US market swings drove a wild week on the ASX.

Published 30-APR-2022 09:14 A.M.

|

16 minute read

Big swings in the US market drove a wild week of ups and downs on the ASX.

The small cap market (including our Portfolio stocks) came along for the ride on broader market sentiment alone.

Big US technology stocks on the NASDAQ, like investor darlings Facebook, Amazon, Apple, Netflix and Google are known for minting many millionaires and billionaires.

But they have each taken a severe beating over the last few months in this period of high inflation and the world’s emergence from COVID.

Many of these market darling growth stocks have had a horror run from their recent peaks, some familiar names include:

Zoom (-82%), Netflix (-71%), Peloton (-89%), Facebook (-46%), Shopify (-74%), Square, (-63%) and Spotify (-71%).

These are multi-billion dollar stocks with huge revenues, but these share price drops are the kind you expect to see when an ASX small cap delivers a bad drill result.

That said, anyone who invested in these US tech stocks years ago — back when they were small caps — would still have done extremely well.

Tech has had a huge run over the last decade but we think now is the decade for commodities to shine.

We believe a commodities super cycle will be driven by a high inflation environment combined with the world’s need for “new critical material” supplies to move to low carbon energy and batteries.

The geopolitical uncertainty from the Ukraine war is only exacerbating the situation by ruling out traditional suppliers, further driving up commodity prices, and pushing investment to new exploration in friendly countries.

Hopefully one of our early stage Investments will experience even a fraction of the growth seen by some of the big US tech companies over the last 10 years.

That is what we are Investing for, and we have a few bets placed in our Portfolio to get there.

We have been calling a new commodities super cycle for a while now and have positioned our small cap Portfolio accordingly.

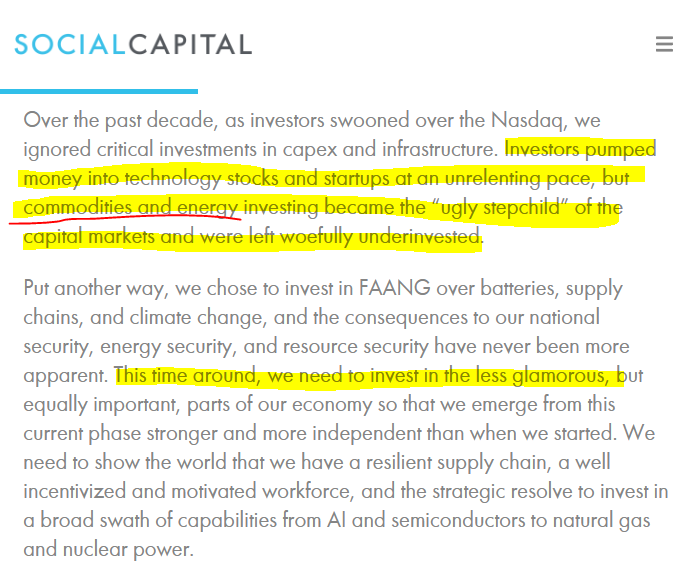

Famous investor Chamath Palihapitiya, who made his billions riding the US technology wave, echoed this sentiment in his annual letter this week:

It’s encouraging to hear one of the most well-known investors in the world acknowledging the need for more investment in energy and commodities, which we think is a leading indicator that other large, global fund managers will follow.

So we are pleased that our small cap Portfolio is currently overweight in early stage commodities exploration, focused on critical materials.

Another way we see that early stage small cap companies will weather a high inflation environment is that if one DOES hit that elusive “huge exploration result”, the market should re-rate it accordingly, regardless of broader market conditions.

Quarterly inflation figures came in from the RBA this week. (Boring, we know, but please keep reading).

The annual inflation rate of 5.1% is the largest increase recorded since 2001 due to higher fuel prices, a result of Russia’s invasion of Ukraine, and increased dwelling construction costs due to supply chain issues.

To get to the point — what does that mean for our Investments and small cap stocks in general in a high inflation environment?

With inflation at its highest level since the Lord of The Rings came out and the threat of higher interest rates looming on the other side of this weekend, plus all the associated doom in the news — some may be wondering whether it’s a good time to be invested in stocks, and importantly, in small caps?

Let’s preface this by saying that (in our view) it is almost always a good time to be invested in small caps (as a small part of a broader portfolio). And no, it’s NOT always a good time to be in just any small cap.

But since that’s the slice of the market that we operate in, we’ll keep doing what we do – Investing in promising early-stage companies backed by quality management — inflationary environment or not. Recession or not. Market crash or not.

That’s the beauty of investing in early-stage companies. While their operating costs may rise with rising inflation, or the cost of debt increases with higher rates, the chance for a big pay day still exists.

This compares to investing in big blue chips, which is playing at the margins — revenues just missing expectations or a slight dip in forecast sales, for example, can massively shift the market’s perception ... and the company’s share price.

But when it comes to small caps, we’re not playing for marginal wins; we’re playing for the 1,000% plus wins (And we’re aware of the risk of the flipside — a 100% loss.)

The market will still react to major catalysts and recognise the big wins, such as an impressive contract signing or an exceptional drill result and will typically react appropriately — regardless of whether the wider market and every sector in it is in the red.

Small caps have a way of defying the larger market and the noise that affects it.

...as long as investors can be patient and not get too worried about share price fluctuations while waiting for that coveted (but rare) successful result that delivers a positive share price catalyst.

...and of course on the assumption that the particular small cap sits within a rising global macro theme - like a commodities super cycle.

To read our commentary on “what is a share price catalyst” and see our list of upcoming potential share price catalysts for EVERY company held in our Portfolios — Next Investors, Wise-Owl, Catalyst Hunter and Finfeed — check out last weekend’s email, sent on ANZAC Day –What exactly is a share price catalyst?, as republished here.

Here are expected near term news announcements we hope might deliver potential catalysts that could move share prices higher ASSUMING a very positive result — despite any issues that are affecting the broader market, including inflation.

Potential near term share price catalysts:

- The Sasanof companies (PRM & GLV) high impact gas drilling event: one of the biggest oil and gas wells drilled in Australia by an ASX junior in decades (memo)

- GGE drilling its maiden Helium well in Utah where it’s aiming to make a commercial Helium discovery (memo)

- LCL drilling results from its large central gold target (we named it “Jabba the blob”) to significantly expand its multi-million ounce known deposit (memo)

- PRL signing a Joint Development Agreement with its partner, Total Eren to materially derisk its WA Green Hydrogen Project (memo)

- IVZ about to drill its giant gas prospect in Zimbabwe - we have been waiting 2 years for this event (memo)

- KNI about to drill its cobalt targets in Norway (memo)

- BPM about to drill its lead zinc prospect in the Earaheedy basin close to Rumble Resources recent discovery (memo)

- FNT commencing drilling for rare earths (memo)

- GAL nickel and palladium drilling results (memo)

That’s not to say that small cap share prices don’t swing up and down with the market day to day. But those moves don’t concern us.

The reason we Invest in these small — or micro-cap — companies is for the chance of 1,000% plus gains while holding a long term position (and ofcourse Free Carrying along the way to de-risk the position).

We know that not all of our Investments will pay off, but in our experience, if those that strike gold (so to say) can outweigh the poor performers, they will lift the entire Portfolio.

HOWEVER, remember that just because the success or failure of these early-stage companies may not be as closely tied to macro-economic events as are bigger companies, it does not mean they are less risky.

Quite the opposite, in fact.

We remind you that investing in early-stage companies is a high-risk endevour — only invest what you can stomach to lose... but who knows, maybe one or two investments will pay off.

At the start of the 10 year US tech boom, many household tech names were just high-risk tech start-ups with founders trying to raise money from investors in Silicon Valley.

While Silicon Valley was the place to be back then for tech, we are hoping that the next 10 years will see some big commodities success stories coming out of traditional commodity regions like Australia, Canada, South America and Africa.

Hopefully one of them is in our Portfolio.

📰 This week on Next Investors

Oneview’s Latest Quarterly Shows 3x Increase in RFPs/RFIs

Our healthtech investment, Oneview Healthcare (ASX:ONE) closed out the week with the announcement of its March quarterly report, which showed a possible future demand surge for its products brought on by the pandemic.

We were particularly interested in the commentary by ONE with respect to its sales pipeline and potential growth trajectory after its recent $20M capital raise. The following were the key takeaways for us:

- The big one for us - 8,630 beds worth of RFIs/RFPs (sales pipeline)

- Cash balance of €11.8M

- Net operating cash outflow of €3.3M ($4.8M)

- OEM (Original Equipment Manufacturer) hardware up-front payments of €1.2M ($1.77M)

- Revenue of €1.6M ($2.37M) vs €2.8M ($4.14M) vs last quarter (down 45%)

The key point for us being the RFI’s/RFP’s - ONE’s sales pipeline.

Requests for Information (RFIs) and Requests for Proposal (RFPs) are formal processes for evaluating ONE’s tech for implementation in a hospital and an important part of ONE’s sales pipeline.

This is in addition to the direct to customer sales which ONE confirmed it is actively progressing. .

The 8,630 beds in the sales pipeline now signals a minimum ~3x growth in customer interest for ONE’s products as represented by RFP/RFI numbers vs last quarter.

📰 Read the full breakdown: Oneview’s Latest Quarterly Shows 3x Increase in RFPs/RFIs

The IVZ Bidding War Has Officially Begun - Drilling in July

On Wednesday our 2020 Energy Pick of the Year, Invictus Energy (ASX:IVZ) confirmed that well-pad construction had commenced ahead of its drilling program that’s now scheduled for July.

IVZ also confirmed that it has now received THREE competing farm-in offers for the upcoming drilling program.

The offers include an updated and improved offer from the current non binding farm-in partner, Cluff Energy Africa. Ongoing due diligence and internal approvals are also being undertaken by additional interested parties.

Those who have been following our coverage of IVZ will know that when we first covered the farm-in agreement with Cluff Energy Africa in December last year, we said it could prove to be like the “first bid at an auction”.

Our thinking was that as IVZ completed the 2D seismic data processing, generated additional drilling prospects and leads, the attractiveness of the project to farm-in partners would increase.

Since then IVZ have had two major developments at the project level which we think is leading to this increased interest in the project, the two developments are as follows:

- 2D seismic data processed: Results confirm extensive seismic anomalies at multiple levels for the Mukuyu prospect, the identification of a substantial new shallow target measuring ~15km x 16km identified and more prospects and leads along the basin margin.

- 7x increase in project size: The project size has increased ~7x, from 100,000 ha to 790,300 ha, following the signing of a Heads of Agreement with Zimbabwe’s Sovereign Wealth Fund.

📰 Read the full breakdown: The IVZ Bidding War Has Officially Begun - Drilling in July

DXB Actively Recruiting Patients Across the Globe, First Dosing Soon

This week our 2021 Biotech Pick of the Year, Dimerix (ASX:DXB), has released its March quarterly report which showed solid progress towards proving its treatment for a rare kidney disease (FSGS) is both safe and effective.

Generally quarterly reports are more a summary of what happened for a three month period, but with respect to DXB we noticed the following new developments:

- For 11 of the 12 countries planned for trials, DXB has received ethics and/or regulatory approval to conduct the FSGS study, with USA approval pending.

- Dr Ash Soman appointed as Chief Medical Officer.

- A new DMX-200 patent application submitted globally, adding patent protection through to 2041, if granted.

- Net operating cash flow for the March quarter was $500K, after a $3.7M R&D tax incentive rebate and the Australian government’s BTB program’s $300K grant

- DXB had a cash balance of $16.8M as at the 31st of March.

At the time of our note, DXB was trading at a market cap of $46.5M and with the $16.8M in cash in the bank, had an Enterprise Value of just ~$30M.

With the trial having started in October 2021, DXB anticipates the first interim data to be ready by H1-2023. We expect the company to receive more interest as this date gets closer.

📰 Read the full breakdown: DXB Actively Recruiting Patients Across the Globe, First Dosing Soon

In our other portfolios 🧬 🦉 🏹

🦉 Wise-Owl

FOD is Finally Cash Flow Positive – Now for the Growth Phase

On Friday our Beverage manufacturing Investment, The Food Revolution Group (ASX:FOD) put out its March quarterly report which showed that the company had reached a major milestone becoming ‘cash flow positive’ — a strong signal that the company is successfully implementing its turnaround plans.

We first invested in FOD just over a year ago, in March 2021, and this is the first cash flow positive quarter since. At the time, we had the view that FOD was “an emerging turnaround story”. Its flagship brand, Black Label Orange Juice Co. was steadily gaining market share and we liked the growth potential on offer.

Since then, FOD has made strategic changes to its sales mix including the release of three new products, reduced costs via improved efficiencies, and improved its strategy around raw materials procurement.

FOD is on a Fix ✅→ Reset✅ → Growth trajectory 🔄.

Early signs of FOD’s transition from the ‘Reset’ phase to the ‘Growth’ phase is that it is now operating cash flow positive. We expect to see overall market interest in FOD increase as the company starts to display this with a noticeable improvement in business performance.

📰 Read the full breakdown: FOD is Finally Cash Flow Positive – Now for the Growth Phase

🏹 Catalyst Hunter

Chargeability anomalies over High Grade Rock Chips - There’s only one thing left to do

On Friday, our exploration investment TechGen Metals (ASX:TG1) put out an announcement detailing some interesting copper/gold drilling targets at its Ashburton Basin project in WA.

TG1 confirmed that after running geophysical surveys over its Station Creek Copper Project, the company identified two high priority IP chargeability anomalies in the same spot where high-grade copper rock chip samples were picked up previously.

The two high priority anomalies were detailed as follows:

- The first anomaly (TA1) measures 500m x 100m and is located only 150m away from high-grade copper and silver rock chip samples that returned a peak results of 54.8% copper & 249g/t silver.

- The second anomaly (TA2) is also sitting right on top of a previous rock chip sample that returned peak grades of 7.32% copper.

The significance of this is that the data from these geophysical surveys is now marrying up with the results from the geochemical sampling programs the company ran previously.

With early stage exploration projects like these, we don’t often see both geophysical AND geochemical work pointing to the same target areas. In the case of TG1, those rock chips are sitting right on top of the geophysical targets.

One of the key reasons we continue to hold TG1 in our portfolio is because of its tiny market cap of $6.8M and enterprise value of only $4.2M. With these new drilling targets now being firmed up for drilling later in the year we think TG1’s share price is leveraged to a re-rate off the back of a new discovery.

We also launched our 2022 TG1 Investment Memo off the back of this news. To see all of the key reasons why we continue to hold TG1 in our portfolio, what we want to see the company achieve in 2022 and the key risks to our investment thesis, check out our memo here.

📰 Read the full breakdown: Chargeability anomalies over High Grade Rock Chips - There’s only one thing left to do

GGE’s Maiden Helium Drilling Event has Begun - Here’s what we are looking for next

On Tuesday, our 2021 Catalyst Hunter Pick of the Year, Grand Gulf Energy (ASX:GGE) confirmed that drilling at its maiden helium exploration well had commenced.

Spudding of the well occurred on Sunday 24 April at 5:30PM local time. GGE fortuitously timed its drilling program to coincide with surging helium prices. Helium is now selling for as high as US$2,000-3,000 mcf. Not long ago it was priced around $350-600 mcf.

Now that GGE’s maiden helium well has been spudded, it's time to take a look at what to expect over the coming weeks from GGE:

- Drilling is expected to take ~30 days to reach the total depth of ~8,500 feet.

- We hope to see some initial results less than one week after the drilling is completed.

- We expect detailed results, including any flow testing to take another 2-3 weeks after this.

- Offtake partner already secured, so GGE already has a buyer of any helium it finds.

We used our note to re-establish our expectations for what we want to see from the Jesse #1 drilling results:

- Our base case target is for GGE to prove there is a helium system present at the project. If GGE intercepts a helium structure, it can be followed up with additional drilling programs.

- An exceptional result for us would be if GGE returns >0.4% helium concentration in the raw gas stream at a flow rate of 10mmcfpd of raw gas. In our opinion, this would constitute a commercial discovery and could immediately be tied into the offtake partners processing facility, moving GGE from explorer to producer.

Effectively, if GGE identifies a working helium structure with this drilling program, the company would meet our base case expectations.

If GGE then completed flow rate testing and returned the results we set above of >0.4%, we think GGE could move from explorer to producer off the back of Jesse #1 alone.

🎓 = To learn more about how we go about setting our expectations for drilling events check out our educational article here.

📰 Read the full breakdown: FOD is Finally Cash Flow Positive – Now for the Growth Phase

🗣️ Quick Takes

NEW: We are now releasing our Quick Take opinions as they happen so you don't have to wait until the weekend to see them.

Bookmark this page to read our Quick Takes LIVE

The links below will scroll you directly to the Quick Take related to the specific company listed.

Here are this week's Quick Takes:

Next Investors (commodities): China to spend US$2.3 trillion on infrastructure

EV1: Now listed on the Frankfurt Stock Exchange

PRM/GLV: LNG markets to benefit from Russian gas supply tightening

FNT: Rare earths drilling scheduled for May, drill plan confirmed

LRS: Thickest intercept to date at Brazilian lithium project

KNI: Letter of Intent between Beyonder AS and Kuniko

EMN: Director appointed, details of conference call

VN8: Fruits of acquisitions leads to record quarterly result

WHK: Up 20% on strong cybersecurity sales figures

PFE: Flagship shifting focus from iron ore to copper/gold

PFE: Drilling plans revealed for Hellcat Project, WA

AKN:Cobalt- Another in-demand commodity to be added to flagship

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.