make it all happen over the near-mid term, with ~$18M in cash at 31 March 2023.

We will get a more accurate idea of MAN’s cash balance in the next few days as the June quarterly is released.

Oil and gas supermajors buying into US lithium brine projects

As we noted above, MAN has moved early in the Paradox Basin, and we have evidence already of oil and gas supermajors entering the US lithium brine space.

(Source)

In May, Exxon entered the US lithium industry paying US$100M for Galvanic Lithium’s project in the Smackover Basin, Arkansas.

This follows moves by French oil and gas major $137BN Equinor, which took a stake in Lithium De France and US shale producer $82BN Occidental Petroleum which has a stake in TerraLithium.

Initially the move by Exxon looked unusual for a company that is one of the biggest oil and gas producers in the world BUT we think it all makes sense strategically.

The oil and gas space is relatively mature.

The transition to electric vehicles and electrification of economies around the world is threatening to reduce demand for oil and gas in the long run.

In the short term this has put new oil and gas projects on hold meaning outsized cash returns for projects that are already in production.

The oil and gas majors now find themselves in a position where existing projects are generating heaps of cash BUT new mega projects are on hold.

This means the oil and gas majors need to find alternative places to invest their cash warchests.

Lithium is a natural fit given its importance in the energy / battery supply chain.

The move to lithium brine makes even more sense given oil and gas majors have for decades been developing technical expertise in pumping liquids to surface from underground reservoirs and then processing them into commercial products.

The key technical risk for lithium brine projects at the moment is extracting and then processing the brines into battery grade lithium carbonate.

We think, if anyone is going to find a way to commercialise processing technologies in the brine space it is highly likely to come from the oil and gas industry.

We think, the move from oil and gas majors into the lithium brine space makes sense both from a commodity perspective and a technical capabilities perspective.

In the long run we expect to see more of the majors enter the space and hopefully this flows through into higher valuations for projects like MAN’s.

What’s next for MAN?

In the short term, we want to see MAN complete the permitting for its two-well re-entry program.

After the re-entry is completed we will get a better idea of the size/scale of MAN’s project.

We are also keeping one eye on MAN finding a potential DLE technology partner, but understand that the company’s key priority is to deliver a maiden JORC resource.

What are the risks?

The two key risks we see for MAN in the short term are “Exploration risk” and “Processing risk”.

Exploration risk is relevant because there is always a chance the company finds uneconomic quantities of lithium in the wells it re-enters.

Processing risk is also a factor because, even if MAN does find a decent amount of lithium, there is no guarantee that any of that lithium can be extracted and processed at rates that make MAN’s project commercially viable.

To see all of the key risks to our MAN Investment Thesis, check out our MAN Investment Memo here or by clicking on the image below:

Our MAN Investment Memo:

Along with the key risks, our MAN Investment Memo provides a short, high-level summary of our reasons for Investing.

The Investment Memo details:

- Key objectives we want to see MAN achieve

- Why we Invested in MAN

- What are the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.