88E Drilling to Target 645M Barrels on North Slope

88 Energy (ASX:88E | AIM: 88E) is a junior oil explorer seeking to discover the next multi-billion barrel oil resource on the North Slope of Alaska, one of the world’s great oil Super Basins.

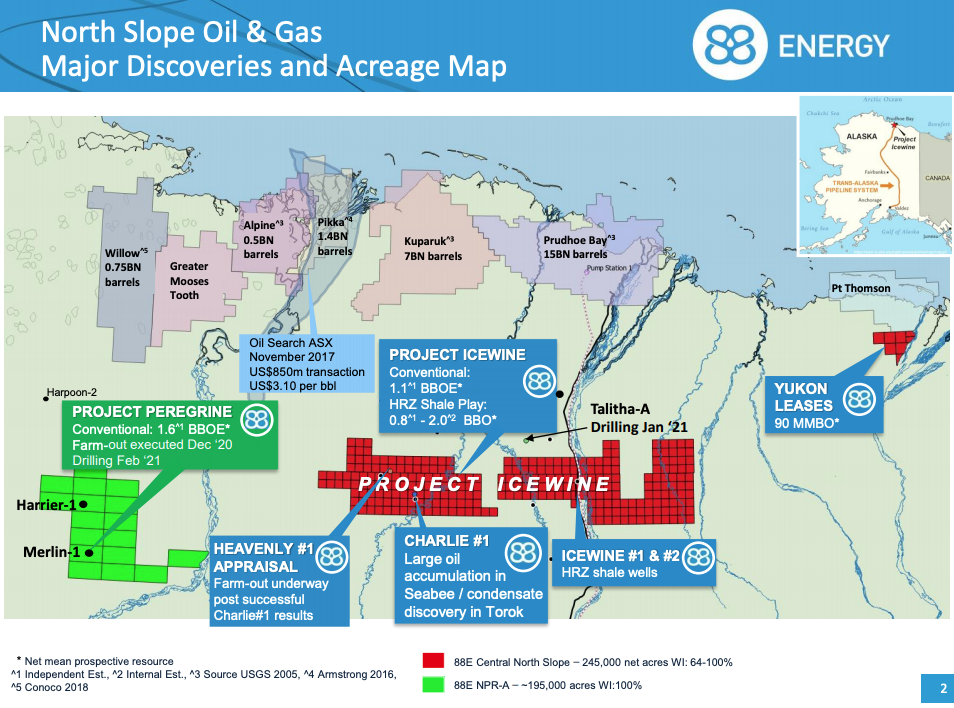

The company is the operator across several exploration/appraisal projects totalling approximately 440,000 net acres on the Slope, with a number of extremely large drill targets that have the potential to unlock significant value on discovery.

88E’s Project Peregrine has an independently assessed 1.6 billion barrels of oil equivalent (gross mean prospective resource), with three prospects that are located on-trend to recent discoveries.

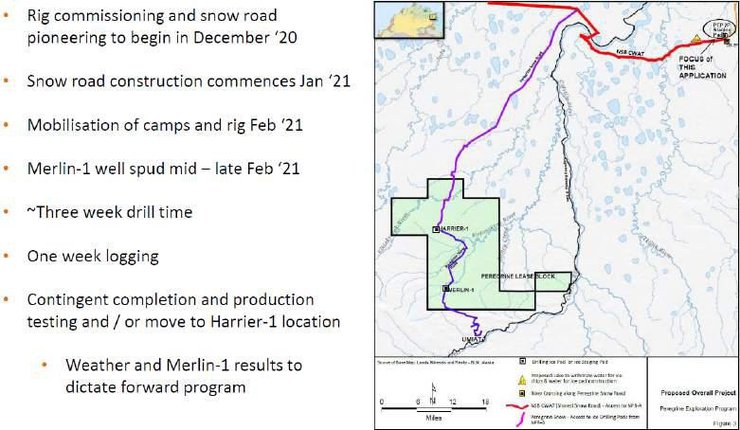

Drilling is planned for February 2021, following a recent farm-out which will see Alaska Peregrine Development Company (APDC) taking on the majority of costs in drilling the upcoming Merlin-1 well. The Merin-1 well is targeting a gross mean unrisked prospective resource of 645 million barrels.

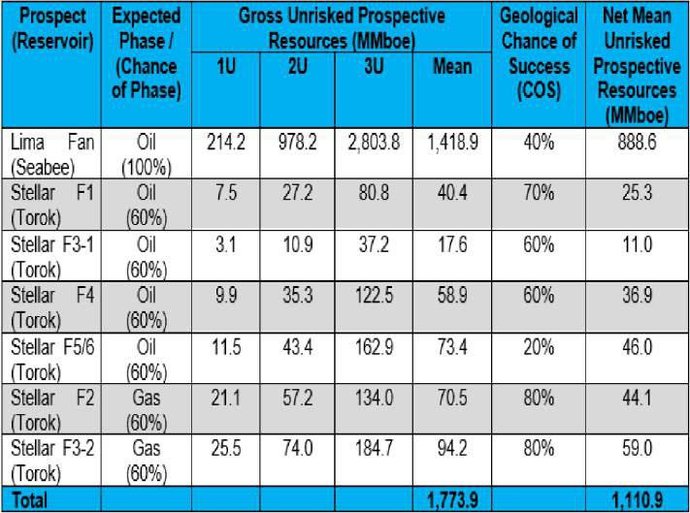

Project Icewine is another highly prospective asset, with a recent independent resource estimate outlining a total resource of 1.77 billion barrels of oil equivalent with a net mean unrisked prospective resource of 1.11 billion boe attributable to 88E. 88E is also in negotiations to farm-out its Yukon leases (approximately 90 million barrels mean prospective oil resource).

While the company has multiple North Slope assets, Project Peregrine is the current exploration focus and indeed provides the most likely near-term share price catalyst, particularly if Merlin-1 is successful.

Asset Overview

Three onshore prospects have been identified at Project Peregrine – Merlin (Nanushuk formation), Harrier (Nanushuk), Harrier Deep (Torok), with a combined mean unrisked recoverable prospective resource of 1.6 billion barrels of oil located on-trend to recent discoveries.

ConocoPhillips’ (NYSE: COP) 750 million barrel Willow discovery is located to the north, and Umiat, a recent Brookian oil discovery with over a billion barrels of oil, is to the south.

The spud of the first well at Project Peregrine, Merlin-1, is on track for late February 2021 with the company now undertaking permitting, planning, and contracting works associated with the drilling.

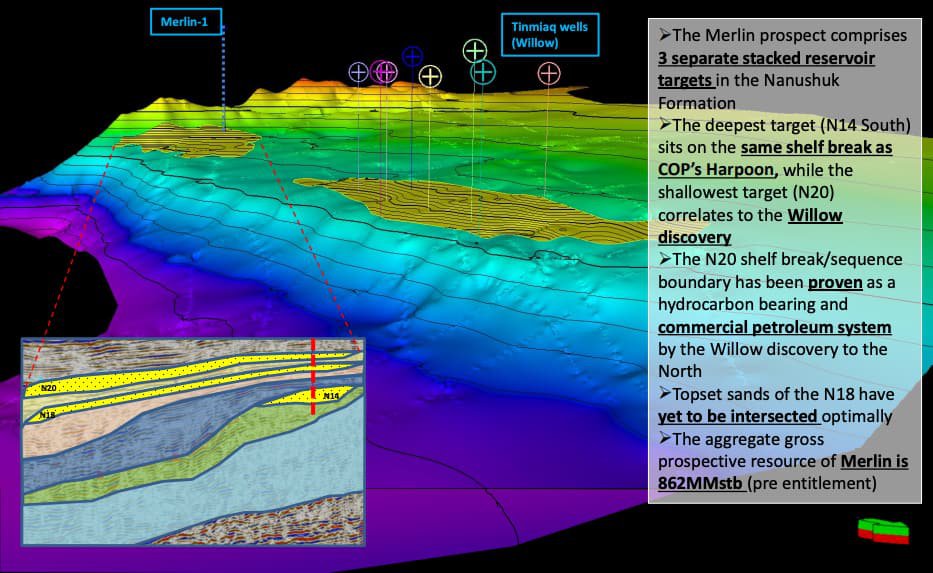

The Merlin-1 well will aim to intersect 3 separate stacked reservoir targets in the Nanushuk Formation. The deepest target sits on the same shelf break as COP’s Haroon, while the shallowest target correlates to the Willow discovery.

In assessing the prospects at Project Icewine, the Seabee reservoir alone could be a company maker as it has a gross mean recoverable prospective resource of 1.4 billion barrels of oil.

Further, Torok has a gross mean recoverable prospective resource of 355 million barrels of oil equivalent, consisting of condensate gas and light oil.

Merlin-1’s target depth is 6,000 ft, a relatively shallow well. The estimated gross well cost is US$12.6M, with APDC contributing US$11.3M to earn 50% of Project Peregrine. 88E is to contribute US$1.3M, representing its 50% share over and above the APDC carry. All additional costs above the US$10M carry will be borne equally by APDC and 88E.

Further, Torok has a gross mean recoverable prospective resource of 355 million barrels of oil equivalent, consisting of condensate gas and light oil.

Positive results from the Charlie-1 well drilled earlier this year have prompted management to immediately commence farm-out proceedings with a view to drilling in the first half of 2022, at a new location following extensive data interpretation.

The estimated quantities of petroleum that may potentially be recovered by the application of a future development project relate to undiscovered accumulations. Consequently, these estimates have both an associated risk of discovery and a risk of development, but the geological chances of success (COS – ‘chance of success’ as determined by an independent organisation) are extremely high relative to many projects that are at this stage.

While the huge Seabee (Lima Fan) resource has a significantly lower COS than some of the other prospects, 40% is still relatively high for early-stage exploration.

Further, to have four prospects (Stellar F1, F3-1, F2, and F3-2) with COS between 60% and 80% is highly encouraging, particularly when one takes into account that these account for a cumulative net mean unrisked prospective resource of 176 million barrels of oil equivalent.

Investment View

Whilst it is notoriously difficult to arrive at a fair valuation for a pre-revenue oil explorer, it is the overall size of the prize at Project Icewine as indicated in the table above, along with the substantial Project Peregrine prospects that support a valuation well above the company’s current enterprise value of approximately A$66 million.

As the drilling of Merlin-1 draws closer, we would expect increased investor interest, driven by speculation in the potential for a company making oil discovery. Beyond that, news of a farm-out at Project Icewine would also mark a major catalyst.

It is worth examining some of the key developments that have occurred over the last 12 months or so that have weighed on the company’s share price, as well as those that have captured the interest of investors.

The key positive share price catalyst that emerged in 2019 was the positive Charlie-1 appraisal well update (October) which resulted in the company’s shares doubling in the December 2019 quarter.

Remember, the fundamentals that drove this rerating are still in place.

The sell-off that occurred in the first half of 2020 coincided with news regarding COVID precautions, the somewhat protracted acquisition of XCD Energy, and the inability of the oil price to stage any meaningful and consistent recovery, something that has only occurred in the last month or so.

Investors have an extreme dislike for uncertainty, preferring to take their money off the table altogether until they can get an accurate read on industry conditions and/or a company’s performance.

It is fair to say that 88E was dogged by external issues rather than its performance and on this basis, its share price could be viewed as a highly beneficial entry point given that COVID concerns are not impacting the company in that region, the acquisition has been completed and the S&P/ASX 200 Energy Index (XEJ) is reflecting a return to energy stocks, having gained more than 2000 points or 35% in the last five weeks.

In November, 88E raised A$10 million (£5.5M), at A$0.006 or 0.33p per share to fund the ongoing exploration activities and to identify and exploit new opportunities on the North Slope of Alaska.

There was strong demand for the stock, suggesting that the market is looking favourably on what 88E is planning to do over the coming months.

These funds, along with drilling cost contributions from APDC have given the company sufficient capital to fund well costs above the anticipated farm-out/carry, and having some more cash allows the company to potentially look at new venture opportunities.

Along with the company’s existing cash balance ($17.2 million at December 10, 2020), this should be more than enough to cover any expenses until the farm-out is complete, at which time the farm-out partner will cover the majority of expenses involved with the drilling.

It appears obvious that investors see 88E as extremely undervalued – sizeable capital raisings often have a negative impact on share prices, but in the case of 88E its shares have rallied strongly since the placement and they are now trading at a premium of about 40% to the placement price.

Analysts are also upbeat about 88E’s prospects, and UK stockbroker Cenkos recently reaffirmed its ‘Buy’ recommendation, attributing a price target of 2.8p (~5.9¢) to the stock, implying an upside of some 600% to the current price.

We believe the metrics applied by Cenkos in arriving at its price target have merit, and with other catalysts, on the horizon, the company may push up towards these levels as early as 2021.

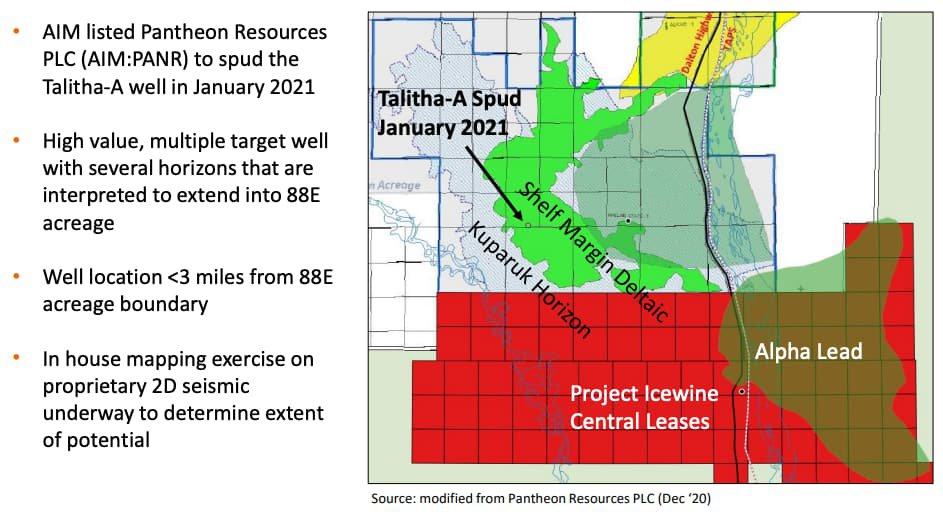

On the score of catalysts, there could be some positive news from the $380 million Pantheon Resources (AIM: PANR) prior to the drilling of Merlin-1.

Pantheon’s Talitha-A well, located close to the northern border of the 88E central acreage position at Project Icewine, is scheduled to spud in January 2021, and several of the prospective horizons in Talitha-A are interpreted to extend into 88E acreage as indicated below.

With the drilling of Talitha-A well occurring ahead of the Merlin-1 spud, 88 Energy’s share price could receive some support even before drilling results start to filter through if Pantheon has success.

Success at Talitha-A would also likely impact farm-out negotiations in 88E’s favour.

As Pantheon recently highlighted, Alaska North Slope is home to the US’s largest two oil fields and it hosts some of the world’s largest discoveries over recent years, featuring both onshore and conventional (not shale) with enormous potential.

With excellent infrastructure and low royalty rates supporting the oil industry, it is a good place to do business for the companies exploring the Slope.

Outlook

Having established that 88 Energy has a diversified range of premium assets in one of the world’s best locations there aren’t too many other factors to be addressed other than management’s ability to successfully commercialise one or some of those prospects.

The timing is definitely right with some big acquisitions being made in the region, the oil price recovering and 88 Energy ripe for the picking based on its current share price.

Consequently, it comes down to strategy, and in 88 Energy’s case that requires some degree of explanation as it isn’t a one size fits all approach.

While we have provided some insight into management’s goals in terms of exploration, the following is a wrap of how things should play out over the next 12 months or so.

At Project Peregrine, most of the boxes have been ticked ahead of drilling with the farm-out ratified and the rig contract executed.

Within three months the aggressive pursuit of a multi-well strategy will aim to validate the prospective resource of more than 1 billion barrels across two targets, being Harrier and Merlin.

In terms of progressing Project Icewine, the focus will be on executing a farm-out based on the Charlie-1 condensate discovery in Torok Fm and the oil pay interpreted in Seabee Fm.

The company’s prospects of establishing an attractive farm-out agreement have been enhanced by the validated independent resource upgrade to 1.77 billion barrels of oil equivalent.

Providing further attraction to a potential farm-in partner are the excellent oil saturations measured in the core from Charlie-1 in Seabee and Torok Fm.

The low-cost acquisition of an existing oil discovery (circa 90 million barrels of mean prospective oil resource) close to infrastructure at 88 Energy’s Yukon leases provides the company with a number of options, particularly given the encouraging nature of the recently acquired 3D seismic information.

Management is undertaking negotiations with other resource owners regarding an aggregation strategy, which could be followed by a farm-out as 88E currently has 100% ownership.

The company’s concerted focus on Project Icewine’s of the HRZ unconventional liquids-rich resource in 2018 has taken a back seat for the moment, but results from Charlie-1 analysis of HRZ are expected to facilitate a farm-out process.

Based on Icewine-2 flowback data including information relating to core and logs, management and the joint venture partners adopted the stance in 2018-19 that the HRZ was comparable to other early stages commercial unconventional plays.

Consequently, Icewine HRZ remains a work in progress.

THE BULLS SAY

- There has been no better entry point in the last five years for investors who fancy picking the bottom. The last time 88E traded around these levels was in January 2016, and in the ensuing three months the company’s shares increased 1,200%.

- 88E’s assets are situated in a prime location in terms of regulatory support and the prospective nature of the ground, highlighted by the presence of oil supermajors such as ConocoPhillips.

- The recent growth in prospective resources will continue to work in the company’s favour in terms of valuations attributed to the stock, as well as making it easier to attract quality farm-in partners.

- The company’s diversified portfolio shows early signs of exploration success, and this sees it well-positioned to deliver a ‘company maker, or on the other hand progress with an aggregation strategy that could see it continue to partner with high profile groups attracted to its suite of assets.

- Most of 88E’s targets can be drilled quickly and cheaply with farm-out partners, placing little strain on the company’s cash flow

THE BEARS SAY

- Despite the fairly advanced stage of a number of its exploration assets, particularly in terms of having established resources, there is no guarantee that 88E will uncover a commercially viable project.

- As a company with a sub-$100 million market capitalisation funding is also an issue, and it is likely that a project requiring significant upfront capital expenditure would require a sizeable farm-in transaction and/or debit and equity funding.

- While the oil price has recovered from extremely depressed March levels, it still has some way to go in terms of returning to long-term median levels.

General Information Only

This material has been prepared by Jason Price. Jason Price is an authorised representative (AR 000296877) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573) (62C), and a Director of S3 Consortium Pty Ltd (trading as StocksDigital).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, Jason Price, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, Jason Price, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.