Growth Portfolio: Beach Energy Ltd (ASX: BPT)

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

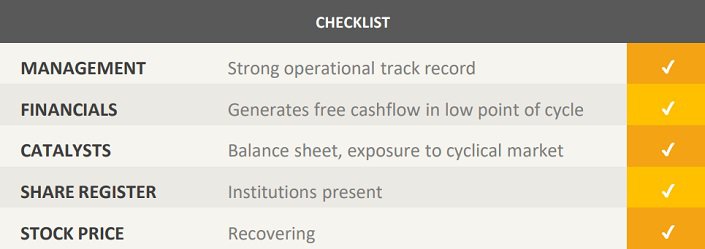

Overview: Beach Energy Group ("Beach Energy", "the Company"), is an Australian oil and gas company focused on the Cooper/Eromanga basin. During FY16 Beach Energy produced 9.7M barrels of oil equivalent, with 53% being oil and 47% gas and gas liquids. The Company recently completed the merger with Drillsearch Energy Limited, which is now operating as a fully owned subsidiary of Beach Energy, and divested assets in Egypt and Queensland.

Catalysts: Beach Energy is highly leveraged to any recovery in the oil price generating an additional $50m NPAT if oil prices increase by US$10 per barrel. The Company successfully identified operational cost savings, reducing the cash flow break-even point to $26 per barrel. Beach has a strong balance sheet with 243 million in cash and undrawn debt facilities of $350m. The merger with Drillsearch may result in further synergies and could be a value driver.

Hurdles: Global benchmark oil prices have significantly declined since 2014 and there is no guarantee that prices won’t fall further. Beach Energy posted a statutory loss during FY16, which may affect the company’s ability to pay dividends in the future. There are integration risks associated with the Drillsearch merger.

Investment View: Beach Energy offers transitional exposure to the domestic oil and gas market. The Company has a strong balance sheet with surplus cash and access to additional capital. Generating free cash flow at the lower end of the commodity cycle, Beach Energy is well-positioned to benefit from any cyclical recovery in the oil and gas market which may allow for higher dividend distributions. However, commodity price volatility, lumpy earnings, and integration risks are primary hurdles. Beach Energy is sensitive to price movements but we believe the valuation is compelling and the risk to reward ratio favourable. We initiate coverage with a ‘buy’ recommendation.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.